RBS 2012 Annual Report Download - page 190

Download and view the complete annual report

Please find page 190 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

188

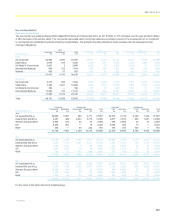

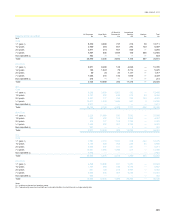

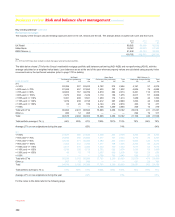

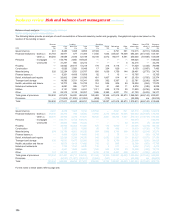

Business review Risk and balance sheet management continued

Key credit portfolios*: Residential mortgages: Key points continued

Ulster Bank

x Ulster Bank’s residential mortgage portfolio totalled £19.2 billion at

31 December 2012, with 88% in the Republic of Ireland and 12% in

Northern Ireland. At constant exchange rates, the portfolio

decreased 2% from 31 December 2011 as a result of natural

amortisation and limited growth due to low market demand.

x The assets include £2.3 billion of exposure (12%) of residential buy-

to-let loans. The interest rate product mix is approximately 91% on a

variable rate product (including tracker products) and 9% on a fixed

rate.

x 16% of the total portfolio is on interest only which reflects legacy

policy and is no longer available to residential mortgage customers

on a permanent basis. Interest only is permitted on a temporary

basis under the suite of forbearance treatments available within

Ulster Bank (refer to page 178 for further information). Interest only

repayment remains an option for private customers within Northern

Ireland on an exception basis.

x Average LTVs increased from 31 December 2011 to 31 December

2012, on a value basis, as a result of decreases in the Central

Statistics Office house price index (4%) impacting the Ulster Bank

portfolio. The average of individual LTV on new originations was

stable in 2012 at 74% (weighted by value of lending) and 69.4% by

volume (2011 - 67.3%). The volume of business remains very low.

The maximum LTV available to Ulster Bank customers is 90% with

the exception of a specific Northern Ireland scheme which permits

LTVs of up to 95%, in which Ulster Bank’s exposure is capped at

85% LTV.

x Refer to the Ulster Bank Group (Core and Non-Core) section on

page 192 for commentary on mortgage REIL and repossessions.

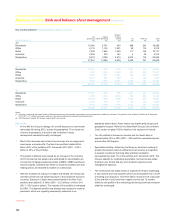

RBS Citizens

x RBS Citizens’ mortgage portfolio totalled £21.5 billion at 31

December 2012, a reduction of 11% from 2011 (£24.2 billion). The

Core business comprises 89% of the portfolio.

x The portfolio comprises £6.2 billion (Core - £5.8 billion; Non-Core -

£0.4 billion) of residential mortgages, of which 1% are in second lien

position. There is also £15.3 billion (Core - £13.3 billion; Non-Core -

£2.0 billion) of home equity loans and lines. Home equity Core

consists of 47% in first lien position while Non-Core consists of 95%

in second lien position.

x RBS Citizens’ lending originates predominantly in the ‘footprint

states’ of New England, Mid Atlantic and Mid West regions. At 31

December 2012, £17.9 billion (83% of the total portfolio) was within

footprint.

x The Non-Core portfolio comprises 11% of the mortgage portfolio

with the serviced by others (SBO) portfolio being the largest

component (75%). The SBO portfolio consists of purchased pools of

home equity loans and lines. The full year charge-off rate was 7.4%

for 2012 (excluding one-time events, the charge-off rate was 6.8%),

which represents a year-on-year improvement (2011 - 8.6%). It is

characterised by out-of-footprint geographies, high (95%) second

lien concentration, and high LTV exposure (111% weighted average

LTV at 31 December 2012). The SBO book has been closed to new

purchases since the third quarter of 2007 and is in run-off, with

exposure down from £2.3 billion at 31 December 2011 to £1.8 billion

at 31 December 2012. The arrears rate of the SBO portfolio has

decreased from 2.3% at 31 December 2011 to 1.9% at 31

December 2012 due primarily to portfolio liquidation (highest risk

borrowers have been charged-off), as well as more effective account

servicing and collections.

x The current weighted average LTV of the mortgage portfolio

decreased from 77% at 31 December 2011 to 75% at 31 December

2012, driven by increases in the Case-Shiller home price index from

the third quarter of 2011 to the third quarter of 2012. The current

weighted average LTV of the mortgage portfolio, excluding SBO, is

71%.

*unaudited