RBS 2012 Annual Report Download - page 405

Download and view the complete annual report

Please find page 405 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

395 -

396

396 -

397

397 -

398

398 -

399

399 -

400

400 -

401

401 -

402

402 -

403

403 -

404

404 -

405

405 -

406

406 -

407

407 -

408

408 -

409

409 -

410

410 -

411

411 -

412

412 -

413

413 -

414

414 -

415

415 -

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

403

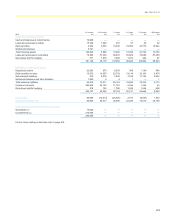

The level 3 sensitivities above are calculated at a trade or low level

portfolio basis. They are not calculated on an overall portfolio basis and

therefore do not reflect the likely overall potential uncertainty on the

whole portfolio. The figures are aggregated and do not reflect the

correlated nature of some of the sensitivities. In particular, for some of the

portfolios the sensitivities may be negatively correlated where a

downwards movement in one asset would produce an upwards

movement in another, but due to the additive presentation of the above

figures this correlation cannot be observed. The actual potential

downside sensitivity of the total portfolio may be less than the non-

correlated sum of the additive figures as shown in the above table.

Judgmental issues

The diverse range of products traded by the Group results in a wide

range of instruments that are classified into the three level hierarchy.

Whilst the majority of these instruments naturally fall into a particular

level, for some products an element of judgment is required. The majority

of the Group’s financial instruments carried at fair value are classified as

level 2: inputs are observable either directly (i.e. as a price) or indirectly

(i.e. derived from prices).

Active and inactive markets

A key input in the decision making process for the allocation of assets to

a particular level is liquidity. In general, the degree of valuation

uncertainty depends on the degree of liquidity of an input. For example, a

derivative can be placed into level 2 or level 3 dependent upon its

liquidity.

Where markets are liquid or very liquid, little judgment is required.

However, when the information regarding the liquidity in a particular

market is not clear, a judgment may need to be made. This can be made

more difficult as assessing the liquidity of a market may not always be

straightforward. For an equity traded on an exchange, daily volumes of

trading can be seen, but for an over-the counter (OTC) derivative

assessing the liquidity of the market with no central exchange can be

more difficult.

A key related issue is where a market moves from liquid to illiquid or vice

versa. Where this change is considered to be temporary, the

classification is not changed. For example, if there is little market trading

in a product on a reporting date but at the previous reporting date and

during the intervening period the market has been considered to be

liquid, the instrument will continue to be classified in the same level in the

hierarchy. This is to provide consistency so that transfers between levels

are driven by genuine changes in market liquidity and do not reflect short

term or seasonal effects.

Interaction with the IPV process

The determination of an instrument’s level cannot be made at a global

product level as a single product type can be in more than one level. For

example, a single name corporate credit default swap could be in level 2

or level 3 depending on whether the reference counterparty is liquid or

illiquid.

As part of the Group’s IPV process, data is gathered at a trade level from

market trading activity, trading systems, pricing services, consensus

pricing providers, brokers and research material amongst other sources.

The breadth and depth of this data allows a good assessment to be made

of liquidity and pricing uncertainty, which assists with the process of

allocation to an appropriate level. Where suitable independent pricing

information is not readily available the instrument will be considered to be

level 3.

Modelled products

For modelled products the market convention is to quote these trades

through the model inputs or parameters as opposed to a cash price

equivalent. A mark-to-market is derived from the use of the independent

market inputs calculated using the Group’s model.

The decision to classify a modelled asset as level 2 or 3 will be

dependent upon the product/model combination, the currency, the

maturity, the observability of input parameters and other factors. All these

need to be assessed to classify the asset.

An assessment is made of each input into a model. There may be

multiple inputs into a model and each is assessed in turn for observability

and quality. If an input fails the observability or quality tests then the

instrument is considered to be in level 3 unless the input can be shown to

have an insignificant effect on the overall valuation of the product.

The majority of derivative instruments are classified as level 2 as they are

vanilla products valued using observable inputs. The valuation

uncertainty on these is considered to be low and both input and output

testing may be available. Examples of these products would be vanilla

interest rate swaps, foreign exchange swaps and liquid single name

credit derivatives.

Non-modelled products

Non-modelled products are generally quoted on a price basis and can

therefore be considered for each of the 3 levels. This is determined by

the liquidity and valuation uncertainty of the instruments which is in turn

measured from the availability of independent data used by the IPV

process.

The availability and quality of independent pricing information is

considered during the classification process. An assessment is made

regarding the quality of the independent information. For example where

consensus prices are used for non-modelled products, a key assessment

of the quality of a price is the depth of the number of prices used to

provide the consensus price. If the depth of contributors falls below a set

hurdle rate, the instrument is considered to be level 3. This hurdle rate is

consistent with the rate used in the IPV process to determine whether or

not the data is of sufficient quality to adjust the instrument’s valuations.

However, where an instrument is generally considered to be illiquid, but

regular quotes from market participants exist, these instruments may be

classified as level 2 depending on frequency of quotes, other available

pricing and whether the quotes are used as part of the IPV process or

not.