RBS 2012 Annual Report Download - page 406

Download and view the complete annual report

Please find page 406 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

396 -

397

397 -

398

398 -

399

399 -

400

400 -

401

401 -

402

402 -

403

403 -

404

404 -

405

405 -

406

406 -

407

407 -

408

408 -

409

409 -

410

410 -

411

411 -

412

412 -

413

413 -

414

414 -

415

415 -

416

416 -

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

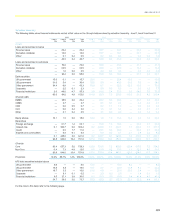

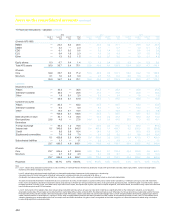

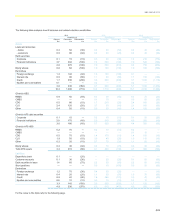

404

Notes on the consolidated accounts continued

11 Financial instruments - valuation continued

For some instruments with a wide number of available price sources,

there may be differing quality of available information and there may be a

wide range of prices from different sources. In these situations an

assessment is made as to which source is the highest quality and this will

be used to determine the classification of the asset. For example, a

tradable quote would be considered a better source than a consensus

price.

Instruments that cross levels

Some instruments will predominantly be in one level or the other, but

others may cross between levels. For example, a cross currency swap

may be between very liquid currency pairs where pricing is readily

observed in the market and will therefore be classified as level 2. The

cross currency swap may also be between two illiquid currency pairs in

which case the swap would be placed into level 3. Defining the difference

between liquid and illiquid may be based upon the number of consensus

providers the consensus price is made up from and whether the

consensus price can be supplemented by other sources.

Level 3 portfolios and sensitivity methodologies

For each of the portfolio categories shown in the tables above, there

follows a description of the types of products that comprise the portfolio

and the valuation techniques that are applied in determining fair value,

including a description of valuation techniques used for levels 2 and 3

and inputs to those models and techniques. Where reasonably possible

alternative assumptions of unobservable inputs used in models would

change the fair value of the portfolio significantly, the alternative inputs

are indicated. Where there have been significant changes to valuation

techniques during the year a discussion of the reasons for this are also

included.

Overview of sensitivity methodologies

Reasonably possible alternative assumptions of unobservable inputs are

determined based on a 95% confidence interval. The assessments

recognise different favourable and unfavourable valuation movements

where appropriate. Each unobservable input within a product is

considered separately and sensitivity is reported on an additive basis.

Alternative assumptions are determined with reference to all available

evidence including consideration of the following: quality of independent

pricing information taking into account consistency between different

sources, variation over time, perceived tradability or otherwise of

available quotes; consensus service dispersion ranges; volume of trading

activity and market bias (e.g. one-way inventory); day 1 P&L arising on

new trades; number and nature of market participants; market conditions;

modelling consistency in the market; size and nature of risk; length of

holding of position; and market intelligence.

Loans and advances to customers

Loans in level 3 primarily comprise loans to emerging market

counterparties and, legacy commercial and residential mortgages.

Loans to emerging market counterparties

The trades in each loan structure are valued using curves using a proxy

methodology. Each curve consists of the independent proxy value and

various basis adjustments, such as those relating to loan-CDS basis,

credit basis, tenor and liquidity. For the low and high valuation scenarios

for the structures, these different bases are flexed up and down within the

range that each one is deemed to span. The resultant maximum and

minimum scenario curves are used to value the assets and liabilities in

the structure separately. The low valuation scenario is the one that

minimises the assets and maximises the liabilities. The high valuation

scenario is the converse.

Commercial mortgages

These senior and mezzanine commercial mortgages are loans secured

on commercial land and buildings that were originated or acquired by the

Group for securitisation. Senior commercial mortgages carry a variable

interest rate and mezzanine or more junior commercial mortgages may

carry a fixed or variable interest rate. Factors affecting the value of these

loans may include, but are not limited to, loan type, underlying property

type and geographic location, loan interest rate, loan-to-value ratios, debt

service coverage ratios, prepayment rates, cumulative loan loss

information, yields, investor demand, market volatility since the last

securitisation and credit enhancement. Where observable market prices

for a particular loan are not available, the fair value will typically be

determined with reference to observable market transactions in other

loans or credit related products including debt securities and credit

derivatives. Assumptions are made about the relationship between the

loan and the available benchmark data.

Residential mortgages

These pools of residential mortgages were mostly acquired for

securitisation before the 2008 financial crisis. Factors that affect the

value, or liquidation level, of these loans are geographic location, current

loan-to-value, condition of the home, and availability of eligible buyers.

The loans are serviced by various mortgage servicers. Operations and

the Front Office monitor the performance of these loans and the

valuations are tested against an estimated recovery level as part of the

IPV process. The market for non-agency securitisation remains extremely

weak and is restricted to new issue prime loans.

Debt securities

Level 3 debt securities principally comprise asset-backed securities.

Residential mortgage-backed securities (RMBS)

RMBS where the underlying assets are US agency-backed mortgages

and there is regular trading are generally classified as level 2 in the fair

value hierarchy. RMBS are also classified as level 2 when regular trading

is not prevalent in the market, but similar executed trades or third-party

data including indices, broker quotes and pricing services can be used to

substantiate the fair value. RMBS are classified as level 3 when trading

activity is not available and a model with significant unobservable data is

utilised.