RBS 2012 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

18

OUR BUSINESS AND OUR STRATEGY

We have noted before that when economies are

emerging from recessions rooted in high levels

of debt and stresses in the financial system,

growth is slower than in the typical recovery.

That was the experience of our major markets

again in 2012.

In the UK, growth weakened. Total economic

activity, as measured by gross domestic

product (GDP), was flat compared with growth

of 0.9% in 2011. At the start of the year,

expectations had been more positive, the

consensus forecast for growth having been

0.5%. Yet the year ended with the economy

contracting.

More positively, unemployment fell, from around

8.3% at the turn of the year to 7.7% towards its

end. That helped to offset the continuing

squeeze on the spending power of earnings as

wages grew by less than inflation.

Housing market activity remained subdued.

Prices were broadly stable, some indices

showing a rise and others a fall. Any price

increases seem to have been concentrated in

and around London.

The Bank of England continued its ultra-loose

monetary policy stance. Although inflation

remained above target, the Bank kept interest

rates at 0.5%. In fact, its greater concern was

that the weak economy would cause inflation to

be too low and in both February and July it

increased its asset purchase programme by

£50 billion taking the total value of assets

purchased to £375 billion. The Government’s

decision to transfer the coupon payments from

the Asset Purchase Facility to HM Treasury,

which will use these proceeds to reduce the

stock of Government debt, has a similar effect

to further quantitative easing.

In July, the Bank of England and HM Treasury

launched the Funding for Lending Scheme

(FLS). It is designed to boost lending to

households and non-financial firms. Early

indications from the Bank’s Credit Conditions

Survey suggested that the supply of credit had

expanded towards the end of the year.

In the United States, GDP growth was slightly

stronger at 2.2% compared with 1.8% in 2011.

Uncertainty about how leaders might resolve

immediate and longer-term fiscal challenges

weighed on growth during much of the year.

There was encouraging news on the job market,

where unemployment had fallen to 7.8% in

December, and the housing market, where

prices and construction activity started to rise.

However, concerned that the recovery remained

too slow to return unemployment to rates

consistent with its mandate to foster maximum

employment, the Federal Open Market

Committee changed policy in two ways. In

September it agreed to increase monetary

accommodation by purchasing mortgage-

backed securities at a pace of $40 billion per

month. Second, it announced in December it

anticipates the Fed Funds rate remaining

exceptionally low as long as the unemployment

rate is above 6.5%, inflation one to two years

ahead is expected to be no more than 2.5%

and inflation expectations are well anchored.

Ireland’s GDP grew by 1.3% in the four quarters

to Q3 2012 as the economy continued its slow

recovery from deep recession. The export

sector continued to benefit from the boost to

competitiveness delivered by falling real wages.

For Ireland, gross national product (GNP) is a

better measure of people's material well-being.

It reflects the income residents receive rather

than the value of the incomes generated in the

country, an important distinction where there is

a large foreign-owned sector that remits profits

overseas. GNP increased by 1.1%.

Unemployment in Ireland averaged more than

14%. At the end of the year house prices were

4.5% lower than 12 months earlier and around

50% below their peak. The rate of decline was

slower than at any time since 2008 and there

were tentative signs that prices were stabilising.

Entering 2012, the greatest economic concern

was how problems related to sovereign debt in

the euro zone would be managed. By agreeing

the outline of a banking union, undertaking to

purchase sovereign debt to push down yields

and making progress on fiscal rules, European

leaders and the European Central Bank took

some steps that are necessary if an economic

and monetary union is to be sustained. At the

end of the year the probability that some of the

worse outcomes would be realised had fallen

although they had not disappeared. Despite

this progress, euro zone GDP contracted and

unemployment had risen to almost 12% by

December.

