RBS 2012 Annual Report Download - page 172

Download and view the complete annual report

Please find page 172 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

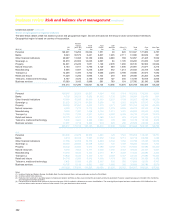

Credit risk mitigation continued

Wholesale market exposures

As set out in the table below, the Group receives collateral for reverse repurchase transactions and for derivatives, typically in the form of cash, quoted

debt securities or equities. The risks inherent in both types of transaction are further mitigated through master bilateral netting arrangements. Industry

standard documentation such as master repurchase agreements and credit support annexes accompanied by legal opinion, is used for financial

collateral taken as part of trading activities.

2012 2011 2010

£bn £bn £bn

Reverse repurchase agreements 104.8 100.9 95.1

Securities received as collateral (1) (104.7)(98.9)(94.3)

Derivative assets gross exposure 441.9 530.1 432.2

Counterparty netting (373.9)(441.6)(330.4)

Cash collateral held (34.1) (37.2) (31.1)

Securities received as collateral (5.6)(5.3)(2.9)

Note:

(1) In accordance with normal market practice, at 31 December 2012 £100.7 billion (2011 - £95.4 billion; 2010 - £93.5 billion) had been resold or re-pledged as collateral for the Group’s own transactions.

Retail

Within the Group’s retail book, mortgage and home equity lending

portfolios are secured by residential property. The Group’s portfolio of US

automobile loans is secured by motor cars or other vehicles. Student

loans and credit card lending are all unsecured. The vast majority of

personal loans are also unsecured.

All borrowing applications, whether secured or not, are subject to

appropriate credit risk underwriting processes including affordability

assessment. Pricing is typically higher on unsecured than secured loans.

For secured loans, pricing will typically vary by LTV. Higher LTV products

are typically subject to higher interest rates commensurate with the

associated risk.

The value of a property intended to secure a mortgage is assessed

during the loan underwriting process using industry-standard

methodologies. Property values supporting home equity lending reflect

either an individual appraisal or valuations generated by statistically valid

automated valuation models. Property values are updated each quarter

using the relevant house price index (the Halifax Quarterly Regional

House Price Index in the UK, the Case-Shiller Home Value Index in the

US, and the Central Statistics Office Residential Property Price Index in

ROI (monthly) and the Nationwide House Price Index in Northern

Ireland).

For automobile lending in the US, new vehicles are valued at cost and

used vehicles at the average trade-in value. At 31 December 2012, this

portfolio amounted to £5.4 billion (2011 - £4.8 billion; 2010 - £5.1 billion).

The existence of collateral has an impact on provisioning levels. Once a

secured loan is classified as non-performing, the realisable value of the

underlying collateral and the costs associated with repossession are used

to estimate the provision required.

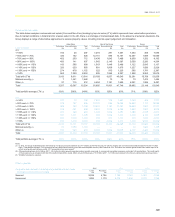

Residential mortgages

The table below shows LTVs for the Group’s residential mortgage

portfolio split between performing (AQ1-AQ9) and non-performing

(AQ10), with the average calculated on a weighted value basis. Loan

balances are as at the end of the year whereas property values are

calculated using the appropriate index.

UK Retail Ulster Bank RBS Citizens (1)

Loan-to-value Performing

£m

Non-performing

£m

Total

£m

Performing

£m

Non-performing

£m

Total

£m

Performing

£m

Non-performing

£m

Total

£m

2012

<= 50% 22,306 327 22,633 2,182274 2,456 4,167 51 4,218

> 50% and <= 70% 27,408 457 27,865 1,635 197 1,832 4,806 76 4,882

> 70% and <= 90% 34,002 767 34,769 2,019294 2,313 6,461 114 6,575

> 90% and <= 100% 7,073 366 7,439 1,119156 1,275 2,011 57 2,068

> 100% and <= 110% 3,301 290 3,591 1,239 174 1,413 1,280 43 1,323

> 110% and <= 130% 1,919 239 2,158 2,412 397 2,809 1,263 42 1,305

> 130% and <= 150% 83 26 109 2,144 474 2,618 463 14 477

> 150% — — — 3,156 1,290 4,446 365 14 379

Total with LTVs 96,092 2,472 98,564 15,9063,256 19,162 20,816 411 21,227

Other (2) 486 12 498 — — — 292 19 311

Total 96,578 2,484 99,062 15,9063,256 19,162 21,108 430 21,538

Total portfolio average LTV (3) 66% 80% 67% 108% 132% 112% 75% 86% 75%

Average LTV on new originations during the year 65% 74% 64%

170

Business review Risk and balance sheet management continued