Philips 2014 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2014 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

|

|

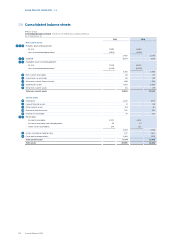

Group nancial statements 12.9

Annual Report 2014 117

IFRS 15 Revenue from Contracts with Customers

IFRS 15 species how and when revenue is recognized

as well as describes more informative and relevant

disclosures. The Standard supersedes IAS 18 Revenue,

IAS 11 Construction Contracts and a number of revenue-

related interpretations.

The new Standard provides a single, principles based

ve-step model to be applied to all contracts with

customers. Furthermore, it provides new guidance on

whether revenue should be recognized at a point in

time or over time. The standard also introduces new

guidance on costs of fullling and obtaining a contract,

specifying the circumstances in which such costs

should be capitalized. Costs that do not meet the

criteria must be expensed when incurred.

IFRS 15 must be applied for periods beginning on or

after January 1, 2017. The Company is currently

assessing the impact of the new Standard.

Specic choices within IFRS

Sometimes IFRS allows alternative accounting

treatments for measurement and/or disclosure. The

most important of these alternative treatments are

mentioned below.

Tangible and intangible xed assets

Under IFRS, an entity shall choose either the cost model

or the revaluation model as its accounting for tangible

and intangible xed assets. In this respect, items of

property, plant and equipment are measured at cost

less accumulated depreciation and accumulated

impairment losses. The useful lives and residual values

are evaluated annually. Furthermore, the Company

chose to apply the cost model meaning that costs

relating to product development, the development and

purchase of software for both internal use and software

intended to be sold and other intangible assets are

capitalized and subsequently amortized over the

estimated useful life.

Employee benet accounting

IFRS does not specify how an entity should present its

service costs related to pensions and net interest on the

net dened benet liability (asset) in the Statement of

income. With regards to these elements, the Company

presents service costs in Income from operations and

the net interest expenses related to dened benet

plans in Financial expense.

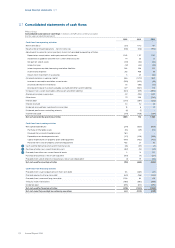

Cash ow statements

Under IFRS, an entity shall report cash ows from

operating activities using either the direct method

(whereby major classes of gross cash receipts and gross

cash payments are disclosed) or the indirect method

(whereby prot or loss is adjusted for the eects of

transactions of a non-cash nature, any deferrals or

accruals of past or future operating cash receipts or

payments, and items of income or expense associated

with investing or nancing cash ows). In this respect,

the Company chose to prepare the cash ow

statements using the indirect method.

Furthermore, interest cash flows are presented in cash flows

from operating activities rather than financing or investing

cash flows, because they enter into the determination of

profit or loss. The Company choose to present dividends paid

to shareholders of Koninklijke Philips N.V. as a component

of cash flows from financing activities, rather than to present

such dividends as operating cash flows which is an allowed

alternative under IFRS.

Policies that are more critical in nature

Revenue recognition

Revenue from the sale of goods in the course of the

ordinary activities is measured at the fair value of the

consideration received or receivable, net of returns,

trade discounts and volume rebates. Revenue for sale

of goods is recognized when the signicant risks and

rewards of ownership have been transferred to the

buyer, recovery of the consideration is probable, the

associated costs and possible return of the goods can

be estimated reliably, there is no continuing

involvement with goods, and the amount of revenue

can be measured reliably. If it is probable that discounts

will be granted and the amount can be measured

reliably, then the discount is recognized as a reduction

of revenue as the sales are recognized.

Transfer of risks and rewards varies depending on the

individual terms of the contract of sale. For consumer-type

products in the sectors Lighting and Consumer Lifestyle

these criteria are met at the time the product is shipped

and delivered to the customer and title and risk have

passed to the customer (depending on the delivery

conditions) and acceptance of the product has been

obtained. Examples of delivery conditions are ‘Free on

Board point of delivery’ and ‘Costs, Insurance Paid point

of delivery’, where the point of delivery may be the

shipping warehouse or any other point of destination as

agreed in the contract with the customer and where title

and risk for the goods pass to the customer.

Revenues of transactions that have separately

identiable components are recognized based on their

relative fair values. These transactions mainly occur in

the Healthcare sector and include arrangements that

require subsequent installation and training activities in

order to become operable for the customer. However,

since payment for the equipment is contingent upon

the completion of the installation process, revenue

recognition is generally deferred until the installation

has been completed and the product is ready to be

used by the customer in the way contractually agreed.

Revenues are recorded net of sales taxes, customer

discounts, rebates and similar charges. For products for

which a right of return exists during a dened period,

revenue recognition is determined based on the

historical pattern of actual returns, or in cases where