RBS 2012 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

26

DIVISIONAL REVIEW

It was another testing year. There were some

signs of improvement but the economy was

weak. Unemployment remained high, house

prices fell further and wages were flat.

We continued to deal with the legacy of the

past. Our review of how we operate confirmed

that Ulster Bank has a sustainable future if

we make the right changes.

Our systems failed in June. We are very sorry

for the effects that had on our customers.

We worked hard to support them and put

things right.

We extended normal opening hours at

83 branches and Saturday hours at 60.

We opened 22 branches on a Sunday.

Our call centre extended its hours to 10pm.

We were able to transfer funds via Western

Union for customers who were abroad.

Corporate customers were able to withdraw

up to £5,000 or €5,000 with the agreement

of their relationship manager.

We processed transactions manually

if corporate customers could not use

online banking.

In September, we announced how we were

going to make amends to customers who

were affected. We wrote to every Ulster Bank

customer to apologise.

Making RBS safer

Our appointment of a board-level Chief Risk

Officer and a new Risk Leadership Team show

how we are contributing to making RBS safer.

The Chief Risk Officer has led a Group-wide

review of risk as well as playing a central role

in our strategic review.

We moved most of our mortgage accounts to a

new system, which reduces operational risk.

Building a better bank that serves

customers well

We know that Ulster Bank has a sustainable

future. But that depends on us changing how

we work and dealing with the past so that we

focus on serving customers well. Our review

told us our business was too complicated

and our costs too high. We are making

changes that will reduce costs by £80 million

by the end of 2013.

The most significant action we took was

dealing with loans we sold before the crisis.

We gave more effort to managing unsecured

loans, mortgages, SME facilities and larger

corporate exposures. In particular, we are

supporting customers who are finding it hard

to pay their mortgage.

We improved our digital services. That makes

it easier for customers to do business with us.

With our apps for iPhone, BlackBerry and

Android handsets you can:

get an up-to-the-minute balance;

view a mini-statement with your last

six transactions;

make transfers between your Ulster Bank

accounts;

pay your friends, family, credit card,

or utility bills; and

locate your nearest Ulster Bank branch

or cash machine.

Customers used the service almost 18 million

times making 1.2 million payments worth £282

million.

Changing our culture

After the IT failure we ran Listening Groups with

our people. We wanted to make sure that their

views on what went well and what didn't could

be incorporated into our future strategy.

Through our Culture and Engagement Team

we listen to our people, take their feedback

and use it to drive improvement.

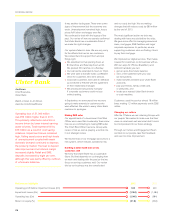

Ulster Bank

Jim Brown

Chief Executive,

Ulster Bank

Watch or listen to Jim Brown

www.rbs.com/AnnualReview

Operating loss of £1,040 million

was £56 million higher than in 2011.

This primarily reflected a reduction in

income driven by lower interest earning

asset volumes. Total expenses fell by

£26 million as a result of cost saving

initiatives. Impairment losses remained

high. Falling asset prices and high levels

of unemployment coupled with weak

domestic demand continued to depress

the property market. The loan to deposit

ratio improved and net interest margin

increased slightly. Retail and SME

deposits increased by eight per cent,

although this was partly offset by outflows

of wholesale balances.

Performance highlights 2012 2011

Operating profit before impairment losses (£m) 324 400

Impairment losses (£m) (1,364) (1,384)

Operating loss (£m) (1,040) (984)

Return on equity (%) (21.8) (22.8)