RBS 2012 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

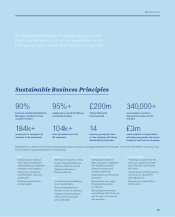

2012 Results

2012 saw landmark achievements in our

restructuring plan. It saw sustained customer

lending support. A 61% share price rise during

the year (and 215% versus the January 2009

low point) underlined an improvement of

investor belief in our future and that of the

banking sector generally.

The critical task of financial stabilisation

passed milestones as RBS recommenced

preference share dividends, completed

the repayment of all crisis liquidity facilities

from public authorities and exited the UK

Government £282 billion Asset Protection

Scheme without making any claim under it.

The notable flotation of Direct Line Group

represented the third of four EU state aid

conditions and offset the disappointment

of Santander withdrawing from its agreed

purchase of 315 branches from RBS.

Underlining this progress, RBS 5 year bonds

traded at c.1% credit spreads compared to

their wide levels earlier in the year of c.4.5%.

The resultant own-credit accounting charge of

£4.6 billion reflects this huge improvement in

the perceived credit quality of RBS.

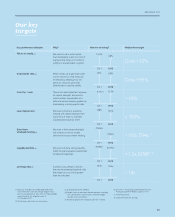

Core Bank operating profits were £6.3 billion of

which Retail and Commercial businesses were

£5.3 billion (excluding Ulster Bank) and

Markets £1.5 billion. Non-Core losses declined

again (32% to £2.9 billion) and Non-Core

assets also fell ahead of target to £57 billion.

We expect to slow the pace and cost of the

remaining run-down once we hit the £40 billion

asset target for the end of 2013. Exceptional

charges in relation to Payment Protection

Insurance claims, LIBOR settlements and

interest rate hedging product redress, together

with the own credit adjustment, resulted in a

loss before tax of £5,165 million.

In a tough economic environment, most of the

banking industry’s ongoing businesses are

running hard to stand still, and so it was at

RBS. But the existing level of operating

performance is essential to fund our historic

clean-up with the moment coming ever closer

when these costs are behind us and rewards

flow directly once more to shareholders.

Reputation

Our industry faces a tough challenge rebuilding

its reputation. 2012 was a wrenching year on

that front as the cultural clean-up came to the

fore which was always a companion to physical

changes required from pre-crisis times.

Expectations are changing fast and even past

ones have not been lived up to often enough.

And the mistakes of some, grievous in cases,

are tainting the efforts of the majority of bank

staff. Most banks have past failings on a range

of fronts. For RBS the two worst in the past year

were LIBOR and our IT incident - quite different

though they are.

There is no single solution or dramatic action

able to address this problem. The best

companies in the world in any industry develop,

almost as part of their DNA, the consistent

commitment to serve customers well and act

accordingly. Our sights are set here. The facts

and the culture that drives them will be

established one piece at a time across many

many issues. But we have no higher priority.

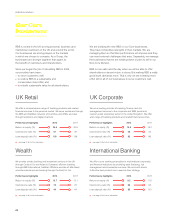

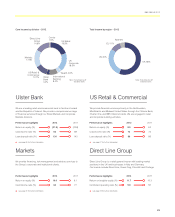

Strategy

The new RBS is a leading UK bank anchored in

retail and commercial business lines. Our

businesses are shaped around customer

needs with substantial competitive strengths in

their respective fields. Each unit is being

retooled to provide improved and enduring

performance and to meet new external

challenges. We sustain strong capabilities

internationally and in financial markets to

support the needs of our customers and

shareholders. Our businesses are managed to

add value in their own right but to provide a

stronger, more balanced and valuable whole

through vital cross-business linkages.

The physical weaknesses uncovered by the

financial crisis - of leverage, risk concentration

and business stretch - are close to being fixed.

RBS’s total assets have already been reduced

by £906 billion from their peak in 2008 - more

than any other entity worldwide has achieved.

The principles behind this strategy are sound

and working. But it will continue to evolve. A

much slower economic recovery and tougher

set of regulatory and policy pressures need to

be absorbed. We have done this with more

emphasis on customer service, balance sheet

conservatism and while asking staff to do more

with less during a period of significant change.

Our business ambitions have been trimmed as

a necessary reaction.

But whatever the outside conditions and

evolution of strategy we are clear about the

interrelated nature of our priorities. To serve

customers well, run only prudent risk and

reward shareholders over the longer term.

In this context we have set a new medium-term

target for our Markets business, which is an

important part of our service to corporate and

institutional customers. We aim to further

reduce its scale and scope, targeting capital

consumption of £80 billion RWAs whilst

sustaining the service provided to our

customer base.

Additionally, the Board has decided it is now

the right time to begin work on a partial flotation

of Citizens, our US banking business, targeted

probably at around 2 years from now. Citizens

is a good business, serving around 5 million

customers in the north east of the United

States where it is has a strong market position.

It has been substantially improved since 2009

and a local public listing will help to highlight its

growing value. This provides a positive

opportunity for Citizens and its 14,700

employees, as well as being a sensible move

for RBS as a whole.

People

The banking industry has come down to earth

hard. While a more balanced global economy

has clear merits, the changes, pressures and

adjustments asked of our people remain high.

And successful results are vital for the many

who rely on us. The engagement, dedication

and professionalism of RBS employees

remains outstanding and has much to be

commended.

Concluding remarks

RBS is coming through an immense and

wrenching restructuring. Much has been

achieved and that should underpin our energy

for what remains. Much is already good about

our Core business, how it serves customers,

how it performs. Our ambition is to be a really

good bank – for all our stakeholders. Simple to

say. A lot still to do. Many will benefit from our

achieving that goal.

I thank our staff and all our stakeholders for

their continued support in this effort.

Stephen Hester

Group Chief Executive

13

RBS GROUP 2012