RBS 2012 Annual Report Download - page 180

Download and view the complete annual report

Please find page 180 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

178

Business review Risk and balance sheet management continued

Early problem identification and problem debt management: Retail customers continued

Key points

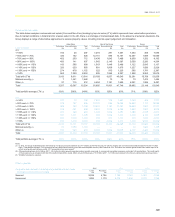

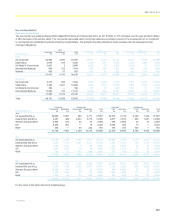

UK Retail

x The reported numbers for forbearance in UK Retail capture all

instances where a change has been made to the contractual

payment terms including those where the customer is up-to-date on

payments and there is no obvious evidence of financial stress. The

reported figures include stock dating back to 1 January 2008.

x At 31 December 2012, stock levels of £4.8 billion represent 4.9% of

the total mortgage assets; this represents a 9.2% increase in

forbearance stock since 31 December 2011. Of these,

approximately 83% were up-to-date with payments (compared with

approximately 97% of the mortgage population not subject to

forbearance activity). The flow of forbearance arrangements has

remained stable year on year.

x The most frequently occurring forbearance types were term

extensions (47% of assets subject to forbearance at 31 December

2012), interest only conversions (25%) and capitalisations of arrears

(19%). The stock of cases subject to interest only conversions

reflects legacy policy. In 2009, UK Retail ceased providing this type

of forbearance treatment for customers in financial difficulty and no

longer permits interest only conversions on residential mortgages

where the customer is current on payments.

x The provision cover on performing assets subject to forbearance

was about five times that on assets not subject to forbearance.

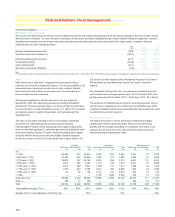

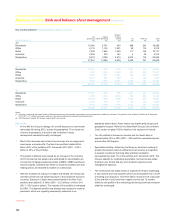

Ulster Bank

x The reported numbers for forbearance in Ulster Bank Group capture

all instances where a change has been made to the contractual

payment terms including those where the customer is up-to-date on

payments and there is no obvious evidence of financial stress. The

reported figures include stock dating back to early 2009.

x Ulster Bank Group continues to assist customers in the difficult

economic environment. Mortgage forbearance treatments have

been in place since 2009 and are aimed at assisting customers in

financial difficulty. At 31 December 2012, 10.4% of total mortgage

assets (£1.9 billion) were subject to a forbearance arrangement, an

increase from 9.1% (£1.8 billion) at 31 December 2011. The majority

of these forbearance arrangements were in the performing book

(73%).

x The majority of forbearance arrangements offered by Ulster Bank

currently are temporary concessions, accounting for 85% of assets

subject to forbearance at 31 December 2012. These are offered for

periods of one to three years and incorporate different levels of

repayment based on the customer’s ability to pay. The additional

treatment options developed by Ulster Retail will lead to a shift to

more long term arrangements over time.

x Of these temporary forbearance types, the largest category at 31

December 2012 was interest only conversions, which accounted for

46% of total assets subject to forbearance. The other categories of

temporary forbearance were payment concessions: reduced

repayments (36%); and payment holidays (3%).

x The flow by forbearance type remained stable when compared with

2011 and there was a modest reduction, 3%, in customers seeking

assistance for the first time year on year.

x The provision cover on performing assets subject to forbearance is

approximately eight times higher than that on performing assets not

subject to forbearance.