RBS 2012 Annual Report Download - page 318

Download and view the complete annual report

Please find page 318 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

308 -

309

309 -

310

310 -

311

311 -

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

316

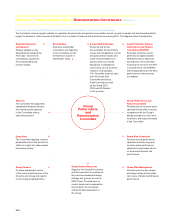

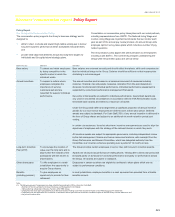

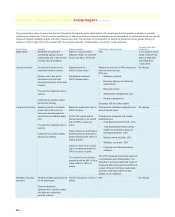

Report of the Board Risk Committee

Letter from Philip Scott,

Chairman of the Board Risk Committee

Dear Shareholder,

I report to you following another challenging twelve months for the Board

Risk Committee. The already demanding schedule of the Committee was

intensified in the period by a number of significant issues, most notably

the IT incident that occurred in June 2012. The Board Risk Committee

has undertaken, on behalf of the Board, to review the cause,

consequence and subsequent management of the IT incident which had

such unacceptable consequences for many of our customers. As a

priority, the Committee has overseen remediation and has sought to

ensure appropriate redress for customers. It will continue carefully to

oversee management of residual technology risks and will ensure

communication with our regulators and stakeholders on conclusion of the

internal and external investigations of the incident, as appropriate.

While 2012 has presented significant challenges, there has also been a

great deal of progress on the development and implementation of risk

and control throughout the organisation. The Board Risk Committee has

been pleased to exercise an oversight role in the development and

enhancement of the risk management framework and associated tools

that support the Group’s aim of being a safer and more sustainable bank.

The Committee has provided input into the Group’s risk strategy and

objectives during 2012 and has overseen the refinement and further

embedding of the Group’s framework into the business divisions. This

has enabled the Committee to gain an improved understanding of the

major risks which the Group faces, including market risk, conduct risk,

country risk, credit risk (including single name concentrations and sector

risk) regulatory risk and operational risk and to ensure robust plans are in

place to manage excess exposures. The Group’s stress testing

capabilities have been developed and are now being used within

business as usual as an effective strategic planning and capital

management tool.

The Board Risk Committee has supported the articulation of a conduct

risk appetite statement which is being embedded strategically within the

Group’s Policy Framework. Conduct Risk standards are being

communicated to staff using the four pillars of conduct risk, employee

conduct, market conduct, corporate conduct and conduct towards

customers. The Committee will monitor implementation of these

enhanced standards during 2013.

Enhancements to risk reporting have continued in the period to ensure

that reports are insightful and relevant, and provide more metric based

information. Data quality is, of course, critical to the accuracy of reporting

and the Committee has received in depth updates on the progress of

data quality programmes and reporting initiatives ongoing throughout the

organisation, most notably the Finance and Risk Transformation

Programme.

However, inevitably risk management tools and measures can only take

the organisation so far. The future success of RBS depends upon the

correct culture and approach that places the customer at the forefront of

all decision making. The Board Risk Committee is fully supportive of the

measures being developed to engender the correct behaviours at all

levels within the RBS Group. The Committee has worked closely with the

Group Performance and Remuneration Committee over the past 12

months to consider issues relating to individual accountability and

responsibility for legacy and new issues. Where appropriate,

recommendations have been made to the Group Performance and

Remuneration Committee in relation to risk performance and reward.

Culture, including the role of financial incentives and reward, will continue

to be a priority of the Committee during 2013.

The members of the Committee have dedicated significant additional time

to the consideration of risk issues during 2012 and I would like to thank

them for their dedication and commitment. The business of the

Committee is set to be no less demanding in 2013. The creation of the

Prudential Regulatory Authority and the Financial Conduct Authority as

part of the UK’s twin peaks regulatory framework will be a major influence

and the Group will have to adapt to the new regulatory approach and

work closely with regulators to implement changes to standards and

reporting where required.

More detailed information on the business of the Committee during 2012

is set out in the Board Risk Committee Report that follows.

Philip Scott

Chairman of the Board Risk Committee

27 February 2013