RBS 2012 Annual Report Download - page 255

Download and view the complete annual report

Please find page 255 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

253

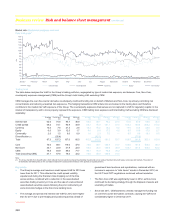

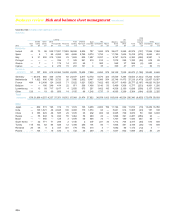

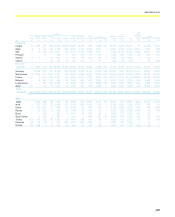

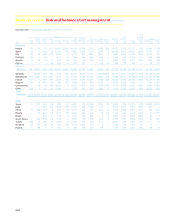

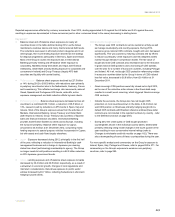

Country risk

Introduction*

Country risk is the risk of material losses arising from significant country-

specific events such as sovereign events (default or restructuring);

economic events (contagion of sovereign default to other parts of the

economy, cyclical economic shock); political events (transfer or

convertibility restrictions, expropriation or nationalisation); and conflict.

Such events have the potential to affect elements of the Group’s credit

portfolio that are directly or indirectly linked to the country in question and

can also give rise to market, liquidity, operational and franchise risk-

related losses.

External environment*

Country risk, notably in the eurozone, remained elevated in 2012,

particularly in the first half of the year. Economic growth projections were

lowered, predominantly for Europe, but also for a number of major

emerging markets. However, important first steps towards achieving

longer-term stabilisation in the eurozone led to some notable easing of

crisis risks. Growth data from major non-European economies, such as

China, were more encouraging towards the end of the year. The ability of

policymakers to tackle fiscal challenges and restore confidence and

growth in both the US and Europe will be a key factor in determining the

pace of recovery.

Eurozone risks

Eurozone risks continued to dominate, as concerns about the impact of

banking sector problems on government balance sheets led to further

capital flight from periphery countries and a rise in sovereign bond yields

until August, particularly for Spain. To break the feedback loop between

banks and their sovereigns, eurozone leaders agreed at their June

summit that the European Stability Mechanism (ESM), the eurozone’s

permanent crisis fund, could lend to banks directly once a single

eurozone-wide banking regulator had been established. They also

approved the provision by the ESM of significant financial support to

Spain to recapitalise its banks.

In the second half of the year, the ESM became fully operational and the

European Central Bank (ECB) announced a major new facility, Outright

Monetary Transactions. This facility allows secondary market purchases

by the ECB of bonds issued by eurozone sovereigns that are subject to a

European Union (EU)/International Monetary Fund (IMF) support

programme. Following these steps, sovereign bond yields fell markedly.

Meanwhile, in Greece, private sector claims on the government were

restructured in early 2012, but political risks remained acute as two

successive parliamentary elections eventually resulted in a narrow victory

for the pro-bailout New Democracy party. As the electoral process

delayed policy implementation and the recession, contrary to earlier

expectations, deepened further, additional reforms became necessary

and the European Commission, the IMF and the ECB (known collectively

as the Troika) further eased Greece’s targets.

Elsewhere, Ireland continued to make progress towards targets set out in

its Troika programme, notably allowing the government to resume a

degree of market financing. Talks with the European authorities on ways

to relieve the government of some of the costs of past banking sector

support continued, resulting in a favourable restructuring of the Anglo

Irish promissory note in early 2013, reducing related fiscal costs

somewhat. Notwithstanding these developments, Irish growth remained

very weak and reliant on external demand. Portugal also made progress

in a number of areas, though had greater structural constraints to

address to boost longer-term growth prospects. Towards the end of the

year, Cyprus also entered negotiations with the EU and IMF on a support

programme. The eurozone as a whole entered recession in the second

half of the year, although divergence within the currency union continued,

with the core considerably stronger than the periphery.

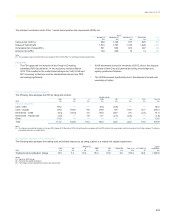

Emerging markets

Emerging markets performed better on the whole. In developing Asia, the

economies of China and India both continued to slow from a strong base,

but risks remained held in check by healthy external balance sheets.

Emerging countries in Europe started to be affected by very weak growth

in the eurozone, with the most export-focused economies being worst hit.

However, countries that took significant action in the wake of the financial

crisis to stabilise their banking sectors, saw an easing of risk. Turkey was

upgraded by one rating agency to investment grade.

General political instability seen in the Middle East and North Africa in

2011 moderated in 2012 in most countries except Syria, although

transition to democratic rule was only partial in some cases. Excluding

Bahrain, Gulf Cooperation Council countries were generally more stable,

underpinned by high oil prices.

Latin America continued to be characterised by greater stability, due to

generally healthier sovereign balance sheets. However, growth prospects

deteriorated because of weaker external demand, notably in the region’s

largest economy, Brazil.

Outlook

Overall, the outlook for 2013 remains challenging with risks likely to

remain elevated but divergent. Much will depend on the success of EU

efforts to contain contagion from the sovereign crisis (where downside

risks are high) and on whether growth headwinds in larger advanced

economies, particularly the US and Japan, persist. Emerging market

balance sheet risks remain lower, despite structural and political

constraints, but it is expected that these economies will continue to be

affected by events elsewhere through financial markets and trade

channels.

*unaudited

Business review Risk and balance sheet management continued