Bank of America 2005 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

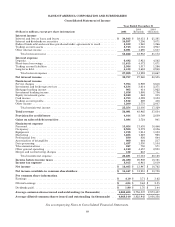

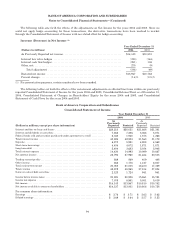

BANK OF AMERICA CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements

Bank of America Corporation and its subsidiaries (the Corporation) through its banking and nonbanking

subsidiaries, provide a diverse range of financial services and products throughout the U.S. and in selected international

markets. At December 31, 2005, the Corporation operated its banking activities primarily under two charters: Bank of

America, National Association (Bank of America, N.A.) and Bank of America, N.A. (USA). On June 13, 2005, Fleet

National Bank merged with and into Bank of America, N.A., with Bank of America, N.A. as the surviving entity. This

merger had no impact on the Consolidated Financial Statements of the Corporation. On June 30, 2005, the Corporation

announced a definitive agreement to acquire all outstanding shares of MBNA Corporation (MBNA) (the MBNA Merger).

The transaction was effective January 1, 2006. On April 1, 2004, the Corporation acquired all of the outstanding stock of

FleetBoston Financial Corporation (FleetBoston) (the FleetBoston Merger).

Note 1—Summary of Significant Accounting Principles

Restatement

The Corporation is restating its historical financial statements for the years 2004 and 2003, for the quarters in 2005

and 2004, and other selected financial data for the years 2002 and 2001. These restatements and resulting revisions

relate to the accounting treatment for certain derivative transactions under the Statement of Financial Accounting

Standards (SFAS) No. 133, “Accounting for Derivative Instruments and Hedging Activities, as amended” (SFAS 133).

As a result of an internal review completed in the first quarter of 2006 of the hedge accounting treatment of certain

derivatives, the Corporation concluded that certain hedging relationships did not adhere to the requirements of SFAS

133. The derivatives involved were used as hedges principally against changes in interest rates and foreign currency

rates in the Asset and Liability Management (ALM) process.

A number of the transactions included in the restatement did not meet the strict requirements of the “shortcut”

method of accounting under SFAS 133. Although these hedging relationships would have qualified for hedge accounting

if the “long haul” method had been applied, SFAS 133 does not permit the use of the “long haul” method retroactively.

Consequently, the restatement assumes hedge accounting was not applied to these derivatives and the related hedged

item during the periods under review. A majority of these transactions related to internal interest rate swaps whereby

the Corporation used its centralized trading desk to execute these trades to achieve operational effectiveness and cost

efficiency. These interest rate swap trades were executed internally between the Corporation’s treasury operations and

the centralized trading desk. It has been the Corporation’s long standing policy to lay these internal swaps off to an

external party within a three-day period. In almost all cases, cash was exchanged (either paid or received) with the

external counterparty to compensate for market rate movements between the time that the internal swap and the

matching trade with the external counterparty were executed. Although the overall external trade, including the cash

exchanged, was transacted at a fair market value of zero, the cash exchanged offset the fair market value of the external

swap which was other than zero. Swaps with a fair market value other than zero at the inception of the hedge cannot

qualify for hedge accounting under the shortcut method. Accordingly, the shortcut method was incorrectly applied for

such derivative instruments.

The Corporation also entered into certain cash flow hedges which utilized the centralized trading desk to lay off the

internal trades with an external party. The key attributes, including interest rates and maturity dates, of the internal

and external trades were not properly matched. The Corporation performed the effectiveness assessment and measure of

ineffectiveness on the internal trades instead of the external trades. As a result, such tests were not performed in

accordance with the requirements of SFAS 133. Accordingly, hedge accounting was incorrectly applied for such

derivative instruments.

The Corporation used various derivatives in other hedging relationships to hedge changes in fair value or cash flows

attributable to either interest or foreign currency rates. Although these transactions were documented as hedging

relationships at inception of the hedge, the upfront and ongoing effectiveness testing was either not performed,

documented or assessed in accordance with SFAS 133. In addition, for one cash flow hedge transaction relating to the

anticipated purchase of securities, which impacted the third quarter of 2004 by $399 million, the timing of an amount

reclassified from Accumulated OCI to earnings upon the subsequent sale of such securities was adjusted. Adjustments to

correct the accounting for those hedging relationships are included in the restated results. We do not believe that these

adjustments are material individually or in the aggregate to our financial results for any reported period.

93