RBS 2012 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

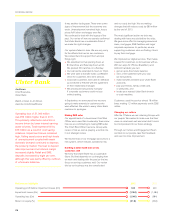

27

RBS GROUP 2012

Making RBS safer

US Retail and Commercial continues to help

make RBS a safer bank. We have delivered

12 straight quarters of operating profit and

improving annual returns on equity. Our capital

position is among the strongest in our peer

group. For the first time since 2008, we were

able to return capital to RBS Group.

We strengthened our balance sheet. Our loan

to deposit ratio was 86% at year end and we

have improved our deposit mix, adding core

checking accounts while reducing more costly

term and time deposits. Wholesale funding

sources are greatly diminished.

Strong risk management remains a top

strategic priority. We have a clearly defined

credit risk appetite, driven by disciplined

underwriting, which has led to consistently

improving credit risk ratios. Asset quality has

improved in all portfolios as evidenced by loss

rates that are near or below pre-crisis levels.

Building a better bank that serves

customers well

In Consumer Banking, our commitment to

customers is clear in the investments we

have made.

We continued to upgrade our ATM network.

The new “Intelligent Deposit Machines”

provide customers with more convenience,

including enhanced deposit capabilities.

We enhanced our online and mobile

services. Our iPhone and Android

applications earned a combined 4.25 out of

5 rating from consumers. We tied for first in a

ratings analysis of 25 large banks

conducted by financial services consulting

firm Javelin Strategy & Research.

Our deposit and credit products help

customers achieve their goals. Through our

branches we opened 455,000 new checking

accounts in 2012.

We believe we can win and deepen customer

relationships by delivering high levels of

service. There is a dedicated team which

continues to improve the customer experience.

This team examines data from customer

surveys, feedback and complaints. This allows

us to identify trends and sources of issues. We

are able to understand what has not worked for

customers and fix it. In one example, customer

feedback led us to cut the wait time between

when we mail a customer’s debit card and the

associated PIN.

We jumped eight spots in 2012 to number 10 in

a survey of bank reputations conducted by

American Banker, an industry publication.

In Commercial Banking, our goal is to help

business customers grow and prosper.

We continue to improve client service and build

strong relationships. The strategy is paying off.

We were lead arranger in 109 deals, up from

83 in 2011. We are now within the top 10

arrangers of middle market syndicated debt

transactions. These deals earned us more than

$52 million in fees compared with $40 million in

2011. We are building our treasury management

capabilities as well. Now, four out of five of our

middle market credit clients also use our cash

management products.

Changing our culture

People lost confidence in banks during the

financial crisis. We have taken steps over the

past few years to strengthen our culture, which

we believe is the foundation of a good bank.

In 2009, we launched our ‘back to basics’

strategy. It keeps us focused on our customers

and what they want and need. Alongside it,

we created a vision, purpose and credo,

emphasizing customers, colleagues

and community.

In 2012, we built on these foundations,

adding five strategic priorities that make it

clearer where we should focus our efforts.

These priorities put ‘back to basics’ in words

that connect with our colleagues.

US Retail &

Commercial

Ellen Alemany

Chief Executive,

Citizens and Head of Americas

Watch or listen to Ellen Alemany

www.rbs.com/AnnualReview

Operating profit of £754 million was

£217 million (40 per cent) higher than in

2011. Total income increased by 2 per cent.

Higher net interest income was driven by

targeted commercial loan growth, deposit

pricing and lower funding costs. Non-

interest income was slightly higher

despite a decline in debit card fees as a

result of the Durbin Amendment legislation,

lower securities fees and lower deposit

fees. Expenses were 3 per cent higher,

largely as a result of one-off items.

Impairments fell sharply, by £235 million

to £91 million. Return on equity was

higher at 8.3 per cent. The loan to deposit

ratio was broadly stable at 86%.

Performance highlights 2012 2011

Operating profit before impairment losses (£m) 845 863

Impairment losses (£m) (91) (326)

Operating profit (£m) 754 537

Return on equity (%) 8.3 6.3