Bank of America 2005 Annual Report Download - page 162

Download and view the complete annual report

Please find page 162 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

BANK OF AMERICA CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements—(Continued)

line commitments in the previous table. The outstanding balances related to these charge cards were $171 million and

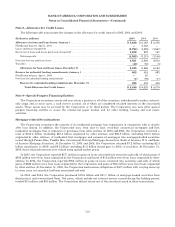

$205 million at December 31, 2005 and 2004.

At December 31, 2005, the Corporation had whole mortgage loan purchase commitments of $4.0 billion, all of which

will settle in the first quarter of 2006. At December 31, 2004, the Corporation had whole mortgage loan purchase

commitments of $3.3 billion, all of which settled in the first quarter of 2005. At December 31, 2005 and 2004, the

Corporation had no forward whole mortgage loan sale commitments.

The Corporation has entered into operating leases for certain of its premises and equipment. Commitments under

these leases approximate $1.3 billion in 2006, $1.1 billion in 2007, $1.1 billion in 2008, $799 million in 2009, $650 million

in 2010 and $3.5 billion for all years thereafter.

In 2005, the Corporation entered into an agreement for the committed purchase of retail automotive loans over a

five-year period, ending June 30, 2010. In 2005, the Corporation purchased $5.0 billion of such loans and at

December 31, 2005, the remaining commitment amount was $47.0 billion. Under the agreement, the Corporation is

committed to purchase up to $7.0 billion of such loans for the period January 1, 2006 through June 30, 2006 and up to

$10.0 billion in each of the agreement’s next four fiscal years.

Other Guarantees

The Corporation sells products that offer book value protection primarily to plan sponsors of Employee Retirement

Income Security Act of 1974 (ERISA) governed pension plans, such as 401(k) plans and 457 plans. The book value

protection is provided on portfolios of intermediate/short-term investment grade fixed income securities and is intended

to cover any shortfall in the event that plan participants withdraw funds when market value is below book value. The

Corporation retains the option to exit the contract at any time. If the Corporation exercises its option, the purchaser can

require the Corporation to purchase zero coupon bonds with the proceeds of the liquidated assets to assure the return of

principal. To manage its exposure, the Corporation imposes significant restrictions and constraints on the timing of the

withdrawals, the manner in which the portfolio is liquidated and the funds are accessed, and the investment parameters

of the underlying portfolio. These constraints, combined with structural protections, are designed to provide adequate

buffers and guard against payments even under extreme stress scenarios. These guarantees are booked as derivatives

and marked to market in the trading portfolio. At December 31, 2005 and 2004, the notional amount of these guarantees

totaled $34.0 billion and $26.3 billion with estimated maturity dates between 2006 and 2035. As of December 31, 2005

and 2004, the Corporation has not made a payment under these products, and management believes that the probability

of payments under these guarantees is remote.

The Corporation also sells products that guarantee the return of principal to investors at a preset future date. These

guarantees cover a broad range of underlying asset classes and are designed to cover the shortfall between the market

value of the underlying portfolio and the principal amount on the preset future date. To manage its exposure, the

Corporation requires that these guarantees be backed by structural and investment constraints and certain pre-defined

triggers that would require the underlying assets or portfolio to be liquidated and invested in zero-coupon bonds that

mature at the preset future date. The Corporation is required to fund any shortfall at the preset future date between the

proceeds of the liquidated assets and the purchase price of the zero-coupon bonds. These guarantees are booked as

derivatives and marked to market in the trading portfolio. At December 31, 2005 and 2004, the notional amount of these

guarantees totaled $6.5 billion and $8.1 billion. These guarantees have various maturities ranging from 2006 to 2016. At

December 31, 2005 and 2004, the Corporation had not made a payment under these products, and management believes

that the probability of payments under these guarantees is remote.

The Corporation also has written put options on highly rated fixed income securities. Its obligation under these

agreements is to buy back the assets at predetermined contractual yields in the event of a severe market disruption in

the short-term funding market. These agreements have various maturities ranging from two to seven years, and the

pre-determined yields are based on the quality of the assets and the structural elements pertaining to the market

disruption. The notional amount of these put options was $803 million and $653 million at December 31, 2005 and 2004.

Due to the high quality of the assets and various structural protections, management believes that the probability of

incurring a loss under these agreements is remote.

In the ordinary course of business, the Corporation enters into various agreements that contain indemnifications,

such as tax indemnifications, whereupon payment may become due if certain external events occur, such as a change in

tax law. These agreements typically contain an early termination clause that permits the Corporation to exit the

agreement upon these events. The maximum potential future payment under indemnification agreements is difficult to

assess for several reasons, including the inability to predict future changes in tax and other laws, the difficulty in

determining how such laws would apply to parties in contracts, the absence of exposure limits contained in standard

126