RBS 2012 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

116

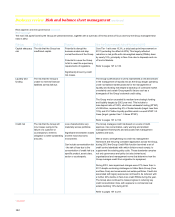

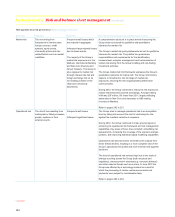

Business review Risk and balance sheet management continued

Risk appetite and risk governance continued

Risk organisation*

The Group has an independent risk management function (‘RBS Risk

Management’) which manages risk through independent challenge and

oversight of the customer-facing businesses and support functions. It

provides an overarching risk control framework linked to the risk appetite

of the Group.

The Head of Restructuring and Risk is the Group Chief Risk Officer, who

leads this function through the strategic setting and execution of its

responsibilities. The Head of Restructuring and Risk reports to the Group

Chief Executive and the Board Risk Committee, with a right of access to

the Chairman.

RBS Risk Management is designed to align as closely as possible with

the customer-facing businesses and support functions while maintaining

an appropriate level of independence, which underpins the Group’s

approach to risk management and is reinforced through the Group by

appropriate reporting lines.

Within RBS Risk Management, Group functional heads (e.g. the Group

Chief Credit Officer for the credit risk discipline, the Group Head of

Operational Risk for the operational risk discipline) report directly into the

Head of Restructuring and Risk and are responsible for firm-wide risk

appetite and standards under their respective disciplines. For example,

Group Compliance is responsible for conduct risk policy ownership,

change management, assurance and training frameworks at Group level,

including anti-money laundering, sanctions, terrorist financing, anti-

bribery and corruption.

Risk management within divisions focuses on all material risks including

credit, market, operational, regulatory and country risk, and business

activities. Liquidity risk and the day-to-day management of liquidity and

funding of the book is Group Treasury’s responsibility.

Oversight of risk within divisions is the responsibility of the relevant

divisional Chief Risk Officer (CRO), with input from the relevant Group

heads of function. This involves ensuring that:

x All activities undertaken by the individual divisions are consistent

with the Group’s risk appetite targets;

x Group policies and resulting operating frameworks, including

delegated authorities and limits, are complied with through effective

monitoring and exception reporting; and

x There is the effective operation of Group-wide risk processes such

as the Group Policy Framework and the New Product Risk

Assessment Process.

Divisional CROs have a direct functional reporting line to the Deputy

Group CRO.

The Head of Restructuring and Risk and the Deputy Group CRO have a

direct involvement in the selection, appointment or removal of divisional

CROs and Group functional heads and also have responsibility for their

ongoing performance assessment and management.

Divisions mirror the Group set-up for risk management, i.e. the Divisional

Executive Committees are responsible for setting and owning their risk

appetite within Group constraints. The Divisional Risk Committees

oversee the businesses relative to divisional and Group risk appetite and

focus on ensuring that risks are adequately monitored and controlled.

The Divisional CROs provide independent oversight to this process, with

support from the Group Chief Risk Officer, the Deputy Group CRO and

Group functional heads as appropriate. Additional challenge and

oversight is provided by Group functional heads on an ongoing basis and

by Divisional Risk and Audit Committees on a periodic review basis.

For more information on risk governance and a presentation of the

Group’s risk committees, refer to pages 117 to 120. For a summary of the

main risk types faced by the Group and how it manages each of them,

refer to pages 122 to 126.

Three lines of defence

Having a strong three lines of defence model is important in a strong

control environment. The Executive Committee approved a refreshed

model in February 2012 and work is underway to embed this across the

Group. The model’s main purpose is to define accountabilities and

responsibilities for managing risk across the Group.

*unaudited