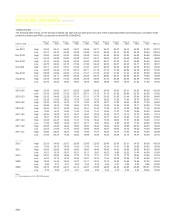

RBS 2012 Annual Report Download - page 531

Download and view the complete annual report

Please find page 531 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

521 -

522

522 -

523

523 -

524

524 -

525

525 -

526

526 -

527

527 -

528

528 -

529

529 -

530

530 -

531

531 -

532

532 -

533

533 -

534

534 -

535

535 -

536

536 -

537

537 -

538

538 -

539

539 -

540

540 -

541

541 -

542

-

543

|

|

RBS GROUP 2012

529

Commercial paper conduit - a special purpose entity that issues

commercial paper and uses the proceeds to purchase or fund a pool of

assets. The commercial paper is secured on the assets and is redeemed

either by further commercial paper issuance, repayment of assets or

liquidity drawings.

Commercial real estate - freehold and leasehold properties used for

business activities. Commercial real estate includes office buildings,

industrial property, medical centres, hotels, retail stores, shopping

centres, agricultural land and buildings, warehouses, garages etc.

Compression trades - portfolio compression reduces the overall notional

size and number of outstanding contracts in credit derivative portfolios

without changing the overall risk profiles of these portfolios. This is

achieved by terminating existing trades on single name reference entities

and on indices and replacing them with a smaller number of new trades

with substantially smaller notionals that carry the same risk profile and

cash flows as the initial portfolio.

Contractual maturity - the date in the terms of a financial instrument on

which the last payment or receipt under the contract is due for settlement.

Core Tier 1 capital - called-up share capital and eligible reserves plus

equity non-controlling interests, less intangible assets and other

regulatory deductions.

Core Tier 1 capital ratio - core Tier 1 capital as a percentage of risk-

weighted assets.

Cost:income ratio - operating expenses as a percentage of total income.

Counterparty credit risk - the risk that a counterparty defaults before the

maturity of a derivative or sale and repurchase contract. In contrast to

non-counterparty credit risk, the exposure to counterparty credit risk

varies by reference to a market factor (e.g. interest rate, exchange rate,

asset price).

Coverage ratio - impairment provisions as a percentage of impaired

loans.

Covered bonds - debt securities backed by a portfolio of mortgages that

are segregated from the issuer's other assets solely for the benefit of the

holders of the covered bonds.

CRD III - the CRD III package came into force on 1 January 2011. It

requires higher capital requirements for re-securitisations; upgrades

disclosure standards for securitisation exposures; strengthens capital

requirements for the trading book; and introduces new remuneration

rules.

CRD IV - in July 2011, the European Commission published its proposed

legislation for a Capital Requirements Directive and a Capital

Requirements Regulation, which together form the CRD IV package. The

package implements the Basel III capital proposals and also includes

new proposals on sanctions for non-compliance with prudential rules,

corporate governance and remuneration. CRD IV has yet to be enacted

into European law and its implementation date remains uncertain.

Credit default swap (CDS) - a contract where the protection seller

receives premium or interest-related payments in return for contracting to

make payments to the protection buyer upon a defined credit event in

relation to a reference financial asset or portfolio of financial assets.

Credit events usually include bankruptcy, payment default and rating

downgrades.

Credit derivative product company (CDPC) - a special purpose entity that

sells credit protection under credit default swaps or certain approved

forms of insurance policies. Sometimes they can also buy credit

protection. CDPCs are similar to monoline insurers. However, unlike

monoline insurers, they are not regulated as insurers.

Credit derivatives - contractual agreements that provide protection

against a credit event on one or more reference entities or financial

assets. The nature of a credit event is established by the protection buyer

and protection seller at the inception of a transaction, and such events

include bankruptcy, insolvency or failure to meet payment obligations

when due. The buyer of the credit derivative pays a periodic fee in return

for a payment by the protection seller upon the occurrence, if any, of a

credit event. Credit derivatives include credit default swaps, total return

swaps and credit swap options.

Credit enhancements - techniques that improve the credit standing of

financial obligations; generally those issued by an SPE in a securitisation.

External credit enhancements include financial guarantees and letters of

credit from third-party providers. Internal enhancements include excess

spread - the difference between the interest rate received on the

underlying portfolio and the coupon on the issued securities; and over-

collateralisation - on securitisation, the value of the underlying portfolio is

greater than the securities issued.

Credit grade - a rating that represents an assessment of the credit

worthiness of a customer. It is a point on a scale representing the

probability of default of a customer.

Credit risk - the risk that the Group will incur losses owing to the failure of

customers to meet their financial obligations to the Group.

Credit risk mitigation - reducing the credit risk of an exposure by

application of techniques such as netting, collateral, guarantees and

credit derivatives.

Credit risk spread - the yield spread between securities with the same

currency and maturity structure but with different associated credit risks,

with the yield spread rising as the credit rating worsens. It is the premium

over the benchmark or risk-free rate required by the market to take on a

lower credit quality.

Credit valuation adjustments (CVA) - the CVA is the difference between

the risk- free value of a portfolio of trades and its market value, taking into

account the counterparty’s risk of default. It represents the market value

of counterparty credit risk, or an estimate of the adjustment to fair value

that a market participant would make to reflect the creditworthiness of its

counterparty.