RBS 2012 Annual Report Download - page 192

Download and view the complete annual report

Please find page 192 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

190

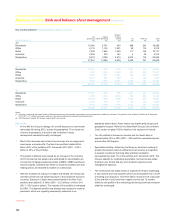

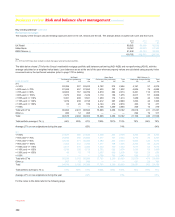

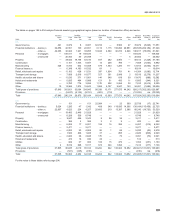

Business review Risk and balance sheet management continued

Key credit portfolios* continued

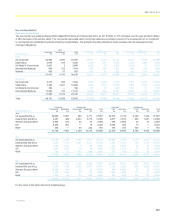

Ulster Bank Group (Core and Non-Core)

Overview

At 31 December 2012, Ulster Bank Group accounted for 10% of the

Group’s total gross loans to customers (2011 and 2010 - 10%) and 8% of

the Group’s Core gross loans to customers (2011 - 8%; 2010 - 9%).

Ulster Bank’s financial performance continues to be overshadowed by the

challenging economic climate in Ireland, with impairments remaining

elevated as high unemployment, coupled with higher taxation and limited

liquidity in the economy, continues to depress the property market and

domestic spending.

The impairment charge of £2,340 million for 2012 (2011 - £3,717 million;

2010 - £3,843 million) was driven by a combination of new defaulting

customers and higher provisions on existing defaulted cases due

primarily to deteriorating security values. Provisions as a percentage of

risk elements in lending increased from 53% in 2011, to 57% in 2012,

predominantly as a result of the deterioration in the value of the Non-Core

commercial real estate development portfolio. Ulster Bank impairment

provisions take into account recovery strategies for its commercial real

estate portfolio, as currently there is very limited liquidity in Irish

commercial and development property.

Core

The impairment charge for the year of £1,364 million (2011 - £1,384

million; 2010 - £1,161 million) reflects the difficult economic climate in

Ireland, with elevated default levels across both mortgage and other

corporate portfolios. The mortgage sector accounted for £646 million

(47%) of the total 2012 impairment charge.

Non-Core

The impairment charge for the year was £976 million, a decrease of

£1,357 million (2011 - £2,333 million; 2010 - £2,682 million), with the

commercial real estate sector accounting for £899 million (92%) of the

total 2012 impairment charge.

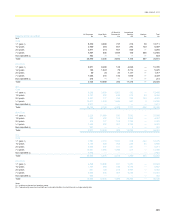

Credit metrics

Gross

loans REIL Provisions

REIL

as a % of

gross loans

Provisions

as a % of

REIL

Provisions

as a % of

gross loans

Impairment

charge

Amounts

written-off

Sector analysis £m £m £m % % % £m £m

2012

Core

Mortgages 19,162 3,147 1,525 16.4 48 8.0 646 22

Commercial real estate

- investment 3,575 1,551 593 43.4 38 16.6 221 —

- development 729 369 197 50.6 53 27.0 55 2

Other corporate 7,772 2,259 1,394 29.1 62 17.9 389 15

Other lending 1,414 207 201 14.6 97 14.2 53 33

32,652 7,533 3,910 23.1 52 12.0 1,364 72

Non-Core

Commercial real estate

- investment 3,383 2,800 1,433 82.8 51 42.4 288 15

- development 7,607 7,286 4,720 95.8 65 62.0 611 103

Other corporate 1,570 1,230 711 78.3 58 45.3 77 23

12,560 11,316 6,864 90.1 61 54.6 976 141

Ulster Bank Group

Mortgages 19,162 3,147 1,525 16.4 48 8.0 646 22

Commercial real estate

- investment 6,958 4,351 2,026 62.5 47 29.1 509 15

- development 8,336 7,655 4,917 91.8 64 59.0 666 105

Other corporate 9,342 3,489 2,105 37.3 60 22.5 466 38

Other lending 1,414 207 201 14.6 97 14.2 53 33

45,212 18,849 10,774 41.7 57 23.8 2,340 213

*unaudited