General Motors 2010 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2010 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

|

|

GENERAL MOTORS COMPANY AND SUBSIDIARIES

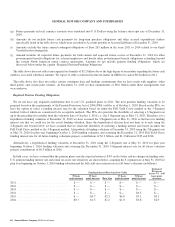

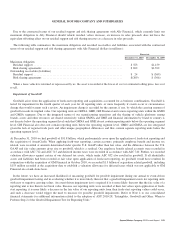

The following table illustrates the sensitivity to a change in certain assumptions for the pension plans, holding all other assumptions

constant (dollars in millions):

Successor

U.S. Plans Non-U.S. Plans

Effect on 2011

Pension

Expense

Effect on

December 31,

2010

PBO

Effect on 2011

Pension

Expense

Effect on

December 31,

2010

PBO

25 basis point decrease in discount rate .............................. –$110 +$2,540 –$ 7 +$714

25 basis point increase in discount rate .............................. +$ 90 –$2,470 +$10 –$677

25 basis point decrease in expected return on assets .................... +$210 — +$35 —

25 basis point increase in expected return on assets .................... –$210 — –$35 —

The U.S. pension plans generally provide covered U.S. hourly employees hired prior to October 15, 2007 with pension benefits of

negotiated, flat dollar amounts for each year of credited service earned by an individual employee. Early retirement supplements are

also provided to those who retire prior to age 62. Hourly employees hired after October 15, 2007 participate in a cash balance pension

plan. Formulas providing for such stated amounts are contained in the applicable labor contract. Pension expense and the pension

obligations do not consider any future benefit increases or decreases that may occur beyond current labor contracts. The usual cycle

for negotiating new labor contracts is every four years. We do not have a past practice of maintaining a consistent level of benefit

increases or decreases from one contract to the next.

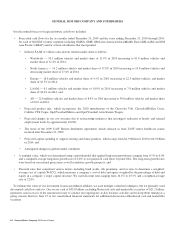

The following data illustrates the sensitivity of changes in pension expense and pension obligation based on the last remeasurement

of the U.S hourly pension plan at December 31, 2010, as a result of changes in future benefit units for U.S. hourly employees,

effective after the expiration of the current contract (dollars in millions):

Successor

Change in future benefit units

Effect on

2011

Pension Expense

Effect on

December 31, 2010

PBO

One percentage point increase in benefit units .......................................... +$81 +$240

One percentage point decrease in benefit units .......................................... –$79 –$233

We utilize a variety of pricing sources to estimate the fair value of our pension assets, including: independent pricing vendors,

dealer or counterparty supplied valuations, third party appraisals, appraisals prepared by investment managers, or investment sponsor

or third party administrator supplied net asset value (or its equivalent) per share (NAV) used as a practical expedient.

A significant portion of our pension assets are classified in Level 3. Pension assets for which fair value is determined through the

use of NAV and for which we may not have the ability to redeem our entire investment with the investee at NAV as of the

measurement date or in the near-term, are classified in Level 3. We classify pension assets that include significant unobservable inputs

in Level 3.

Significant assets classified in Level 3, with the related Level 3 inputs to the valuation that may be subject to volatility and change,

and additional considerations for leveling, are as follows:

• Government, agency and corporate debt securities — Pricing services and dealers often use proprietary pricing models which

incorporate unobservable inputs. These inputs primarily consist of yield and credit spread assumptions. Management may

consider other security attributes such as liquidity, market activity, price level, credit ratings and geo-political risk, in assessing

the observability of inputs used by pricing services or dealers, which may affect classification in the fair value hierarchy.

• Group annuity contracts – The value of each group annuity contract or policy depends, in part, on the values of the units of the

separately managed investment accounts backing the contract. The fair value of the separately managed investment account

98 General Motors Company 2010 Annual Report