RBS 2012 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

69

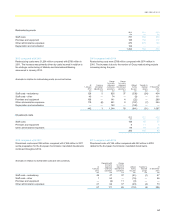

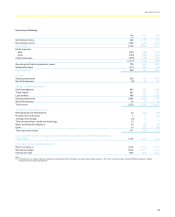

2012 compared with 2011

Operating profit fell by 6% as a 10% decline in income was only partly

offset by lower costs, down 6%, and improved impairment losses, down

33%.

Mortgage balances grew by £4.1 billion with the share of new business at

10%, ahead of our stock level of 8%. Growth as a result of FLS was

starting to appear by the end of the year as mortgage applications moved

through the pipeline to completion. Deposit growth of 6% was in line with

the market and drove a 300 basis point improvement in the loan:deposit

ratio to 103%.

Net interest income was down 7% due to weaker deposit margins and

reduction in unsecured balances, partly offset by mortgage growth.

Unsecured balances now represent 13% of total loans and advances to

customers compared with 23% in 2008, following realignment of risk

appetite and strong mortgage growth. Net interest margin declined as a

result of lower rates on current account hedges and increased

competition on savings rates in the early part of the year, partly offset by

widening asset margins.

Non-interest income was 19% lower mainly due to:

x lower unauthorised overdraft fees as we continue to help customers

manage their finances by providing mobile text alerts and further

improving mobile banking functionality;

x weak consumer confidence lowering spending and associated fees

on cards; and

x lower investment income as a result of weak customer demand and

less advisor availability due to restructuring and retraining in

preparation for regulatory changes in 2013.

Costs were down £150 million, 6%, driven by the ongoing simplification of

processes across the business, lower headcount and lower FSCS levy.

Impairment losses were £259 million or 33% lower, reflecting the

continued benefit of risk appetite tightening in prior years and also a

smaller unsecured loan book. Impairments as a percentage of loans and

advances were 50 basis points versus 70 basis points in 2011.

Risk-weighted assets continued to improve over the year as the portfolio

mix adjusted, with increases in lower-risk secured mortgages, decreases

in unsecured lending and further quality improvements across the book.

2011 compared with 2010

UK Retail delivered strong full year results, as operating profit increased

by £673 million to £2,021 million, despite continued uncertainty in the

economic climate and the low interest rate environment. Profit before

impairment losses was up £301 million or 12%, while impairments fell by

£372 million, with further improvements in the unsecured book and

continued careful mortgage underwriting. Return on equity improved to

24.5%.

The division continued to focus on growing secured lending while at the

same time building customer deposits, thereby reducing the Group’s

reliance on wholesale funding. Loans and advances to customers grew

2%, with a change in mix from unsecured to secured as the Group

actively sought to improve its risk profile. Mortgage balances grew by 5%,

while unsecured lending contracted by 11%.

x Mortgage growth reflected continued strong new business levels.

Gross mortgage lending market share of 10% continues above our

stock position of 8%.

x Customer deposits grew 6%, outperforming the market total deposit

growth of 3%. Savings balances grew by £6 billion, or 9%, with 1.5

million accounts opened, demonstrating the strength of our

customer franchise and our strategy to further develop primary

banking relationships.

Net interest income increased by 6% to £4,302 million, driven by strong

balance sheet growth. Net interest margin increased 6 basis points

recovering asset margins more than offset by more competitive savings

rates and lower long term swap rate returns adversely impacting liability

margins.

Non-interest income declined 10% to £1,206 million, primarily driven by

lower investment and protection income as a result of the dissolution of

the bancassurance joint venture. In addition, a number of changes have

been made to support delivery of Helpful Banking, such as ‘Act Now’ text

alerts, which have decreased fee income.

Overall expenses decreased by 6%. Cost reductions were driven by a

clear management focus on process re-engineering and operational

efficiency together with benefits from the dissolution of the

bancassurance joint venture, partly offset by higher inflation rates in utility

and mail costs.

Impairment losses decreased 32% to £788 million reflecting the impact of

a strengthened risk appetite, and a more stable economic environment.

Risk-weighted assets were broadly stable, with volume growth in lower

risk secured mortgages more than offset by a decrease in the unsecured

portfolio.