RBS 2012 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

136

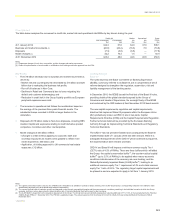

Business review Risk and balance sheet management continued

Capital management: Looking forward continued

The changes in the definition of regulatory capital under CRD IV and the

capital ratios will be subject to transitional rules:

x The increase in the minimum capital ratios and the new buffer

requirements will be phased in over the five years from

implementation of the CRD IV;

x The application of the regulatory deductions and adjustments at the

level of common equity, including the new deduction for deferred tax

assets, will also be phased in over the five years from

implementation; the current adjustment for unrealised gains and

losses on available-for-sale securities will be phased out; and

x Subordinated debt instruments which do not meet the new eligibility

criteria will be will be grandfathered on a reducing basis over ten

years.

The Group is well advanced in its preparations to comply with the new

requirements based on the draft rules. Given the phasing of both capital

requirements and target levels, in advance of needing to comply with the

fully loaded end state requirements, the Group will have the opportunity

to continue to generate additional capital from earnings and take

management actions to mitigate the impact of CRD IV.

The Group’s pro forma Core Tier 1 ratio on a fully loaded basis at 31

December 2012, based on its interpretation of the rules and assuming

they were applied today, is estimated at 7.7%(1). The pro forma capital

ratio reflects the Group’s interpretation of the draft July 2011 CRD IV

rules and how these rules are expected to be updated for subsequent EU

and Basel pronouncements.

The actual impact of CRD IV on capital ratios may be materially different

as the requirements and related technical standards have not yet been

finalised and will ultimately be subject to application by local regulators.

The actual impact will also be dependent on required regulatory

approvals and the extent to which further management action is taken

prior to implementation.

Models changes

The Group, in conjunction with the FSA, regularly evaluates its models for

the assessment of RWAs ascribed to credit risk (including counterparty

risk) across various classes. This includes implementing changes to the

RWA requirements for commercial real estate portfolios consistent with

revised industry guidance from the FSA. The changes to RWA resulting

from model changes during 2012 have increased RWA requirements by

£44 billion of which £12 billion relates to property guidance. Further uplifts

are expected in 2013 totalling c.£10 billion to £15 billion.

Other regulatory capital changes*

The Group is managing the changes to capital requirements from new

regulation and model changes and the resulting impact on the common

equity Tier 1 ratio, focusing on risk reduction and deleveraging. This is

principally being achieved through the continued run-off and disposal of

Non-Core assets and deleveraging in Markets, as the business focuses

on the most productive returns on capital. Markets RWAs decreased by

£19 billion in 2012 which also lessens the increases driven by the

counterparty risk changes in CRD IV.

European Banking Authority (EBA) recommendation

The EBA issued a recommendation in 2011 that the national regulators

should ensure that credit institutions build up a temporary capital buffer to

reach a 9% Core Tier 1 ratio by 30 June 2012 (‘the recapitalisation of EU

banks’). In its final report on the recapitalisation exercise in October 2012,

the EBA stated that once the CRD IV is finally adopted, the 2011

recommendation would be replaced with a new recommendation. The

new recommendation will include the requirement for banks to maintain a

nominal amount of Core Tier 1 capital as defined by the EBA for the 2011

stress test and recapitalisation recommendation) corresponding to the

amount of 9% of the RWAs at 30 June 2012. The Group does not expect

the potential floor to become a limiting factor.

Note:

(1) Based on the following principal assumptions: (i) divestment of Direct Line Group (ii) deductions for financial holdings of less than 10% of common equity Tier 1 capital have been excluded pending

the finalisation of CRD IV rules (iii) RWA uplifts assume approval of all regulatory models and completion of planned management actions (iv) RWA uplifts include the impact of credit valuation

adjustments (CVA) and asset valuation correlation on banks and central clearing counterparties (v) EU corporates, pension funds and sovereigns are assumed to be exempt from CVA volatility

charge in calculating RWA impacts.

*unaudited