RBS 2012 Annual Report Download - page 398

Download and view the complete annual report

Please find page 398 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

388 -

389

389 -

390

390 -

391

391 -

392

392 -

393

393 -

394

394 -

395

395 -

396

396 -

397

397 -

398

398 -

399

399 -

400

400 -

401

401 -

402

402 -

403

403 -

404

404 -

405

405 -

406

406 -

407

407 -

408

408 -

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

396

Notes on the consolidated accounts continued

11 Financial instruments - valuation continued

Monoline insurers

The Group has purchased protection from monoline insurers

(‘monolines’), mainly against specific asset-backed securities. Monolines

specialise in providing credit protection against the principal and interest

cash flows due to the holders of debt instruments in the event of default

by the debt instrument counterparty. This protection is typically held in the

form of derivatives such as credit default swaps (CDSs) referencing

underlying exposures held directly or synthetically by the Group.

The gross mark-to-market of the monoline protection depends on the

value of the instruments against which protection has been bought. A

positive fair value, or a valuation gain, in the protection is recognised if

the fair value of the instrument it references decreases. For the majority

of trades the gross mark-to-market of the monoline protection is

determined directly from the fair value price of the underlying reference

instrument. However, for the remainder of the trades the gross mark-to-

market is determined using industry standard models.

The methodology employed to calculate the monoline CVA uses market

implied probability of defaults and internally assessed recovery levels to

determine the level of expected loss on monoline exposures of different

maturities. The probability of default is calculated with reference to

market observable credit spreads and recovery levels. CVA is calculated

at a trade level by applying the expected loss corresponding to each

trade’s expected maturity, to the gross mark-to-market of the monoline

protection. The expected maturity of each trade reflects the scheduled

notional amortisation of the underlying reference instruments and

whether payments due from the monoline are received at the point of

default or over the life of the underlying reference instruments.

Credit derivative product companies (CDPC)

A CDPC is a company that sells protection on credit derivatives. CDPCs

are similar to monoline insurers, however they are not regulated as

insurers.

The Group has purchased credit protection from CDPCs through

tranched and single name credit derivatives. The Group's exposure to

CDPCs is predominantly due to tranched credit derivatives (“tranches”). A

tranche references a portfolio of loans and bonds and provides protection

against total portfolio default losses exceeding a certain percentage of

the portfolio notional (the attachment point) up to another percentage (the

detachment point).

The Group has predominantly traded senior tranches with CDPCs, the

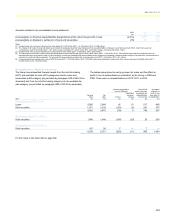

average attachment and detachment points are 16% and 49%

respectively (2011 - 13% and 47%; 2010 - 13% and 49%), and the

majority of the loans and bonds in the reference portfolios are investment

grade.

The gross mark-to-market of the CDPC protection is determined using

industry standard models. Trade restructurings during the second half of

2012 provided market evidence of the fair value of certain CDPC

exposures resulting in valuation adjustments of £279 million at

31 December 2012. These adjustments are also included in the table

above. For trades facing other CDPCs, the methodology employed to

calculate the CDPC CVA is different to that outlined above for monolines,

as there are no market observable credit spreads and recovery levels for

these entities. The level of expected loss on these CDPC exposures is

estimated with reference to risk mitigation strategies.

Other counterparties

The CVA for all other counterparties is calculated on a portfolio basis

reflecting an estimate of the amount a third party would charge to assume

the credit risk.

Where exposure exists to a counterparty that is considered to be close to

default, the CVA is calculated by applying expected losses to the current

level of exposure. Otherwise, expected losses are applied to estimated

potential future exposures which are modelled to reflect the volatility of

the market factors which drive the exposures and the correlation between

those factors. Potential future exposures arising from vanilla products

(including interest rate and foreign exchange derivatives) are modelled

jointly using the Group's core counterparty risk systems. The majority of

the Group's CVA held in relation to other counterparties arises on these

vanilla products together with exposures to counterparties which are

considered to be close to default. The exposures arising from all other

product types are modelled and assessed individually. The potential

future exposure to each counterparty is the aggregate of the exposures

arising on the underlying product types.

The correlation between exposure and counterparty risk is also

incorporated within the CVA calculation where this risk is considered

significant. The risk primarily arises on credit derivative trades where the

default risk of the referenced entity is correlated with the counterparty

risk. The risk also arises on trades with emerging market counterparties

where the gross mark-to-market value of the trade, and

therefore the counterparty exposure, increases as the strength of the

local currency declines.

Collateral held under a credit support agreement is factored into the CVA

calculation. In such cases where the Group holds collateral against

counterparty exposures, CVA is held to the extent that residual risk

remains.

Bid-offer, liquidity and other reserves

Fair value positions are adjusted to bid or offer levels, by marking

individual cash based positions directly to bid or offer or by taking bid-

offer reserves calculated on a portfolio basis for derivatives exposures.

The bid-offer approach is based on current market spreads and standard

market bucketing of risk.