Bank of America 2005 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

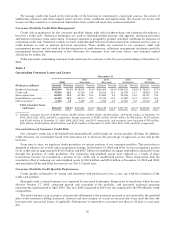

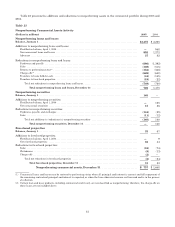

Commercial Portfolio Credit Quality Performance

Overall commercial credit quality continued to improve in 2005; however, the rate of improvement slowed in the

second half of the year.

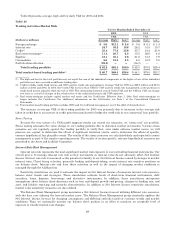

Table 20 presents commercial net charge-offs and net charge-off ratios for 2005 and 2004.

Table 20

Commercial Net Charge-offs and Net Charge-off Ratios(1)

2005 2004

(Dollars in millions) Amount Percent Amount Percent

Commercial—domestic ......................................... $170 0.13% $177 0.15%

Commercial real estate ......................................... —— (3) (0.01)

Commercial lease financing ..................................... 231 1.13 90.05

Commercial—foreign ........................................... (72) (0.39) 173 1.05

Total commercial ........................................ $329 0.16% $356 0.20%

(1) Percentage amounts are calculated as net charge-offs divided by average outstanding loans and leases during the year for each loan

category.

Commercial net charge-offs were $329 million for 2005 compared to $356 million for 2004. Commercial lease

financing net charge-offs increased $222 million in 2005 compared to 2004 primarily due to the domestic airline

industry. Commercial—foreign net recoveries were $72 million in 2005 compared to net charge-offs of $173 million in

2004. Recoveries were centered in Bermuda, Latin America, India and the United Kingdom. Commercial—foreign net

charge-offs of $173 million in 2004 were primarily related to one borrower in the food products industry.

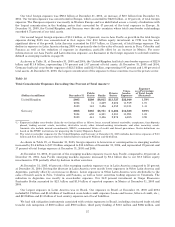

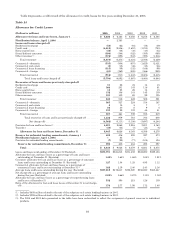

As presented in Table 21, commercial criticized credit exposure decreased $2.7 billion, or 27 percent, to $7.5 billion

at December 31, 2005. The net decrease was driven by $9.9 billion of paydowns, payoffs, credit quality improvements,

charge-offs principally related to the domestic airline industry, and loan sales. Reductions were distributed across many

industries of which the largest were airlines, utilities and media. These decreases were partially offset by $7.2 billion of

newly criticized exposure. Global Business and Financial Services accounted for 54 percent, or $1.5 billion, of the

decrease in commercial criticized exposure centered in Commercial Aviation,Latin America and Middle Market

Banking, which comprised 20 percent, 15 percent and 9 percent of the total decrease. Global Capital Markets and

Investment Banking accounted for 33 percent, or $896 million, of the decrease in criticized exposure.

Table 21

Commercial Criticized Exposure(1)

December 31

2005 2004

(Dollars in millions) Amount Percent(2) Amount Percent(2)

Commercial—domestic ..................................... $5,259 2.62% $ 6,340 3.38%

Commercial real estate ..................................... 723 1.63 1,028 2.54

Commercial lease financing ................................. 611 2.95 1,347 6.38

Commercial—foreign ...................................... 934 1.73 1,534 3.12

Total commercial criticized exposure ................. $7,527 2.35% $10,249 3.44%

(1) Criticized exposure corresponds to the Special Mention, Substandard and Doubtful asset categories defined by regulatory

authorities. Exposure amounts include loans and leases, SBLCs and financial guarantees, derivative assets, assets held-for-sale

and commercial letters of credit.

(2) Commercial criticized exposure is taken as a percentage of total commercial utilized exposure.

We routinely review the loan and lease portfolio to determine if any credit exposure should be placed on

nonperforming status. An asset is placed on nonperforming status when it is determined that full collection of principal

and/or interest in accordance with its contractual terms is not probable. As presented in Table 22, nonperforming

commercial assets decreased $891 million to $757 million at December 31, 2005 due primarily to the $749 million

decrease in nonperforming commercial loans and leases.

The decrease in total nonperforming commercial loans and leases primarily resulted from paydowns and payoffs of

$686 million, gross charge-offs of $669 million, returns to performing status of $152 million and loan sales of $108

million. These decreases were partially offset by new nonaccrual loans of $929 million.

59