RBS 2012 Annual Report Download - page 335

Download and view the complete annual report

Please find page 335 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

333

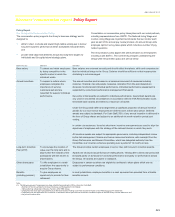

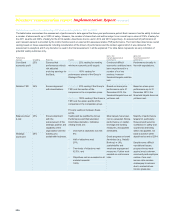

Executive directors’ annual incentive 2012 - assessment of performance outcome

Stephen Hester

Stephen Hester’s performance is measured against a number of strategic and business objectives. In the course of 2012, the Group’s priority has been

to deliver a revised Strategic Plan, given the continued challenges in the external environment. Re-balancing the Group towards the retail and

commercial business, whilst continuing to strengthen the balance sheet and reduce risks remained key. Targets for capital, short-term wholesale

funding, liquidity reserves, leverage and loan:deposit ratio were all met ahead of schedule. Stephen Hester gave strong leadership to the Group’s focus

on customers following a technology incident and to ongoing cultural change. Stephen Hester has waived any annual incentive entitlement for the 2012

performance year.

Core objectives Targets for 2012 Progress in 2012

Strategic progress Revise original Strategic Plan to

respond to significant changes in

the macro environment and outlook

for wholesale banking. Deliver

execution of revised strategy.

The continued challenges in the economic and regulatory environment prompted

revision of the Group’s strategy, including a restructured wholesale business. The

revised strategy continues to deliver on safety and soundness, whilst rebalancing the

Group towards retail and commercial business and delivering economic returns for the

Core Bank by the end of plan period. The revised strategy for the investment banking

business was implemented successfully, with restructuring targets for 2012 broadly

met. The Asset Protection Scheme was successfully exited in October; this was at the

earliest opportunity post payment of the minimum fee.

Business delivery and

financial performance

Lead delivery of overall

performance, including measures

relating to ROE, cost management,

Core Tier 1 capital ratio, funding

and risk profile, lending, EU

mandated disposals and

restructuring of the wholesale

business.

Core ROE was stable at 10%, Retail and Commercial (ex Ulster) remained strong at

14%, and Markets improved to 10%. Operating profit for Core (£6.3 billion) and Group

(£3.5 billion) were both ahead of budget. Core cost:income ratio was 59%, with Core

Tier 1 ratio at 10.3%. Core bank business lending and home loans increased by £3

billion despite weak customer confidence. More than £58 billion loans and facilities

were offered to UK businesses, of which over £30 billion was to SMEs; £16 billion of UK

home loans were advanced, including £3 billion to first time buyers. The new Funding

for Lending Scheme allowed RBS to cut interest rates on loans to small businesses and

the cost of borrowing for first time homebuyers. Branch disposal did not proceed due to

unexpected withdrawal of Santander; in contrast, Direct Line Insurance Group plc

divestment successfully executed on time and with positive market reception.

Risk and control Continue culture change across the

Group including delivery of

measures relating to wholesale

funding reliance and liquidity

reserves and leverage ratio. Deliver

against agreed APS objectives.

All risk reduction quantitative measures were met or exceeded. The liquidity portfolio is

ahead of target at £147 billion, while short-term wholesale funding was cut to £42

billion. The Group loan:deposit ratio improved to 100%, with Core loan:deposit ratio

ahead of target at 90%. Leverage was on target at 15x. The new conduct risk

framework was launched. As part of the response to the LIBOR findings and industry-

wide challenges on behaviour and ethics, led the development of the Group’s purpose,

vision and values to support cultural and behavioural change. Performance against

agreed APS objectives secured exit from the Scheme.

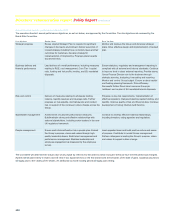

Stakeholder

management

Achievement of customer franchise

measures, maintain strong and

effective relationships with external

stakeholders and continue progress

on Treating Customers Fairly (TCF)

actions.

Customer metrics were impacted by the technology incident in the second half of 2012

- although strong leadership and successful delivery of ‘no customer out of pocket’.

Constructive engagement with regulators overall and specifically on LIBOR, conduct

risk/cultural change, and the technology incident. Early engagement with the new

Financial Conduct Authority. Continued positive feedback from key shareholders.

Increased engagement with external stakeholders on how banks should behave in

society and cultural change. Continued good progress to address risks identified by

UK/US regulators relating to TCF.

People management Ensure each division/function has

high quality leadership teams, build

out performance management,

talent management and succession

planning across the Group. Maintain

effective employee engagement.

The Group Chief Executive continues to be widely acknowledged internally and

externally as having provided strong leadership to the Group in extraordinary

circumstances. People Plans in place with continual improvement on talent bench

strength. Key replacement appointments made to Management Committee. Female

executive representation increased to 19%. The Group’s ‘Your Feedback 2012’ survey

results were stable on leadership and employee engagement in a challenging context.

The Group’s purpose, vision and values will support improvements in employee

engagement.