RBS 2012 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

138

Business review Risk and balance sheet management continued

Liquidity, funding and related risks

Introduction

Liquidity risk is the risk that the Group is unable to meet its financial

obligations, including financing wholesale maturities or customer deposit

withdrawals, as and when they fall due. Liquidity risk is highly dependent

on company specific characteristics such as the maturity profile and

composition of the Group’s assets and liabilities, the quality and

marketable value of its liquidity buffer and broader market factors, such

as wholesale market conditions alongside depositor and investor

behaviour.

Safety and soundness of the balance sheet is one of the central pillars of

the Group’s restructuring strategy. Effective management of liquidity risk

is central to the safety and soundness agenda. The Group’s experiences

in 2008 have heavily influenced both the Group’s and other stakeholders’

approach to this area.

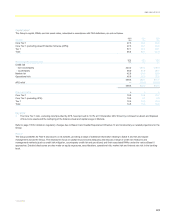

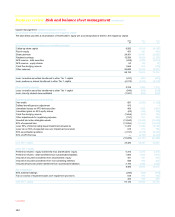

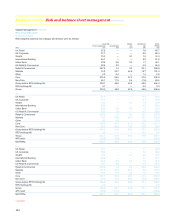

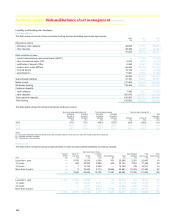

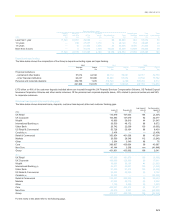

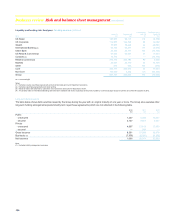

2012 achievements and looking forward*

The Group continued to make solid progress in pursuit of its safety and

soundness agenda throughout 2012, with the majority of its medium-term

balance sheet targets now met or exceeded. This is despite particularly

volatile wholesale market conditions during most of the year due to

ongoing stresses emanating from the eurozone.

The Group has actively reduced short-term wholesale funding and has a

lower wholesale funding need compared to earlier years. Progress has

largely been due to the continued success in executing the Group’s

restructuring efforts, as well as by attracting deposits and continuing to

deleverage via the run down of Non-Core and risk reductions in Markets.

The Group has a smaller balance sheet that is funded by a diverse and

stable deposit base.

The Group is expected to have a lower wholesale funding requirement

going forward. The Group will continue to look at accessing the market

opportunistically from time to time to further support the Group’s overall

funding strategy.

Highlights of 2012 include:

x The Group’s credit profile improved markedly during the year

reflecting the success of its restructuring efforts. Credit default

swaps spreads fell by 60% from their 2011 peak and secondary

bond spreads on five year maturity have narrowed from c.450 basis

points to c.100 basis points.

x The Group repaid all the remaining emergency UK Government

funding and liquidity support that was provided to it during 2008-

2009 under the Credit Guarantee Scheme and Special Liquidity

Scheme.

x The Group resumed coupon payments on hybrid capital securities

following the end of the two year coupon payment ban imposed by

the European Commission as part of its 2009 State Aid ruling.

Coupons remain suspended on Tier 1 instruments issued by RBS

Holdings N.V. until the end of April 2013.

x The Group and RBS plc issued a combined £1.0 billion in term debt

net of buy-backs, a fraction of the £20.9 billion issued in 2011.

Short-term wholesale funding was actively managed down to £41.6

billion from £102.4 billion.

x The overall size of the liquidity buffer reduced modestly to £147.2

billion from £155.3 billion reflecting the lower levels of short-term

wholesale funding and a smaller balance sheet. This also allowed

the Group to alter the ratio of primary to secondary liquid assets

within the liquidity buffer to 62%:38% from 77%:23%. This re-

weighting, by reducing the holdings of the lowest yielding liquid

assets, benefited the Group’s net interest margin, whilst maintaining

a higher quality buffer.

x Retail & Commercial deposits grew by £8 billion to £401 billion, with

particularly strong growth in UK Retail following successful savings

campaigns. Wholesale deposits were allowed to run-off, declining by

£11 billion to leave Group deposits £3 billion lower at £434 billion.

x The Group’s loan:deposit ratio improved from 108% in 2011 to reach

management’s medium-term target of 100% at 31 December 2012,

with lending fully funded by customer deposits and a corresponding

reduction in more volatile short-term wholesale funding.

x The Group has taken advantage of market conditions through the

course of the year to further supplement its capital base.

x RBS Group plc, RBS plc, RBS Citizens Financial Group Inc. and

Direct Line Insurance Group plc in aggregate issued £4.8 billion of

subordinated liabilities in 2012.

x The Group successfully undertook two public liability management

exercises targeting Lower Tier 2 and senior unsecured debt in

support of ongoing balance sheet restructuring initiatives.

*unaudited