General Motors 2010 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2010 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

|

|

GENERAL MOTORS COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

primarily utilized for certain assets related to land, buildings and land improvements, leasehold interests, and the majority of

our machinery and equipment and tooling. Economic obsolescence represents a loss in value due to unfavorable external

conditions such as the economics of our industry and was a factor in establishing fair value. Our machinery, equipment and

special tools amounts, determined under the cost approach, were adjusted for economic obsolescence. Due to the downturn in

the automotive industry, significant excess capacity exists and the application of the cost approach generally requires the

replacement cost of an asset to be adjusted for physical deterioration, and functional and economic obsolescence. We

estimated economic obsolescence as the difference between the discounted cash flows expected to be realized from our

utilization of the assets as a group, compared to the initial estimate of value from the cost approach method. We did not reduce

any fixed asset below its liquidation in place value as a result of economic obsolescence; however the effects of economic

obsolescence caused some of our fixed assets to be recorded at their liquidation in place values.

• The income approach which considers value in relation to the present worth of future benefits derived from ownership, usually

measured through the capitalization of a specific level of income which can be derived from the subject asset. This method

assumed fair value could not exceed the present value of the cash flows the assets generate discounted at a risk related rate of

return commensurate with the level of risk inherent in the subject asset. This method was used to value certain assets related to

buildings and improvements, leasehold interest, machinery and equipment and tooling.

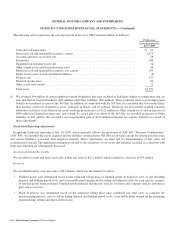

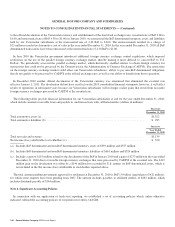

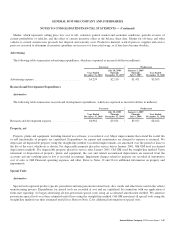

The following table summarizes the components of Property as a result of the application of fresh-start reporting at July 10, 2009

and Property, net at July 9, 2009:

Successor Predecessor

July 10,

2009

July 9,

2009

Land ..................................................................................... $ 2,524 $ 1,040

Buildings and land improvements, net .......................................................... 3,731 8,490

Machinery and equipment, net ................................................................ 5,915 13,597

Construction in progress ..................................................................... 1,838 2,307

Real estate, plants, and equipment, net .......................................................... 14,008 25,434

Special tools, net ........................................................................... 4,492 10,782

Total property, net .......................................................................... $18,500 $36,216

Goodwill

We recorded Goodwill of $30.5 billion upon application of fresh-start reporting. When applying fresh-start reporting, certain

accounts, primarily employee benefit and income tax related, were recorded at amounts determined under specific U.S. GAAP rather

than fair value and the difference between the U.S. GAAP and fair value amounts gives rise to goodwill, which is a residual. Further,

we recorded valuation allowances against certain of our deferred tax assets, which under ASC 852 also resulted in goodwill. Our

employee benefit related accounts were recorded in accordance with ASC 712 and ASC 715 and deferred income taxes were recorded

in accordance with ASC 740. None of the goodwill from this transaction is deductible for tax purposes.

Intangible Assets

We recorded Intangible assets of $16.1 billion at their fair values. The following is a summary of the approaches used to determine

the fair value of our significant intangible assets:

• We recorded $7.9 billion for the fair value of technology. The relief from royalty method was used to calculate the $7.7 billion

fair value of developed technology. The significant assumptions used included:

• Forecasted revenue for each technology category by Old GM’s former segments;

138 General Motors Company 2010 Annual Report