RBS 2012 Annual Report Download - page 160

Download and view the complete annual report

Please find page 160 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

158

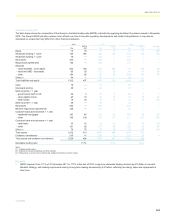

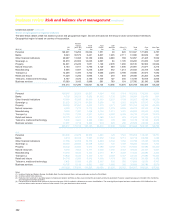

Business review Risk and balance sheet management continued

Credit risk

Introduction

Credit risk is the risk of financial loss due to the failure of a customer or

counterparty to meet its obligation to settle outstanding amounts. The

credit risk that the Group faces arises mainly from wholesale and retail

lending, provision of contingent obligations (such as letters of credit and

guarantees) and counterparty credit risk arising from derivative contracts

and securities financing transactions entered into with customers. Other

material risks covered by the Group’s credit risk management framework

are:

x Concentration risk - the risk of an outsized loss due to the

concentration of credit risk to a specific asset class or product,

industry sector, customer or counterparty, or country.

x Settlement risk - the intra-day risk that arises when the Group

releases funds prior to confirmed receipt of value from a third party.

x Issuer risk - the risk of loss on a tradable instrument (e.g. a bond)

due to default by the issuer.

x Wrong way risk - the risk of loss that arises when the risk factors

driving the exposure to a counterparty are positively correlated with

the probability of default for that counterparty.

x Credit mitigation risk - the risk that credit risk mitigation (for example,

taking a legal charge over property to secure a customer loan) is not

enforceable or that the value of such mitigation decreases, thus

leading to unanticipated losses.

Top and emerging credit risks*

The quantum and nature of credit risk assumed across the Group’s

different businesses vary considerably, while the overall credit risk

outcome usually exhibits a high degree of correlation with the

macroeconomic environment. The Group therefore remains sensitive to

the economic conditions within the geographies in which it operates, in

particular the UK, Ireland, the US and the eurozone.

The following credit risks continue to be the focus of management

attention.

Irish property market

The continuing challenging economic climate within Ireland has resulted

in impairment levels for Irish portfolios remaining at elevated levels. In

particular, high unemployment, austerity measures and general economic

uncertainty have reduced real estate lease rentals. This, together with

limited liquidity, has depressed asset values and reduced consumer

spending with a consequent downward impact on the commercial real

estate portfolio as well as broader impacts on Ulster Bank Group’s

mortgage and small and medium enterprise (SME) lending portfolios.

Further details on Ulster Bank Group’s credit risk profile can be found on

pages 190 to 193.

Commercial real estate

While progress has been made in reducing the overall exposure and

rebalancing the portfolio, commercial real estate remains a key credit

concentration risk for the Group. The Group has continued to strengthen

its approach to managing sector concentration risk, with a particular focus

on additional controls for the commercial real estate portfolio.

However, the credit performance remains sensitive to the economic

environment in the UK and Ireland. Although some improvements have

been seen in commercial real estate values across prime locations,

secondary and tertiary values remain subdued.

Refinancing risk remains a focus of management attention and is

assessed throughout the credit risk management life cycle. In particular, it

is considered as part of the early problem recognition and impairment

assessment processes.

Further details on the Group’s exposure to commercial real estate can be

found on pages 181 to 185.

Eurozone troubles

The ongoing impact of the troubles in the eurozone continued to be felt

most significantly in the banking sector, where widening credit spreads

and regulatory demand for increases in Tier 1 capital and liquidity

exacerbated the risk management challenges already posed by the

sector’s continued weakness, as provisions and write-downs remain

elevated.

A material percentage of global banking activity in risk mitigation now

passes through the balance sheets of the top global players, increasing

the systemic risks to the banking sector. The Group’s exposures to these

banks continue to be closely managed. In particular, the Group has

intensified its management of settlement risk through ongoing review of

the level of risk and the operational controls in place to manage it,

together with proactive actions to reduce limits. The weaker banks in the

eurozone also remained subject to heightened scrutiny and the Group’s

risk appetite for these banks was adjusted throughout 2012.

The Group has continued to focus on operational preparations for

possible sovereign defaults and/or eurozone exits. The Group has also

considered initiatives to determine and reduce redenomination risk.

Further actions to mitigate risks and strengthen control in the eurozone

typically included taking guarantees or insurance, updating collateral

agreements, and tightening certain credit pre-approval processes.

The Group has a material exposure to Spanish AFS debt securities

issued by banks and other financial institutions of £4.8 billion at 31

December, predominately comprised of covered bonds backed by

mortgages. Whilst the exposure was reduced by £1.6 billion during 2012,

largely as a result of sales, the portfolio continues to be subject to

heightened scrutiny, including undertaking stress analysis.

Further details on the Group’s approach to managing country risk and the

risks faced within the eurozone can be found on pages 252 to 280.

*unaudited