RBS 2012 Annual Report Download - page 247

Download and view the complete annual report

Please find page 247 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

245

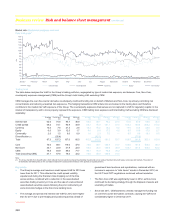

During 2012, an improved methodology was implemented for interest

rates, to more realistically represent the distribution of rate changes. The

enhanced model introduces a level-dependent scaling methodology for

interest rates, which removes the overestimation of rate fluctuations in

regimes of declining rates and leads to a swifter adaptation to changing

circumstances in times of increasing rates. At the point of implementation

the impact on the trading VaR was a decrease of £3.9 million, while the

interest rate VaR saw an increase of £1.4 million. The non-trading total

and interest rate VaR decreased by £0.5 million and £1.9 million

respectively.

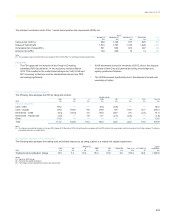

SVaR - is applied to the trading portfolio and utilises data from a specific

one year period of stress. As with VaR, the technique produces estimates

of the potential change in the market value of a portfolio over a specified

time horizon at given confidence level. For the purposes of calculating

regulatory SVaR, a time horizon of ten trading days is assumed and a

confidence level of 99%.

In December 2012, the FSA confirmed the European Banking Authority

guidelines relating to SVaR. The FSA now requires the use of ‘Dynamic’

SVaR, where the worst one year period of stress is determined on a daily

basis.

Risks not in VaR (RNIV) - The RNIV framework has been developed to

quantify those market risks not adequately captured by VaR and SVaR

methodologies. The RNIV approach is used for market risks that fall

within the scope of VaR, but which are insufficiently captured by the

model methodology, for example due to the lack of sufficient historical

data. These risks are therefore assessed outside the VaR model.

The Group adopts two approaches to the quantification of risks not in

VaR (RNIVs):

x Some RNIVs are quantified using a (standalone) VaR approach. For

these RNIVs, two values are calculated: (i) the VaR RNIV; and (ii)

the SVaR RNIV.

x Some RNIVs are quantified using a stress scenario approach. For

these RNIVs, an assessment of ten-day extreme, but plausible,

market moves is used in combination with position sensitivities to

give a stress-type loss number - the stressed RNIV value.

For each legal entity covered by the FSA VaR model waiver, all RNIVs

are aggregated to obtain the following three measures: (i) Total VaR

RNIV; (ii) Total SVaR RNIV; and (iii) Total stressed RNIV.

In each case, no allowance is made for potential diversification in respect

of material RNIVs.

Incremental risk charge (IRC) - The IRC model aims to quantify the

impact of defaults and rating changes on the market value of bonds,

credit derivatives, and other related positions held in the trading book. It

is calculated over a one year horizon to a 99.9% confidence level, and

therefore represents a 1-in-1,000 loss over the following year. The

modelling framework differentiates between the liquidity of different

underlying instruments, with a minimum liquidity horizon of three months.

It also captures basis risks between different products referencing the

same underlying credit (e.g. bonds and credit default swaps (CDS)), and

between similar products with different contractual terms (e.g. CDS in

different currencies). The portfolio impact of correlated defaults and rating

changes is assessed with reference to the resulting market value change

of positions, which is determined using stressed recovery rates and

modelled credit spread changes. The average liquidity horizon at the year

end was 4.6 months.

In 2012, the IRC model was enhanced further; i) to better capture the risk

characteristics of sovereign exposure migrations and defaults; and ii) to

align the recovery rates for sovereign exposures to the banking book

internal ratings based approach.

All price risk (APR) - The APR model is applied to the corporate credit

correlation trading portfolio, subject to certain eligibility constraints

(principally that the underlying names are liquid corporate CDS

positions). The measure is calibrated to a 99.9% confidence level over a

one year time horizon. All material price risks, including defaults and

credit rating changes, are within the scope of the model. Of these, the

most significant are credit spread risk, credit correlation risk, index basis

risk, default risk, and recovery rate risk. In addition, losses due to both

hedging costs and hedge slippage are modelled. The overall APR capital

charge is floored at 8% of the corresponding standard rules charge for

the same portfolio. The average liquidity horizon at the year end was 12

months.

Model validation - A model assessment is performed before a new or

changed model element is implemented, and before a change is made to

a market data mapping. Depending on the results, it may be necessary to

notify the FSA before implementation. The form of internal validation

depends on the type of model and the materiality of the change.

In the case of VaR models, the following steps are considered. In some

cases, for example a minor change to a market data mapping, it will not

be necessary to perform all of the steps. However, in all cases there will

be an independent review and validation.

x Perform accuracy testing of the valuation methods used within VaR

on appropriately chosen test portfolios. Ensure that tests capture the

effect of using external data proxies where these are used.

x Back-test the approach using the relevant portfolio.

x Back-test the approach using hypothetical portfolio(s) where this is

helpful for isolating the performance of specific areas of the model.

x Identify all risks not adequately captured in VaR, and ensure that

such risks are captured via the risks not in VaR process.

x Identify any model weaknesses or scope limitations, their effect and

how they have been addressed.

x Identify ongoing model testing designed to give early warning of

market or portfolio weakness becoming significant.

x Perform impact assessment. Estimate the impact on total one-day

and ten-day 99% VaR at the total legal entity level and the major

business level, and individual risk factor level one-day and ten-day

99% VaR at the total legal entity level.