RBS 2012 Annual Report Download - page 248

Download and view the complete annual report

Please find page 248 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

246

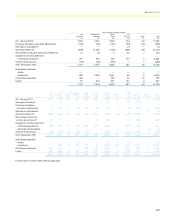

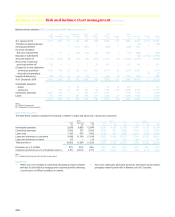

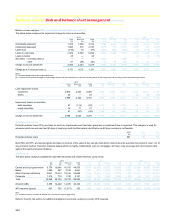

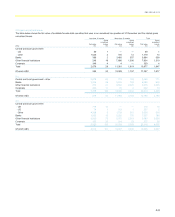

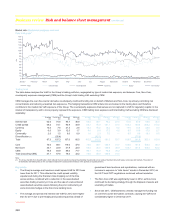

Business review Risk and balance sheet management continued

Market risk: Risk measurement continued

Additionally, Group Risk Analytics (GRA) assess the appropriateness of

all new or amended models prior to their introduction. Existing approved

models are re-assessed on a periodic basis to ensure they remain fit-for-

purpose, for example, following significant market developments or

portfolio changes. The models required to be reviewed by GRA (in

relation to market risk) include VaR, SVaR, IRC, APR and economic

capital. The independent validation review process will consider some or

all of the following areas as appropriate:

x Test and challenge the logical and conceptual soundness of the

methodology;

x The assumptions underlying the model will be tested, where feasible

against actual behaviour. The validation report will judge the

reasonableness and stability of the assumptions and specify which

assumptions, if any, should be routinely monitored in production;

x Compare model results with independent model replication;

x Compare outcome with results from alternative methods;

x Test parameter selection and calibration;

x Ensure that model outputs are sufficiently conservative in areas

where there is significant model uncertainty;

x Confirm applicability of tests for accuracy, and stability; recalculate;

and ensure that results are robust; and

x Ensure appropriate factor sensitivity analysis has been performed

and documented.

Stress testing*

The Group undertakes daily stress testing to identify the potential losses

in excess of VaR. Stress testing is used to calculate a range of trading

book exposures which result from severe and extreme market events.

Stress testing measures the impact of exceptional changes in market

rates and prices on the fair value of the Group’s trading and available-for-

sale portfolios. The Group calculates sensitivity analysis, historical stress

tests and bottom-up stress testing.

Sensitivity analysis measures the sensitivity of the current portfolio of

positions to defined market risk factor movements. These stresses are of

a smaller magnitude compared to historical or bottom-up stress testing

and are subject to the Group Market Risk limit framework.

Historical stress tests calculate the changes in the portfolio valuations

that would be generated if the extreme market movements that occurred

during significant historical market events were repeated. Historical stress

tests also form part of the Group Market Risk limit framework.

Bottom-up stress testing requires analysis of the market risk exposures

by risk factors and different liquidity horizons, to identify the key risks.

Stresses for these risks are then designed following consultation with risk

managers, economists and front office. The tests may be based on an

economic scenario that is translated into risk factor shocks by an

economist or by risk managers and front office as a means of assessing

the vulnerabilities of their book.

The Global Market Risk Stress Testing Committee reviews and discusses

all matters relating to market risk stress testing. Stress test exposures are

discussed with senior management and relevant information is reported

to the Group Risk Committee, the ERF and the Board. Breaches in the

Group’s market risk stress testing limits are monitored and reported.

Reverse stress testing is designed to assess the plausibility of scenarios

derived by stressing market risk factors until the loss reaches a given

threshold. Market Risk contributes to the firm wide, cross risk reverse

stress tests.

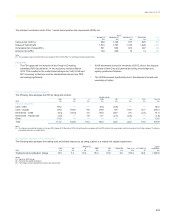

In addition to VaR and stress testing, the Group calculates a wide range

of sensitivity and position risk measures, for example interest rate ladders

or option revaluation matrices. These measures provide valuable

additional controls, often at individual desk or strategy level.

Pricing models*

Pricing models are developed and owned by the front office. Where

pricing models are used as the basis of books and records valuations,

they are subject to oversight and approval by asset level modelled

product review committees. These committees prioritise models for

independent validation by GRA taking into consideration both the

materiality of risk booked against the model and an assessment of the

degree of model risk (i.e. valuation uncertainty arising from choice of

modelling assumptions). GRA review aims to quantify model risk by

comparing model outputs against those of alternative independently

developed models, the results of which are used by Market Risk to inform

risk limits and by Finance to inform model reserves.

Marking-to-market

To ensure that the risks associated with trading activity are reflected in

the financial and management statements, assets and liabilities in the

trading book are measured at their fair value. Any profits or losses on the

revaluation of positions are recognised in the income statement on a daily

basis.

The fair value is the amount at which the instrument could be exchanged

in a current transaction between willing parties. The fair values are

determined following IAS 39 ‘Financial Instruments: Recognition and

Measurement’ guidance, which requires banks to use quoted market

prices or valuation techniques (models) that make the maximum use of

observable inputs.

When marking-to-market using a model, the valuation methodologies

must be approved by all stakeholders (trading, finance, market risk,

model development and model review) prior to use for profit and loss and

risk management purposes.

Traders are responsible for marking-to-market their trading book

positions on a daily basis. Traders can either:

x directly mark a position with a price (e.g. spot foreign exchange); or

x indirectly mark a position through the marking of inputs to an

approved model, which will in turn generate a price.

*unaudited