RBS 2012 Annual Report Download - page 245

Download and view the complete annual report

Please find page 245 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

243

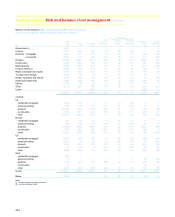

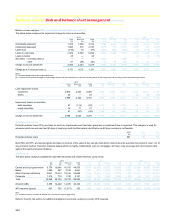

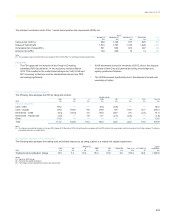

Market risk

Introduction

Market risk arises from fluctuations in interest rates, foreign currency,

credit spreads, equity prices, commodity prices and risk related factors

such as market volatilities. The Group manages market risk within its

trading and non-trading portfolios through a comprehensive market risk

management framework. This control framework includes qualitative and

quantitative guidance in the form of comprehensive policy statements,

dealing authorities, limits based on, but not limited to, value-at-risk (VaR),

stressed VaR (SVaR), stress testing and sensitivity analyses.

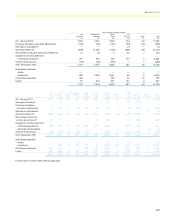

Governance

Business structure

The primary focus of the Group’s trading activities is to provide an

extensive range of financing, risk management and investment services

to its customers, including major corporations and financial institutions

around the world. The Group undertakes these activities organised within

the principal business lines: money markets; rates flow trading;

currencies and commodities; equities; credit markets; and portfolio

management and origination.

Financial instruments held in the Group’s trading portfolios include, but

are not limited to: debt securities; loans; deposits; equities; securities sale

and repurchase agreements and derivative financial instruments.

The Group undertakes transactions in financial instruments that are

traded or cleared on an exchange, including interest rate swaps, futures

and options. Holders of exchange traded instruments provide margin on a

daily basis with cash or other security at the exchange.

The Group also undertakes transactions in financial instruments that are

traded over-the-counter rather than on a recognised exchange. These

instruments range from commoditised transactions in derivative markets,

to trades where the specific terms are tailored to meet customer

requirements.

In 2011, RBS Group announced plans to transfer a substantial part of its

business from RBS N.V. to RBS plc, in an effort to simplify the structure

and reduce risk. During 2012, a substantial part of the business was

transferred to RBS plc. A key element of this was the Financial Services

Authority (FSA) approval of the Netherlands trading branch location into

the scope of the regulatory models.

Organisation structure

Independent oversight and support is provided to the divisions by the

Global Head of Market & Insurance Risk, assisted by the Group and

divisional market risk teams. The head of each division, assisted by a

divisional market risk management team, is accountable for all market

risks associated with its activities. The Global Market Risk Committee

reviews and makes recommendations concerning the market risk profile

across the Group, including risk appetite, risk policy, models,

methodology and market risk development issues. The committee meets

quarterly and is chaired by the Global Head of Market & Insurance Risk.

Attendees include respective divisional market risk managers and Group

Market Risk.

Regulatory Risk

Trading activities will indirectly be impacted by regulatory proposals that

will change market participants behaviours. These are discussed in more

detail in the Regulatory risk section (refer to page 285). Developments

specific to market risk include the Fundamental Review of the Trading

Book (FRTB) and the Fundamental Review of the Securitisation

Treatments. The FRTB remains at a conceptual stage and there is

currently insufficient practical detail available to provide a meaningful

assessment of what may eventually be implemented. The Basel

Committee's review of the treatment of securitisation positions is further

advanced and the Group is currently reviewing how it can participate to

assess the impact on trading book activities.

Risk measurement

Key principles

The Group’s qualitative market risk appetite is set out in policy

statements, which outline the governance, responsibilities and

requirements surrounding the identification, measurement, analysis,

management and communication of market risk arising from the trading

and non-trading investment activities of the Group. All teams involved in

the management and control of market risk are required to fully comply

with the policy statements to ensure the Group is not exposed to market

risk beyond the qualitative and quantitative risk appetite. The control

framework covers the following principles:

x Clearly defined responsibilities and authorities for the primary

groups involved in market risk management in the Group;

x An independent market risk management process;

x Daily monitoring, analysis and reporting of market risk exposures

against market risk limits;

x Clearly defined limit structure and escalation process in the event of

a market risk limit excess;

x A market risk measurement methodology that captures correlation

effects and allows aggregation of market risk across risk types,

markets and business lines;

x Use of VaR as a measure of the one-day and SVaR as a measure

of the ten-day market risk exposure of all trading positions;

x Use of non-VaR based limits and other controls;

x Use of stress testing and scenario analysis to support the market

risk measurement and risk management process by assessing how

portfolios and global business lines perform under extreme market

conditions;

x Use of back-testing as a diagnostic tool to assess the accuracy of

the VaR model and other risk management techniques;

x Adherence to the risks not in VaR framework to identify, quantify

and capitalise risks not captured within the VaR model; and

x A product approval process that requires market risk teams to

assess and quantify market risk associated with proposed new

products.

Business review Risk and balance sheet management continued