RBS 2012 Annual Report Download - page 170

Download and view the complete annual report

Please find page 170 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

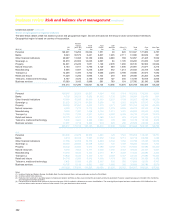

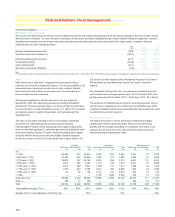

Credit risk mitigation

Approaches and methodologies*

The Group employs a number of structures and techniques to mitigate

credit risk. Netting of debtor and creditor balances is undertaken in

accordance with relevant regulatory and internal policies. Exposure on

OTC derivative and secured financing transactions is further mitigated

by the exchange of financial collateral and the use of market standard

documentation. Further mitigation may occur in a range of

transactions, from retail mortgage lending to large wholesale financing.

This can include: structuring a security interest in a physical or

financial asset; use of credit derivatives, including credit default swaps,

credit-linked debt instruments and securitisation structures; and use of

guarantees and similar instruments (for example, credit insurance)

from related and third parties. Such techniques are used in the

management of credit portfolios, typically to mitigate credit

concentrations in relation to an individual obligor, a borrower group or

a collection of related borrowers.

The use and approach to credit risk mitigation varies by product type,

customer and business strategy. Minimum standards applied across

the Group cover:

x The suitability of qualifying credit risk mitigation types and any

conditions or restrictions applicable to those mitigants;

x The means by which legal certainty is to be established, including

required documentation, supportive independent legal opinions

and all necessary steps required to establish legal rights;

x Acceptable methodologies for initial and any subsequent

valuations of collateral and the frequency with which collateral is

to be revalued and the use of collateral haircuts;

x Actions to be taken in the event that the value of mitigation falls

below required levels;

x Management of the risk of correlation between changes in the

credit risk of the customer and the value of credit risk mitigation;

x Management of concentration risks, for example, by setting

thresholds and controls on the acceptability of credit risk mitigants

and on lines of business that are characterised by a specific

collateral type or structure; and

x Collateral management to ensure that credit risk mitigation

remains legally effective and enforceable.

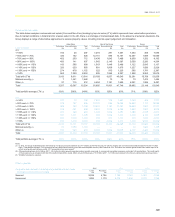

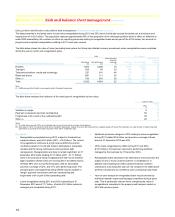

Secured portfolios

Within its secured portfolios, the Group has recourse to various types

of collateral and other credit enhancements to mitigate credit risk and

reduce the loss to the Group arising from the failure of a customer to

meet its obligations. These include: cash deposits; charges over

residential and commercial property, debt securities and equity shares;

and third-party guarantees. The existence of collateral may affect the

pricing of a facility and its regulatory capital requirement. When a

collateralised financial asset becomes impaired, the impairment charge

directly reflects the realisable value of collateral and any other credit

enhancements.

Corporate exposures

The type of collateral taken by the Group’s commercial and corporate

businesses and the manner in which it is taken will vary according to

the activity and assets of the customer.

x Physical assets - These include business assets such as stock,

plant and machinery, vehicles, ships and aircraft. In general,

physical assets qualify as collateral only if they can be

unambiguously identified, located or traced, and segregated from

uncharged assets. Assets are valued on a number of bases

according to the type of security that is granted.

x Real estate - The Group takes collateral in the form of real estate,

which includes residential and commercial properties. The market

value of the collateral will typically exceed the loan amount at

origination date. The market value is defined as the estimated

amount for which the asset could be sold in an arms length

transaction by a willing seller to a willing buyer.

x Receivables - When taking a charge over receivables, the Group

assesses their nature and quality and the borrower’s

management and collection processes. The value of the

receivables offered as collateral will typically be adjusted to

exclude receivables that are past their due dates.

The security charges may be floating or fixed, with the type of security

likely to impact: (i) the credit decision; and (ii) the potential loss upon

default. In the case of a general charge such as a mortgage

debenture, balance sheet information may be used as a proxy for

market value if the information is deemed reliable.

The Group does not recognise certain asset classes as collateral: for

example, short leasehold property and equity shares of the borrowing

company. Collateral whose value is correlated to that of the obligor is

assessed on a case-by-case basis and, where necessary, over-

collateralisation may be required.

The Group uses industry-standard loan and security documentation

wherever possible. Non-standard documentation is typically prepared

by external lawyers on a case-by-case basis. The Group’s business

and credit teams are supported by in-house specialist documentation

teams.

The existence of collateral has an impact on provisioning. Where the

Group no longer expects to recover the principal and interest due on a

loan in full or in accordance with the original terms and conditions, it is

assessed for impairment. If exposures are secured, the current net

realisable value of the collateral will be taken into account when

assessing the need for a provision. No impairment provision is

recognised in cases where all amounts due are expected to be settled

in full on realisation of the security.

168

Business review Risk and balance sheet management continued

*unaudited