General Motors 2010 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2010 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

|

|

GENERAL MOTORS COMPANY AND SUBSIDIARIES

When available, quoted market prices are used to determine fair value. If quoted market prices are not available, fair value is based

upon valuation techniques that use, where possible, market-based inputs. Generally, fair value is estimated using a combination of the

income approach and the market approach because circumstances usually do not permit the use of a single approach. Under the

income approach, estimated future cash flows are discounted at a rate commensurate with the risk involved using marketplace

assumptions. Under the market approach, valuations are based on actual comparable market transactions and market earnings and

book value multiples for the same or comparable entities. The assumptions used in the income and market approaches have a

significant effect on the determination of fair value. Significant assumptions include estimated future cash flows, appropriate discount

rates, and adjustments to market transactions and market multiples for differences between the market data and the investment being

valued. Changes to these assumptions could have a significant effect on the valuation of cost and equity method investments.

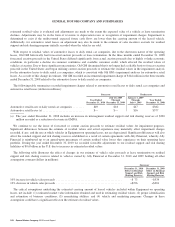

In the three months ended December 31, 2009 we recorded impairment charges related to our investment in Ally Financial common

stock of $270 million. We determined the fair value of our investment in Ally Financial common stock using a market multiple,

sum-of-the-parts methodology. This methodology considered the average price/tangible book value multiples of companies deemed

comparable to each of Ally Financial’s operations, which were then aggregated to determine Ally Financial’s overall fair value. Based

on our analysis, the estimated fair value of our investment in Ally Financial common stock was determined to be $970 million,

resulting in an impairment charge of $270 million. The following table illustrates the effect of a 0.1 change in the average price/

tangible book value multiple on our impairment charge (dollars in millions):

Change in Assumption

Effect on

December 31, 2009

Impairment Charges

Increase in average price/tangible book value multiple .......................................................... +$100

Decrease in average price/tangible book value multiple ......................................................... –$100

At December 31, 2010 the balance of our investment in Ally Financial common stock was $964 million and the balance of our

investment in Ally Financial preferred stock was $665 million.

Derivatives

Derivatives are used in the normal course of business to manage exposures arising from market risks resulting from changes in

certain commodity prices and interest and foreign currency exchange rates. Derivatives are accounted for in the consolidated balance

sheets as assets or liabilities at fair value.

Significant judgments and estimates are used in estimating the fair values of derivative instruments, particularly in the absence of

quoted market prices. Internal models are used to value a majority of derivatives. The models use, as their basis, readily observable

market inputs, such as time value, forward interest rates, volatility factors, and current and forward market prices for commodities and

foreign currency exchange rates.

The valuation of derivative liabilities takes into account our nonperformance risk. At December 31, 2010 and December 31, 2009,

our nonperformance risk was not observable through a liquid credit default swap market. Our nonperformance risk was estimated

using internal analysis to develop conclusions on our implied credit rating, which we used to determine the appropriate credit spread,

which would be applied to us by market participants. Prior to receiving published credit ratings we developed our credit rating

conclusions using an analysis of comparable industrial companies. At December 31, 2010 we incorporated published credit agency

ratings of GM into our credit rating conclusions. At December 31, 2009, all derivatives whose fair values contained a significant

credit adjustment based on our nonperformance risk were classified in Level 3. At December 31, 2010, we have determined that our

non-performance risk no longer represents a significant input in the determination of the fair value of our derivatives. As of

December 31, 2010 all automotive operations derivatives have been classified in Level 2.

Sales Incentives

The estimated effect of sales incentives to dealers and customers is recorded as a reduction of Automotive revenue, and in certain

instances, as an increase to Automotive cost of sales, at the later of the time of sale or announcement of an incentive program to

dealers. There may be numerous types of incentives available at any particular time, including a choice of incentives for a specific

106 General Motors Company 2010 Annual Report