RBS 2012 Annual Report Download - page 167

Download and view the complete annual report

Please find page 167 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

165

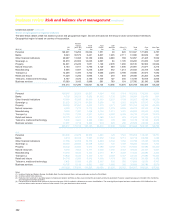

Key points

Financial markets and the Group’s focus on risk appetite and sector

concentration had a direct impact on the portfolio during the year with the

following key trends observed:

x Total credit risk assets fell 7%, with reductions in all wholesale

sectors. Exposure to the personal sector remained broadly flat.

x Credit risk assets fell in all geographic regions, except the UK. This

was driven by the Group’s continued focus on reducing exposures to

the peripheral eurozone countries and appropriate management of

liquidity requirements reflected in the reduced exposures to Western

European and US central banks.

x UK exposure, as a proportion of the total portfolio, increased during

the year and now comprises 51% of credit risk assets, driven by

continued growth in UK personal sector assets and increased UK

sovereign risk exposure.

x Exposure to the property sector fell by 11% during the year driven

by tighter portfolio controls in all regions and a £9.5 billion reduction

in Non-Core resulting from focussed action on early and contractual

repayments.

x Exposure to banks and financial institutions declined by 5% as a

result of subdued borrowing activity and a reduction in lending and

derivatives to finance companies, financial services companies,

funds, monoline insurers and Credit Derivative Product Companies

(CDPCs).

x Reported exposures are affected by currency movements. During

2012, sterling appreciated 4.4% against the US dollar and 2.6%

against the euro resulting in a decrease in sterling terms of

exposures denominated in these currencies (and in other currencies

linked to the US dollar or euro).

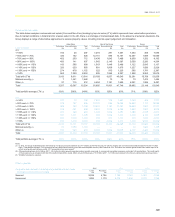

x The Group’s sovereign portfolio comprises exposures to central

governments, central banks and sub-sovereigns such as local

authorities, primarily in the Group’s key markets of the UK, Western

Europe and the USA. The asset quality is high as exposures are

largely cash balances placed with central banks such as the Bank of

England, the Federal Reserve and the Eurosystem (including the

European Central Bank and central banks in the eurozone).

Exposure to sovereigns fluctuates according to Group liquidity

requirements and cash positions. These are driven by inflows and

outflows of deposits which determine the level of cash placed with

central banks and have contributed to higher exposures at the Bank

of England and lower exposures at European and US central banks.

Information on the Group’s exposure to governments, including

peripheral eurozone sovereigns, can be found in the Risk

management section on Country risk.

x Exposure to the banking sector is one of the largest in the Group’s

portfolio. The sector is well diversified geographically with derivative

exposures being largely collateralised. Exposures are tightly

controlled through the combination of the single name concentration

framework, bespoke credit policies and country limits. Exposures to

the banking sector decreased by £3 billion in 2012 as a result of

reduced interbank lending and derivative activity, and a reduction in

limits to banks in countries under stress, such as the peripheral

eurozone countries.

x Exposure to other financial institutions comprising traded and non-

traded products is spread across a range of financial companies

including insurance, securitisation vehicles, financial intermediaries

including broker dealers and CCPs, financial guarantors - monolines

and CDPCs - and funds comprising unleveraged, hedge and

leveraged funds. The size and asset quality of the Core portfolio

have not changed materially since 2011. However, entities in this

sector remain vulnerable to market shocks or contagion from the

banking sector. Credit risk is managed through the single name

concentration, sector concentration and asset and product class

frameworks, with specific sector and product caps in place where

there is a perception of heightened credit risk. The Group is also

actively managing down its exposures to monolines and CDPCs

with a view to exiting these portfolios. Exposures to CDPCs and

monolines have decreased materially during 2012 as trades are

commuted and exposures reduce due to tightening credit spread of

the assets protected by CDPCs and monolines.

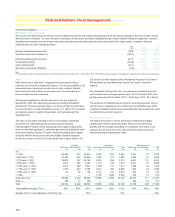

x The Group’s exposure to the property sector was £91 billion (a fall of

11% during the year), the majority of which was commercial real

estate in Ireland and the UK (see section on commercial real estate

on pages 181 and 182 for further details). The remainder comprised

lending to construction companies and building materials groups,

which fell by £1.9 billion (15%), and housing associations, which

remained stable. Most of the Group’s Core property exposure is

within UK Corporate (73%).

x The 22% decline in exposure to the retail and leisure sectors, was

driven by the de-leveraging by customers and refinements in sector

classifications within the Wealth division. Excluding the impact of

sector reclassifications, the reduction in the retail and leisure

portfolios was 15% in 2012. While the market outlook for this sector

remains challenging and despite some high-profile failures among

UK high street retailers, losses on the Group’s retail portfolio

remained low during 2012. The sector continues to show wide

variation in performance, however, credit metrics overall remained

broadly stable. The leisure sector displayed weaker credit metrics

than the wider corporate portfolio, in line with the industry trend. The

Group’s risk appetite is driven by the importance of the leisure

sector to the UK franchise, especially for the UK Corporate division,

but is mitigated through tighter origination policies and a reduction in

exposure to high risk sub-sectors. Leisure sector exposure fell by

8% in 2012 driven predominantly by Non-Core. The gambling sub-

sector is subject to specific controls due to its high credit and

reputational risk profile.