RBS 2012 Annual Report Download - page 182

Download and view the complete annual report

Please find page 182 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

180

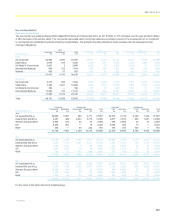

Business review Risk and balance sheet management continued

Early problem identification and problem debt management: Impairment loss provision methodology continued

Depending on various factors as explained below, the Group uses one of

the following three different methods to assess the amount of provision

required: individual; collective; and latent.

x Individually assessed provisions - Provisions required for individually

significant impaired assets are assessed on a case-by-case basis. If

there is objective evidence that an impairment loss has been

incurred, the amount of the loss is measured as the difference

between the assets carrying amount and the present value of the

estimated future cash flows discounted at the financial asset’s

original effective interest rate. Future cash flows are estimated

through a case-by-case analysis of individually assessed assets.

This assessment takes into account the benefit of any guarantees or

other collateral held. The value and timing of cash flow receipts are

based on available estimates in conjunction with facts available at

that time. Timings and amounts of cash flows are reviewed on

subsequent assessment dates, as new information becomes

available. The asset continues to be assessed on an individual basis

until it is repaid in full, transferred to the performing portfolio or

written-off.

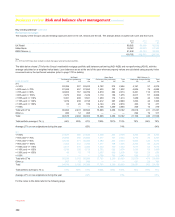

x Collectively assessed provisions - Provisions on impaired credits

below an agreed threshold are assessed on a portfolio basis to

reflect the homogeneous nature of the assets. The Group segments

impaired credits in its collectively assessed portfolios according to

asset type, such as credit cards, personal loans, mortgages and

smaller homogenous wholesale portfolios, such as business or

commercial banking. A further distinction is made between those

impaired assets in collections and those in recoveries (refer to

Problem debt management on page 176 for a discussion of the

collections and recoveries functions).

The provision is determined based on a quantitative review of the

relevant portfolio, taking account of the level of arrears, the value of

any security, historical and projected cash recovery trends over the

recovery period. The provision also incorporates any adjustments

that may be deemed appropriate given current economic and credit

conditions. Such adjustments may be determined based on: a

review of the current cash collections profile performance against

historical trends; updates to metric inputs, including model

recalibrations; and monitoring of operational processes used in

managing exposures, including the time taken to process non-

performing exposures.

x Latent loss provisions - A separate approach is taken for provisions

held against impairments in the performing portfolio that have been

incurred as a result of events occurring before the balance sheet

date but which have not been identified at the balance sheet date.

The Group’s methodologies to estimate latent loss provisions reflect:

x the probability that the performing customer will default - historical

loss experience, adjusted, where appropriate, to take into account

current economic and credit conditions; and

x the emergence period, defined as the period between an impairment

event occurring and a loan being identified and reported as impaired.

Emergence periods are estimated at a portfolio level and reflect the

portfolio product characteristics such as the repayment terms and the

duration of the loss mitigation and recovery processes. They are based

on internal systems and processes within the particular portfolio and are

reviewed regularly.

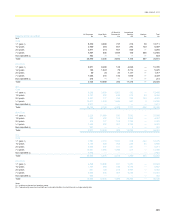

Refer to pages 224 to 241 for analysis of impaired loans, related

provisions and impairments.