RBS 2012 Annual Report Download - page 169

Download and view the complete annual report

Please find page 169 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

167

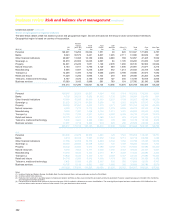

2012 2011 2010

AQ10 credit risk assets by division AQ10

£m

Divisional credit

risk assets

%

AQ10

£m

Divisional credit

risk assets

%

AQ10

£m

Divisional credit

risk assets

%

UK Retail 4,998 4.4 5,097 4.6 5,017 4.6

UK Corporate 6,310 6.25,484 5.2 5,198 4.8

International Banking 612 0.9 1,736 2.4 2,227 2.8

Ulster Bank 8,236 24.16,305 16.7 4,348 10.7

US Retail & Commercial 633 1.2646 1.1 599 1.2

Retail & Commercial 20,789 5.3 19,268 4.8 17,389 4.3

Markets 773 0.7 749 0.7 605 0.5

Core 21,5623.8 20,017 3.4 17,994 3.2

Non-Core 22,845 35.025,020 27.0 25,005 19.9

44,4077.145,037 6.7 42,999 6.2

Key points

x Trends in the asset quality of the Group’s credit risk exposures

during 2012 reflected changes in the composition of the Core

portfolio and the run-off and disposals of Non-Core assets as well as

regrading through new and updated models, particularly in relation

to the bank and personal sectors. Adjusting for those factors, the

overall asset quality of the Group’s corporate exposure was broadly

unchanged despite difficult external conditions in the UK and

ongoing uncertainty in the eurozone.

x The decrease in the Group’s Core exposures within the AQ1 band

reflects the decrease in the Group’s exposure to sovereigns in

Western Europe and North America and the change in the bank and

sovereign Probability of Default (PD) rating models noted on page

162. The credit outlook for banks and sovereigns continues to be

challenging and the transition to the updated PD models creates

additional credit migration causing assets to move to higher PDs.

While the nominal value and appearance of migration out of AQ1 is

material most of the migration continues to occur within the range of

stronger credit grades and hence the change in the credit quality of

the portfolio is modest. The weighted PD percentage for banks and

sovereigns increased by 5 basis points to 0.13% and 3 basis points

to 0.04% respectively. The AQ composition of the Corporate

portfolio has not changed materially during the year.

x The increase in AQ4 is partly driven by the change to the bank and

sovereign PD models noted above, and partly due to the

improvement in the UK Retail mortgage asset quality band

distribution. This followed updates to the Group’s models which

were delayed whilst long term recalibrations were made to the

capital rating system. These PD recalibrations reflect improvements

in the underlying credit quality of the UK mortgage portfolio.

x On a sector basis, the proportion of non-performing assets in the

property sector increased slightly to 58% of total AQ10 exposure

(2011 - 57%). Non-performing assets relating to property represent

a material proportion of AQ10 exposure in Non-Core (85%), UK

Corporate (56%) and Ulster Bank (30%). In particular, continued

weakness in the Irish economy meant non-performing assets in the

Ulster Bank portfolio continued to grow, driven by exposures in the

personal and property sectors. Refer to the Key credit portfolios:

Ulster Bank Group (pages 190 to 193) for more details. A small

number of significant individual non-performing property cases led to

the overall increase in the AQ10 population in UK Corporate.

x Non-performing assets (AQ10) in Non-Core increased as a

percentage of the overall Non-Core portfolio due to the run-off and

disposals of better performing assets. The overall level of AQ10

assets in Non-Core fell due to repayments, assets returning to the

performing book and the write off of certain real estate exposures in

2012.

x In UK Retail non-performing assets (AQ10) reduced slightly during

the year predominantly as a result of lower flows of unsecured

assets into non-performing. Recovery activity on non-performing

assets is pursued over a number of years during which time the

assets remain on balance sheet along with the appropriate

impairment provision.

x Non-performing credit risk assets within International Banking

decreased markedly as renegotiations led to the return of significant

exposure in the transport sector to the performing book.