RBS 2012 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

213

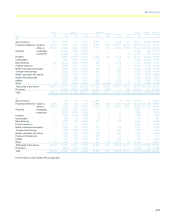

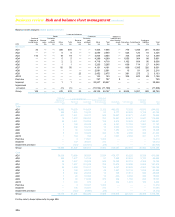

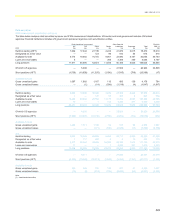

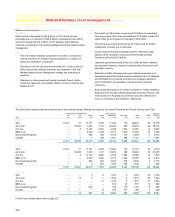

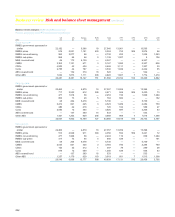

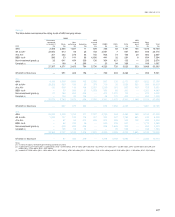

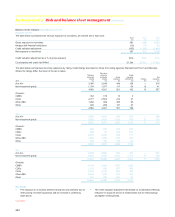

Asset-backed securities

Introduction

The Group structures, originates, distributes and trades debt in the form

of loan, bond and derivative instruments in all major currencies and debt

capital markets in North America, Western Europe, Asia and major

emerging markets. The carrying value of the Group's debt securities is

detailed below.

The Group’s credit market activities gave rise to risk concentrations in

asset-backed securities (ABS). The Group has exposures to ABS, which

are predominantly debt securities, but can also be held in derivative form.

ABS have an interest in an underlying pool of referenced assets. The

risks and rewards of the referenced pool are passed onto investors by the

issue of securities with varying seniority by a special purpose entity.

Debt securities include residential mortgage-backed securities (RMBS),

commercial mortgage-backed securities (CMBS), collateralised debt

obligations (CDOs), collateralised loan obligations (CLOs) and other

ABS. In many cases, the risk associated with these assets is hedged by

credit derivatives. The counterparties to some of these hedge

transactions are monoline insurers.

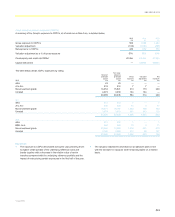

The following tables summarise the gross and net exposures and

carrying values of these securities by the location of the underlying

assets at 31 December 2012, 2011 and 2010 and by IFRS measurement

classification of held-for-trading (HFT), designated at fair value (DFV),

available-for-sale (AFS) and loans and receivables (LAR). Gross

exposures represent the principal amounts relating to ABS. Government

sponsored or similar RMBS comprises securities that are: (a) guaranteed

or effectively guaranteed by the US government, by way of its support for

US federal agencies and government sponsored enterprises or (b)

guaranteed by the Dutch government. Net exposures represent the

carrying value after taking account of protection purchased from monoline

insurers and other counterparties, but exclude the effect of counterparty

credit valuation adjustments. The hedge provides credit protection of both

principal and interest cash flows in the event of default by the

counterparty. The value of this protection is based on the underlying

instrument being protected.

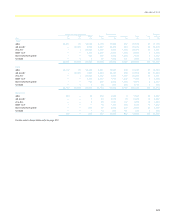

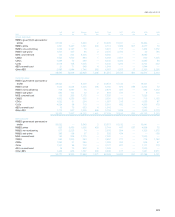

Residential mortgage-backed securities

RMBS are securities that represent an interest in a portfolio of residential

mortgages. Repayments made on the underlying mortgages are used to

make payments to holders of the RMBS. The risk of the RMBS will vary

primarily depending on the quality and geographic region in which the

underlying mortgage assets are located and the credit enhancement of

the securitisation structure. Several tranches of notes are issued, each

secured against the same portfolio of mortgages, but providing differing

levels of seniority to match the risk appetite of investors. The most junior

(or equity) notes will suffer early capital and interest losses experienced

by the referenced mortgage collateral, with each more senior note

benefiting from the protection provided by the subordinated notes below.

Additional credit enhancements may be provided to the holder of senior

RMBS notes, including provided by monoline insurers.

The main categories of mortgages that serve as collateral to RMBS held

by the Group with related vintages are set out below and described in the

Glossary on pages 528 to 535. The US market has more established

definitions of differing underlying mortgage quality and these are used as

the basis for the Group's RMBS categorisation.

The Group RMBS classifications include sub-prime and non-conforming.

Non-conforming RMBS include Alt-A RMBS. Classification as sub-prime

or Alt-A is based on Fair Isaac Corporation scores (FICO), level of

documentation and loan-to-value (LTV) ratios of the underlying mortgage

loans. RMBS are classified as sub-prime if the mortgage portfolio

comprises loans with FICO scores between 500 and 650 with full or

limited documentation. Mortgages in Alt-A RMBS portfolios have FICO

scores of 640 to 720, limited documentation and an original LTV of 70%

to 100%.