RBS 2012 Annual Report Download - page 155

Download and view the complete annual report

Please find page 155 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

153

Non-traded interest rate risk

Introduction and methodology

Non-traded interest rate risk impacts earnings arising from the Group’s

banking activities. This excludes positions in financial instruments which

are classified as held-for-trading, or hedging items.

The Group provides a range of financial products to meet a variety of

customer requirements. These products differ with regard to repricing

frequency, tenor, indexation, prepayments, optionality and other features.

When aggregated, they form portfolios of assets and liabilities with

varying degrees of sensitivity to changes in market rates.

Mismatches in these sensitivities give rise to net interest income (NII)

volatility as interest rates rise and fall. For example, a bank with a floating

rate loan portfolio and largely fixed rate deposits will see its net interest

income rise, as interest rates rise and fall as rates decline. Due to the

long-term nature of many banking book portfolios, varied interest rate

repricing characteristics and maturities, it is likely the NII will vary from

period to period, even if interest rates remain the same. New business

volumes originated in any period, will alter the interest rate sensitivity of a

bank if the resulting portfolio differs from portfolios originated in prior

periods.

The Group policy is to manage interest rate sensitivity in banking book

portfolios within defined risk limits. With the exception of CFG and

Markets, interest rate risk is transferred from the divisions to Group

Treasury. Aggregate positions are then hedged externally using cash and

derivative instruments, primarily interest rate swaps, to manage

exposures within Group Asset and Liability Management Committee

(GALCO) approved limits.

The Group assesses interest rate risk in the banking book (IRRBB) using

a set of standards to define, measure and report the risk. These

standards incorporate the expected divergence between contractual

terms and the actual behaviour of fixed rate loan portfolios due to

refinancing incentives and the risks associated with structural hedges of

interest rate insensitive balances, which relates to the stability of the

underlying portfolio.

Key measures used to evaluate IRRBB are subject to approval by

divisional Asset and Liability Management Committees (ALCOs) and

GALCO. Limits on IRRBB are proposed by the Group Treasurer for

approval by the Executive Risk Forum annually. Residual risk positions

are reported on a regular basis to divisional ALCOs and monthly to the

Group Balance Sheet Management Committee, GALCO, the Executive

Risk Forum and the Group Board.

The Group uses a variety of approaches to quantify its interest rate risk

encompassing both earnings and value metrics. IRRBB is measured

using a version of the same value-at-risk (VaR) methodology that is used

for the Group’s trading portfolios. Net interest income exposures are

measured in terms of earnings sensitivity over time against movements in

interest rates.

Analyses

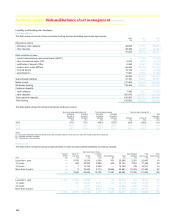

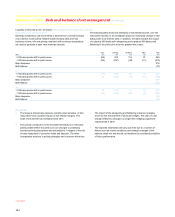

Value-at-risk

VaR metrics are based on interest rate repricing gap reports as at the

reporting date. These incorporate customer products and associated

funding and hedging transactions as well as non-financial assets and

liabilities such as property, plant and equipment, capital and reserves.

Behavioural assumptions are applied as appropriate.

The VaR does not provide a dynamic measurement of interest rate risk

since static underlying repricing gap positions are assumed. Changes in

customer behaviour under varying interest rate scenarios are captured by

way of earnings risk measures. IRRBB VaR for the Group’s Retail and

Commercial banking activities at 99% confidence level and currency

analysis of period end VaR were as follows:

Average Period end Maximum Minimum

£m £m £m £m

2012 46 21 65 20

2011 63 51 80 44

2010 58 96 96 30

2012

£m

2011

£m

2010

£m

Euro 19 26 33

Sterling 17 57 79

US dollar 15 61 121

Other 4 5 10

Key points

x Interest rate exposure at 31 December 2012 was considerably lower

than at 31 December 2011 and average exposure was 27% lower in

2012 than in 2011.

x The reduction in VaR seen across all currencies reflects closer

matching of the Group’s structural interest rate hedges to the

behavioural maturity profile of the hedged liabilities as well as

changes to the VaR methodology (refer to page 244 for more details

on VaR methodology improvement).

x It is estimated that the change in methodology reduced VaR by

£13.8 million (33%) on implementation.