RBS 2012 Annual Report Download - page 181

Download and view the complete annual report

Please find page 181 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

179

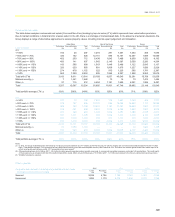

Unsecured portfolios

For unsecured portfolios in UK Retail and Ulster Bank, forbearance

treatments comprise either debt consolidation loans provided to

customers subject to collections activity who do not meet the Group’s

standard underwriting criteria, longer-term financial hardship plans, or

repayment arrangements to facilitate the repayment of overdraft

excesses. Additionally, support is provided to customers experiencing

financial difficulties through breathing space initiatives on all unsecured

products, including credit cards, whereby the Group suspends

collections activity for a 30-day period to allow customers to establish a

debt repayment plan. Arrears continue to accrue for customer loans

benefiting from breathing space.

x For unsecured portfolios in UK Retail, £162 million of balances

(1.1% of the total unsecured balances) were subject to

forbearance at 2012 year end.

x For unsecured portfolios in Ulster Bank, £20 million (3.4% by

value) of the population was subject to forbearance at 31

December 2012.

Within RBS Citizens, granting of forbearance is significantly less

extensive for non real-estate portfolios, as it is predominantly restricted

to the granting of short-term (1-3 months) loan extensions to

customers to alleviate the financial burden caused by temporary

hardship. Such extensions are offered only if a customer has

demonstrated a capacity and willingness to pay following the extension

term. The number and frequency of extensions available to a given

customer are limited per customer. Additionally, in the case of loans

secured by vehicles and credit cards, RBS Citizens may offer

temporary interest rate modifications, but no principal reduction. RBS

Citizens may also provide forbearance to student loan borrowers

consistent with the policy guidelines of the US Office of the Comptroller

of the Currency.

Provisioning for retail customers

Provisions are assessed in accordance with the Group’s provisioning

policies.

The majority of retail forbearance takes place in the performing book

and, for the purposes of the latent loss provisions, these constitute a

separate risk pool. They are subject to higher provisioning rates than

the remainder of the performing book. These rates are reviewed

regularly in both divisions. Once forbearance is granted, the account

continues to be assessed separately for latent provisioning for 24

months (UK Retail only) or until the forbearance period expires. After

that point, the account is no longer separately identified for latent

provisioning. In the non-performing portfolio, assets are grouped into

homogeneous portfolios sharing similar credit characteristics according

to the asset type. Further characteristics such as LTVs, arrears status

and default vintage are also considered when assessing recoverable

amount and calculating the related provision requirement. Whilst non-

performing forbearance retail loans do not form a separate risk pool,

the LGD models used to calculate the collective impairment provision

will be affected by agreements made under forbearance

arrangements.

In RBS Citizens, consumer loans subject to forbearance are

segmented from the rest of the non-forborne population and assessed

individually for impairment loan throughout their lives until the accounts

are repaid or fully written-off. The amount of recorded impairment

depends upon whether the loan is collateral dependent. If the loans

are considered collateral dependent, the excess of the loan’s carrying

amount over the fair value of the collateral is the impairment amount. If

the loan is not deemed collateral dependent, the excess of the loans’

carrying amount over the present value of expected future cash flows

is the impairment amount. Any confirmed losses are charged off

immediately.

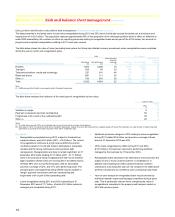

Impairment loss provision methodology

A financial asset or portfolio of financial assets is impaired and an

impairment loss incurred if there is objective evidence that an event or

events since initial recognition of the asset has adversely affected the

amount or timing of future cash flows from the asset.

For retail loans, which are segmented into collective, homogenous

portfolios, time-based measures, such as days past due, are typically

used as evidence of impairment. For these portfolios, the Group

recognises an impairment at 90 days past due.

For corporate portfolios, given their complexity and nature, the Group

relies not only on time-based measures, but also on management

judgement to identify evidence of impairment. Other factors considered

may include: significant financial difficulty of the borrower; a breach of

contract; a loan restructuring; a probable bankruptcy; and any

observable data indicating a measurable decrease in estimated future

cash flows.