RBS 2012 Annual Report Download - page 161

Download and view the complete annual report

Please find page 161 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

159

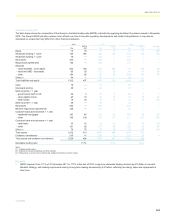

Shipping

The downturn observed in the shipping sector since 2008 has continued,

with an oversupply of vessels leading to lower asset prices and charter

rates. The Group has continued to manage exposures within this portfolio

intensively, with an increasing number of customers managed under the

Group’s Watchlist process (see page 172 for a description of this

process). The financed fleet comprises modern vessels with experienced

operators and despite the difficult market conditions impairments to date

have remained low. However, impairment levels remain vulnerable to a

continuing underperforming market.

Further details on the Group’s shipping portfolio can be found on page

166.

Retailers

Given the cyclical nature of the retail corporate sector and its sensitivity to

stressed economic conditions, the Group has continued to apply

heightened scrutiny to this portfolio. Despite some high-profile failures of

UK high street retailers, loss experience on the RBS retail portfolio

remained low during 2012 as a result of active management. The

portfolio is generally well diversified by geography and by counterparty.

Central counterparties (CCPs)

New regulation requiring greater use of CCPs for clearing over-the-

counter derivatives across the industry is aimed at reducing systemic risk

in the banking sector. RBS welcomes this move but recognises that the

Group’s concentration risk to CCPs will rise; thus exchanging

concentration risk to individual counterparties for concentration risk to

CCPs. CCPs are vulnerable to a significant member default, fraud and

increased operational risk if their infrastructure and collateral

management approaches are not developed commensurate with

increased activity they undertake.

In response to this industry change, the Group has developed a tailored

risk appetite and risk control framework. The Group’s central counterparty

exposure is dominated by a small number of well-established, high

quality and reputable clearing houses.

Renegotiations and forbearance

Loan modifications take place in a variety of circumstances including but

not limited to a customer’s current or potential credit deterioration. Where

the contractual payment terms of a loan have been changed because of

the customer’s financial difficulties, it is classified as ‘renegotiated’ in the

wholesale portfolio and as ‘forbearance’ in the retail portfolio.

RBS uses renegotiations and forbearance as management tools to

support viable customers through difficult financial periods in their lives or

during business cycles. Used wisely, they can reduce the incidence of

personal insolvency, as well as bankruptcies for otherwise successful

enterprises. On a broader scale they can also help reduce the impact of

“fire sale” pricing on real economic assets. However, they must be used

selectively and require additional management vigilance throughout the

loan life cycle. The Group has continued to take steps to improve its

management and reporting of such loans within both corporate and retail

businesses. More details of the Group’s approach can be found on pages

173 to 180.

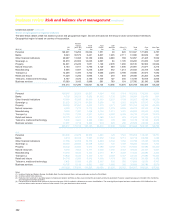

Objectives, organisation and governance

The existence of a strong credit risk management function is vital to

support the ongoing profitability of the Group. The potential for loss

through economic cycles is mitigated through the embedding of a robust

credit risk culture within the business units and through a focus on the

importance of sustainable lending practices. The role of the RBS credit

risk management function is to own the credit approval, concentration

and credit risk control frameworks and to act as the ultimate authority for

the approval of credit. This, together with strong independent oversight

and challenge, enables the business to maintain a sound lending

environment within approved risk appetite.

Responsibility for development of, and compliance with, Group-wide

policies and credit risk frameworks and Group-wide assessment of

provision adequacy resides with the Group Credit Risk (GCR) function

under the management of the Group Chief Credit Officer. Execution of

these policies and frameworks is the responsibility of the risk

management functions, located within the Group’s business divisions.

The divisional credit risk management functions work together with GCR

to ensure that the risk appetite set by the Group Board is met, within a

clearly defined and managed control environment. The credit risk function

within each division is managed by a Chief Credit Officer, who reports

jointly to a divisional Chief Risk Officer and to the Group Chief Credit

Officer. Divisional activities within credit risk include credit approval,

transaction and portfolio analysis, ongoing credit risk stewardship, and

early problem recognition and management.

Material aspects of the Group’s credit risk management framework, such

as credit risk appetite and limits for portfolios of strategic significance, are

considered and approved by the Executive Risk Forum (ERF). The ERF

has delegated approval authority to the Group Credit Risk Committee, a

functional sub-committee of the Group Risk Committee, to act on credit

risk matters. These include, but are not limited to, credit risk appetite and

limits (within the overall risk appetite set by the Board and the ERF),

credit risk strategy and frameworks, credit risk policy and the oversight of

the credit profile across the Group.

The Group Credit Risk Committee is chaired by the Group Chief Credit

Officer and has representation from each of the Group’s divisional credit

risk functions. Monthly updates are provided to the Group Risk

Committee on key matters approved under delegated authority by the

Group Credit Risk Committee, performance against limits, and emerging

issues, to enable it to fulfil its role as an oversight committee.

Oversight of the Group’s provision adequacy is provided by the Group

Audit Committee.

Key trends in the credit risk profile of the Group, performance against

limits and emerging risks are set out in the RBS Risk Management

Monthly Report provided to the Group Board, the Executive Committee

and the Board Risk Committee.