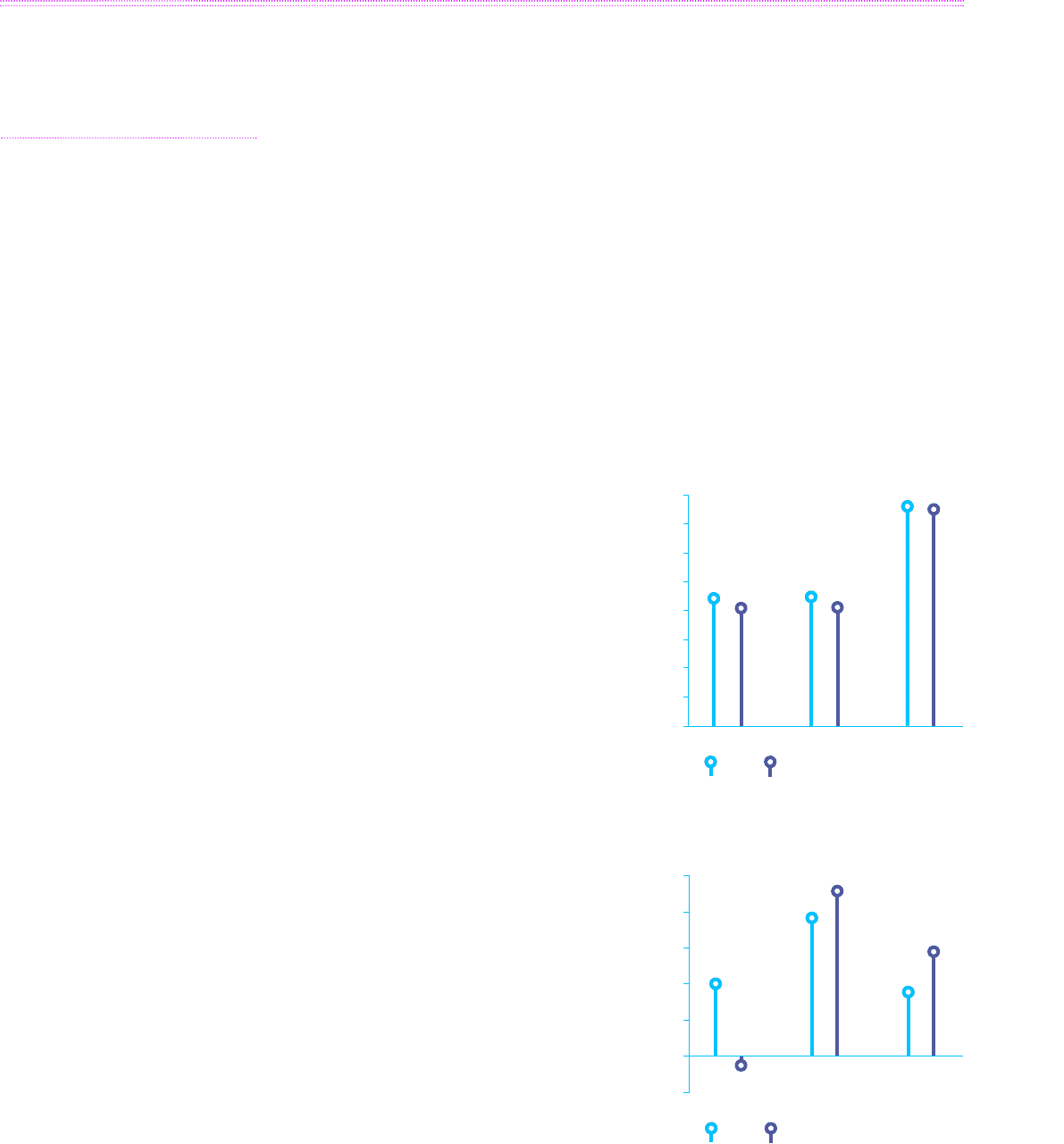

The economic

environment

16

14

12

10

8

6

4

2

0

UK US Republic

of Ireland

2011

Sources: Datastream and Office for National Statistics

2012

Unemployment rates, %, December

Real GDP growth rates, %

2.5

2.0

1.5

1.0

0.5

0

-0.5

UK US Republic

of Ireland

Sources: Datastream

Note: Ireland growth rates are four quarters to Q3 2012 over four

quarters to Q3 2011 and four quarters to Q3 2011 over four quarters

to Q3 2010

2011 2012