RBS 2012 Annual Report Download - page 174

Download and view the complete annual report

Please find page 174 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

Early problem identification and problem debt management

While the principles of identifying, managing and providing for problem

debts are broadly similar for wholesale and retail customers, the

procedures differ based on the nature of the assets, as discussed below.

Wholesale customers

The controls and processes for managing wholesale problem debts are

embedded within the divisions’ credit approval frameworks and form an

essential part of the ongoing credit assessment of customers. Any

necessary approvals will be required in accordance with the delegated

authority grid governing the extension of credit.

Early problem recognition

Each division has established Early Warning Indicators (EWIs) designed

to identify those performing exposures that require close attention due to

financial stress or heightened operational issues. Such identification may

also take place as part of the annual review cycle. EWIs vary from

division to division and comprise both internal parameters (such as

account level information) and external parameters (such as the share

price of publicly listed customers).

Customers identified through either the EWIs or annual review are

assessed by portfolio management and/or credit officers within the

division to determine whether or not the customer’s circumstances

warrant placing the exposure on the Watchlist (detailed below).

Watchlist *

There are three Watchlist ratings - amber, red and black - reflecting

progressively deteriorating conditions. Watchlist Amber loans are

performing loans where the counterparty or sector shows early signs of

potential stress or has other characteristics such that they warrant closer

monitoring. Watchlist Red loans are performing loans where indications

of the borrower’s declining creditworthiness are such that the exposure

requires active management, usually by the Global Restructuring Group

(GRG). Watchlist Black loans comprise risk elements in lending and

potential problem loans.

Once on the Watchlist process, customers come under heightened

scrutiny. The relationship strategy is reassessed by a forum of

experienced credit, portfolio management and remedial management

professionals within the division. In accordance with Group-wide policies,

a number of mandatory actions are taken, including a review of the

customer’s credit grade and facility security documentation. Other

appropriate corrective action is taken when circumstances emerge that

may affect the customer’s ability to service its debt. Such circumstances

include deteriorating trading performance, an imminent breach of

covenant, challenging macroeconomic conditions, a late payment or the

expectation of a missed payment.

For all Watchlist Red cases, the division is required to consult with GRG

on whether the relationship should be transferred to GRG (see more on

GRG below). Relationships managed by the divisions tend to be with

companies operating in niche sectors, such as airlines or products such

as securitisation special purpose vehicles. The divisions may also

manage those exposures when subject matter expertise is available in

the divisions rather than within GRG.

At 31 December 2012, exposures to customers reported as Watchlist

Red and managed within the divisions totalled £4.3 billion (2011 - £4.9

billion).

Strategies that are available within divisions include granting a customer

various types of concessions. Any decision to approve a concession will

be a function of the division’s specific country and sector appetite, the key

credit metrics of the customer, the market environment and the loan

structure/security. Refer to the section below on Wholesale

renegotiations.

Other potential outcomes of the review of the relationship are to: take the

customer off the Watchlist and return them to the mainstream loan book;

offer further lending and maintain ongoing reviews; transfer the

relationship to GRG for those customers requiring such stewardship; or

exit the relationship altogether.

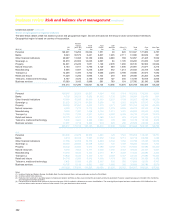

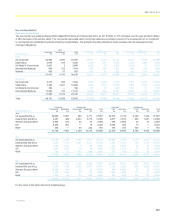

The following table shows a sector breakdown of credit risk assets of Watchlist Red counterparties under GRG management:

2012 2011

Watchlist Red credit risk assets under GRG management Core

£m

Non-Core

£m

Total

£m

Core

£m

Non-Core

£m

Total

£m

Property 5,605 4,377 9,982 6,561 6,011 12,572

Transport 2,238 478 2,716 1,159 2,252 3,411

Retail and leisure 1,542 432 1,974 1,528 669 2,197

Services 870 84 954 808 141 949

Other 3,087 1,177 4,264 1,952 916 2,868

Total 13,342 6,548 19,890 12,008 9,989 21,997

Global Restructuring Group (GRG)

In cases where the Group’s exposure to the customer exceeds £1 million,

the relationship may be transferred to GRG following consultation with

the originating division. The primary function of GRG is active

management of the exposures to minimise loss for the Group and where

feasible return the exposure to the Group’s mainstream loan book

following an assessment by GRG that no further losses are expected.

At 31 December 2012, credit risk assets relating to exposures under

GRG management (excluding those placed under GRG stewardship for

operational reasons rather than concerns over credit quality and those in

the AQ10 internal asset quality (AQ) band) totalled £19.9 billion. Credit

risk assets are defined on page 163. The internal asset quality bands are

defined on page 166.

172

Business review Risk and balance sheet management continued

*unaudited