RBS 2012 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

135

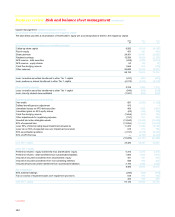

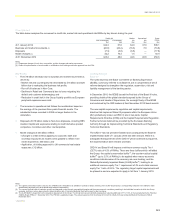

Flow statement

The table below analyses the movement in credit risk, market risk and operational risk RWAs by key drivers during the year.

Credit risk

Non-counterparty Counterparty

Market

risk

Operational

risk

Gross

RWAs

£bn £bn £bn £bn £bn

At 1 January 2012 344.3 61.9 64.0 37.9 508.1

Business and market movements (1) (46.0)(20.4)(16.3) 7.9 (74.8)

Disposals (7.3)(3.8)(6.5) — (17.6)

Model changes (2) 32.2 10.3 1.4 — 43.9

At 31 December 2012 323.2 48.0 42.6 45.8 459.6

Notes:

(1) Represents changes in book size, composition, position changes and market movements.

(2) Refers to implementation of a new model or modification of an existing model after approval from the FSA.

Key Points

x The £75 billion decrease due to business and market movements is

driven by:

- Market risk and counterparty risk decreased by £16 billion and £20

billion due to reshaping the business risk profile;

- Run-off of balances in Non-Core;

- Declines in Retail and Commercial due to loans migrating into

default and customer deleveraging; and

- Reduction in credit risk in the Group liquidity portfolio as European

peripheral exposures were sold.

x The increase in operational risk follows the recalibration based on

the average of the previous three years financial results. The

substantial losses recorded in 2008 no longer feature in the

calculation.

x Disposals of £18 billion relate to Non-Core disposals, including RBS

Aviation Capital and exposures relating to credit derivative product

companies, monolines and other counterparties.

x Model changes of £44 billion reflect:

- Changes to credit metrics applying to corporate, bank and

sovereign exposures as models were updated to reflect more

recent experience, £30 billion; and

- Application, of slotting approach to UK commercial real estate

exposures, £12 billion.

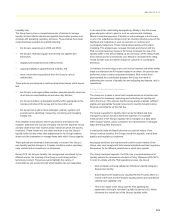

Looking forward

Basel III*

The rules issued by the Basel Committee on Banking Supervision

(BCBS), commonly referred to as Basel III, are a comprehensive set of

reforms designed to strengthen the regulation, supervision, risk and

liquidity management of the banking sector.

In December 2010, the BCBS issued the final text of the Basel III rules,

providing details of the global standards agreed by the Group of

Governors and Heads of Supervision, the oversight body of the BCBS

and endorsed by the G20 leaders at their November 2010 Seoul summit.

The new capital requirements regulation and capital requirements

directive that implement Basel III proposals within the European Union

(EU) (collectively known as CRD IV) are in two parts, Capital

Requirements Directive (CRD) and the Capital Requirements Regulation.

Further technical detail will be provided by the European Banking

Authority through its Implementing Technical Standards and Regulatory

Technical Standards.

The CRD IV has not yet been finalised and consequently the Basel III

implementation date of 1 January 2013 has been missed. While it is

anticipated that agreement of the CRD IV will be achieved during 2013,

the implementation date remains uncertain.

CRD IV and Basel III will impose a minimum common equity Tier 1

(CET1) ratio of 4.5% of RWAs. There are three buffers which will affect

the Group: the capital conservation buffer(1); the counter-cyclical capital

buffer(2) (up to 2.5% of RWAs), to be applied when macro-economic

conditions indicate areas of the economy are over-heating; and the

Global-Systemically Important Bank (G-SIB) buffer(3), leading to an

additional common equity Tier 1 requirement of 4% and a total common

equity Tier 1 ratio of 8.5%. The regulatory target capital requirements will

be phased in and are expected to apply in full from 1 January 2019.

Notes:

(1) The capital conservation buffer is set at 2.5% of RWAs and is intended to be available in periods of stress. Drawing on the buffer would lead to a corresponding reduction in the ability to make

discretionary payments such as dividends and variable compensation.

(2) The counter-cyclical buffer is institution specific and depends on the Group's geographical footprint and the macroeconomic conditions pertaining in the individual countries in which the Group

operates. As there is a time lag involved in determining this ratio, it has been assumed that it will be zero for the time being.

(3) The G-SIB buffer is dependent on the regulatory assessment of the Group. The Group has been provisionally assessed as requiring additional CET1 of 1.5% in the list published by the Financial

Stability Board (FSB) on 1 November 2012. The FSB list is updated annually. The actual requirement will be phased in from 2016, initially for those banks identified (in the list) as G-SIBs in

November 2014.

*unaudited