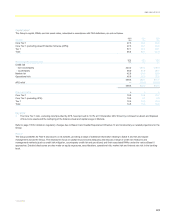

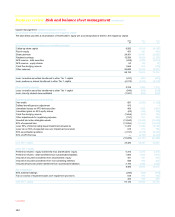

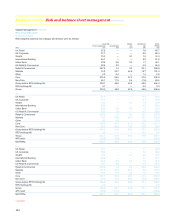

RBS 2012 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

139

Liquidity risk

The Group has in place a comprehensive set of policies to manage

liquidity risk that reflects internal risk appetite, best market practice and

complies with prevailing regulatory strictures. These policies have been

comprehensively updated since 2008 reflecting:

x the Group’s experiences in 2008 and 2009;

x the Group’s restructuring plan and revised risk appetite and

framework;

x regulatory developments and enhancements;

x ongoing instability in global financial markets; and

x more conservative expectations from the Group’s various

stakeholders.

These policies are designed to address three broad issues which ensure

that:

x the Group’s main legal entities maintain adequate liquidity resources

at all times to meet liabilities as and when they fall due;

x the Group maintains an adequate liquidity buffer appropriate to the

business activities of the Group and its risk profile; and

x the Group has in place robust strategies, policies, systems and

procedures for identifying, measuring, monitoring and managing

liquidity risk.

At its simplest, these policies and the governance and actions they

mandate, determine the sources of liquidity risk and the steps the Group

can take when these risks exceed certain tolerances which are actively

monitored. These include not only when and how to use the Group’s

liquidity buffer but also what other adjustments to the Group’s balance

sheet could be undertaken to manage these risks within Group appetite.

These policies are reviewed at least annually or sooner if the Group’s

own liquidity position changes or if market conditions and/or regulatory

rules warrant further amendment or refinement.

During 2012, the Group’s liquidity risk management was tested by two

different events, the lowering of the Group’s credit rating and the

technology incident. These two events highlight the variety of

circumstances and events through which liquidity risk can materialise.

In the case of the credit rating downgrade by Moody’s, the Group was

given adequate notice to plan for such an outcome and challenge

Moody’s analytical approach. Potential or actual changes in the Group’s

or any of its subsidiaries ratings prompt an intensive internal review of the

likelihood and magnitude of such an outcome on customer and

counterparty behaviours. These include stress testing and scenario

modelling. This analysis was reviewed internally and shared with the

FSA. As a precautionary measure the Group increased the size of its

liquidity buffer in the period leading up the conclusion of the rating review.

Such actions proved unnecessary once Moody’s concluded their rating

review as there was very limited impact on customer or counterparty

behaviour.

Conversely, the technology event could not be foreseen and whilst similar

steps to understand the full impact needed to be taken, the process was

performed under a vastly compacted timeframe. Both events have

demonstrated the considerable progress the Group has made in

addressing the sources of liquidity risk and mitigating any impacts, real or

reputational.

Policy, framework and governance

Governance

The Group has in place a robust and comprehensive set of policies and

procedures for assessing, measuring and controlling the liquidity risk

within the Group. This ensures that the Group always maintain sufficient

eligible and appropriate financial resources to meet its forward looking

financial commitments as they fall due.

The Group’s appetite for liquidity risk is set by the Board and then

managed by various functions within the business. For example,

measurement of the Group’s liquidity risk is managed on a daily basis

within Group Finance, policy compliance and development is managed

within the Group Risk framework.

In setting risk limits the Board takes into account the nature of the

Group’s various activities, the Groups overall risk appetite, market best

practice and regulatory compliance.

Analogous provisions and requirements exist for each member of the

Group, who must comply with both internal standards and local regulatory

frameworks for the different jurisdictions in which they operate.

The Group’s principal regulator, the FSA, has a comprehensive set of

liquidity policies the cornerstone of which is Policy Statement (PS) 09/16.

In order to comply with the FSA regulatory process, the Group:

x Must complete and keep updated an Individual Liquidity Adequacy

Assessment (ILAA);

x Submit itself to the Supervisory Liquidity Review Process which is a

review of the ILAA and the Group’s liquidity policies and operational

capacity and capability; and

x This in turn leads to the Group and the FSA agreeing the

parameters of Group’s Individual Liquidity Guidance (ILG). Which

influences the overall size of the Group’s liquidity buffer.