RBS 2012 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

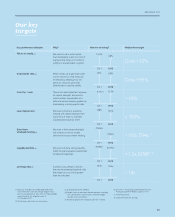

16

OUR BUSINESS AND OUR STRATEGY

Progress on our Strategic Plan

Strategy and business objectives

Strategy and business objectives

RBS to deliver its strategy from a stable risk profile and

balance sheet, with each banking business self-funding

(1:1 loan:deposit ratio)

How are we going to do this?

Reduced balance sheet scale

Continue to de-risk and shrink our Non-Core balance sheet.

Careful control of future asset growth to support Core

customers’.

Funding programme

Limit over-reliance on wholesale markets to meet the

Group’s funding requirements, while building up an

appropriate liquidity reserve. Generate a stable deposit

base to fund each business.

Stable and robust capital support

Focus on implementing state of the art risk controls, run-off

of excess risk concentrations and maintenance of strong

equity capital.

Our progress so far

The Group’s funded balance sheet was further managed down

to £870 billion by the end of 2012. Non-Core and M&IB have

driven the deleveraging to date, with Non-Core’s funded balance

sheet standing at £57 billion, 22% of its starting point in 2008

and ahead of target for the year.

Throughout the restructuring process we have been able to

shrink our assets while sustaining a strong capital base.

Our Tier 1 leverage ratio of 15.0x times in 2012 comfortably met

our target.

Our Core bank continued to take in more than £1 of deposits for

every £1 of loans made in 2012 with a loan to deposit ratio of

90%. The Group met its target of 100% loan to deposit ratio at

the end of 2012.

Our reliance on short-term wholesale funding has been

further reduced to £42 billion or 5% of funded assets.

We had an excess of liquidity in 2012 with liquidity reserves of

£147 billion, or 3.5x our short-term wholesale funding,

surpassing our target.

In 2012, we passed a major milestone in our capital story when

we exited the Asset Protection Scheme (“APS”), the Government

scheme we entered in 2009 to provide capital relief and

insurance against the possibility of a further significant

deterioration in credit losses. Now, even without the benefit of

APS, we have maintained a Core Tier 1 capital ratio of 10.3%,

above our target.

Our capital ratio meets regulatory requirements well ahead of the

internationally agreed implementation timeline and shows that

the Group has sufficient capital to deal with future requirements.

Medium-term target

Group leverage ratio <18x

Group loan:deposit ratio of 100%

Short-term wholesale funding <10% of third party assets

Liquidity portfolio >1.5x short-term wholesale funding

Core Tier 1 capital ratio >10%

Strategy and business objectives

RBS to be based on enduring customer franchises with each business

capable of generating a sustainable return in excess of its cost of capital

How are we going to do this?

Franchises with substantial competitive strength

Track market positions and customer satisfaction in all Core businesses

Income growth

Focus on businesses capable of delivering sustainable growth and achieve

market-level growth in each

Cost control

Deliver on the Group’s cost programmes, whilst making essential investments in

our businesses. Achieve a cost:income ratio that places RBS among the most

efficient of its global peers.

Rigorous capital and cost allocation

Accurately deploy the Group’s capital and allocate appropriate costs to focus

the divisions on sustainable returns, as well as on profit growth.

Our progress so far

Our goal is for the new RBS to be built upon customer-driven businesses

with substantial competitive strengths in their respective markets. We have

top tier competitive positions across all of our enduring customer franchises.

We continue to monitor closely and drive improvements in our customer

satisfaction scores.

Achieving growth continues to be a major challenge in our operating

environment. Put simply, if our customers are not growing, we will not grow.

We have restructured and invested in our ongoing businesses to serve our

customers better and deliver improved and enduring performance. We believe

there is additional upside to these franchises when economic recovery

takes hold.

So far, through our cost reduction programme, we have taken £3.6 billion

annualised out of our cost base. This, along with lower than originally projected

programme spend, has allowed us to invest in our Core franchises in order to

enhance our customer service and product offerings through improvements to

our technology and infrastructure.

In 2012 our Core cost:income ratio of 59% showed a further improvement

towards our target.

We use direct service usage, requirement for market funding and other

appropriate drivers to allocate costs accurately to the divisions. Capital is

allocated with a focus on sustainable risk-adjusted returns rather than short-term

performance prospects. This gives our divisions a realistic view of how their

income translates into profits and returns. In 2012, the only Core business that

was materially short of earning its cost of capital was Ulster Bank, although a

number of our other businesses have some work to do to improve their returns.

Core return on equity in 2012 was 9.8%, reflecting protracted economic

challenges in the areas in which we operate.

Medium-term target

All our principal Core businesses sustain positions amongst the leaders in

their chosen fields.

Core cost:income ratio <55%

Core return on equity >12%

Group leverage ratio <18x