RBS 2012 Annual Report Download - page 256

Download and view the complete annual report

Please find page 256 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

254

Business review Risk and balance sheet management continued

Country risk continued

Governance, monitoring and management*

The Group’s country risk framework is set by the Executive Risk Forum

(ERF), which has delegated authority to the Group Country Risk

Committee (GCRC) to manage exposures within the framework and deal

with any limit breaches, with escalation where needed to ERF. Under this

framework, exposures to all countries are monitored. Countries with

material exposures are included in the Group’s country risk Watchlist

process to identify emerging issues and facilitate the development of

mitigation strategies. Detailed portfolio reviews are undertaken on a

regular basis to ensure that country portfolio compositions remain aligned

to the Group’s country risk appetite in light of evolving economic and

political developments.

Limits on total exposure are set for individual countries based on a risk

assessment taking into account the country’s economic and political

situation and outlook, as well as the Group’s portfolio composition in that

country. Sub-limits are set on medium-term (greater than one year)

exposure since this exposure can, by nature, not be reduced as rapidly

as short-term exposure in the event of deterioration of a country’s

creditworthiness.

During 2012, in addition to all emerging markets and the vulnerable

eurozone countries, the Group brought nearly all advanced countries

under country limits. The exceptions were the UK (and related European

special territories of Guernsey, Jersey, the Isle of Man and Gibraltar) and

the US, given their home country status.

Also in 2012, an enhanced country risk appetite framework was

introduced. The Group’s risk appetite for a particular country is now

guided by global risk appetite, the country’s internal rating and strategic

importance to the Group, the portfolio composition by tenors and clients,

an assessment of the potential for losses arising from a number of

possible key country risk events, and other country-specific

considerations such as funding profile, risk/return analysis, business

opportunities and reputational risk. The actual country limits continue to

be set by GCRC (or the ERF above certain benchmark levels).

Further enhancements included improved divisional country risk

operating models and the implementation of a new sovereign rating

model.

Eurozone crisis preparedness

A Group executive steering group is driving eurozone crisis

preparedness. Its agenda in 2012 included operational preparations for

possible sovereign defaults and/or eurozone exits. The steering group

also considered initiatives to determine and reduce redenomination risk.

Further actions to mitigate risks and strengthen control in the eurozone

typically included taking guarantees or insurance, updating collateral

agreements, and tightening certain credit pre-approval processes.

Redenomination risk

The overall impact of redenomination risk on the Group is difficult to

determine with certainty, but would be shaped by: the scope and reach of

any new legislation introduced by an exiting country; its applicability to

the facility documentation; and whether there are any appropriate offsets

to the exposures. For the purposes of estimating funding mismatches at

risk of redenomination (detailed below), the Group takes, as its starting

point balance sheet exposure as defined on page 255 and excludes

exposures at low risk of redenomination. The latter are identified through

consideration of the relevant documentation, particularly the currency of

exposure, governing law, court of jurisdiction, precise definition of the

contract currency (for euro facilities), and location of payment. The Group

also deducts offsets for provisions taken and liabilities that would be

expected to redenominate at the same time.

A redenomination event would also be accompanied by increased credit

risk, for two reasons. First, capital controls would likely be introduced in

the affected country, resulting in any non-redenominated assets,

including non-euro assets, potentially becoming harder to service.

Second, a sharp devaluation could imply payment difficulties for

counterparties with large debts denominated in foreign currency and

counterparties that are heavily dependent on imports.

The Group's focus continues to be on reducing its asset exposures and

funding mismatches in the eurozone periphery countries. During 2012,

total asset exposures to these countries decreased by 13% to

£59.1 billion. The estimated funding mismatch at risk of redenomination

was £9.0 billion for Ireland, £4.5 billion for Spain, and £1.0 billion for Italy

at 31 December 2012. These mismatches can fluctuate due to volatility in

trading book positions and changes in bond prices. The net positions for

Greece, Portugal and Cyprus were all minimal.

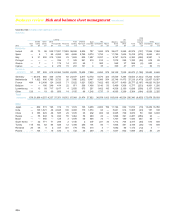

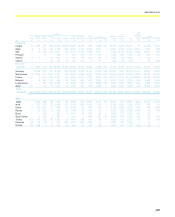

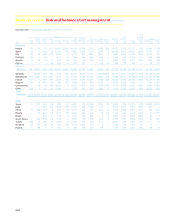

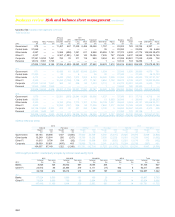

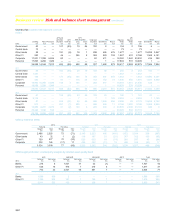

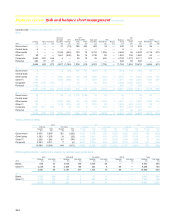

Refer to pages 256 to 280 for discussion on the Group’s exposure to

banks, financial institutions and other sectors in a number of eurozone

countries.

Credit default swaps

The Group uses credit default swap (CDS) contracts to service customer

activity as well as to manage counterparty and country exposure. The

latter is done to hedge portfolios or specific exposures. This may give rise

to maturity mismatches between the underlying exposure and the CDS

contract, as well as between bought and sold CDS contracts on the same

reference entity. CDS positions are monitored on a daily basis as part of

regular market risk management.

The terms of the Group’s CDS contracts are covered by standard

International Swaps and Derivatives Association (ISDA) documentation,

which determines if a contract is triggered due to a credit event. Such

events may include bankruptcy or restructuring of the reference entity or

a failure of the reference entity to repay its debt or interest. Under the

terms of a CDS contract, one of the regional Credit Derivatives

Determinations Committees of the ISDA is empowered to decide whether

or not a credit event has occurred.

The Group transacts CDS contracts primarily on a collateralised basis

with investment-grade global financial institutions who are active

participants in the CDS market. These transactions are subject to regular

margining, which usually takes the form of cash collateral. For European

peripheral sovereigns, credit protection has been purchased from a

number of major European banks, predominantly outside the country of

the reference entity. In a few cases where protection was bought from

banks in the country of the reference entity, giving rise to wrong-way risk,

this risk is mitigated through specific collateralisation and monitored on a

weekly basis.

*unaudited