RBS 2012 Annual Report Download - page 178

Download and view the complete annual report

Please find page 178 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

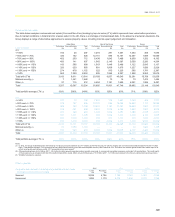

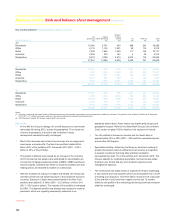

Early problem identification and problem debt management: Wholesale renegotiations continued

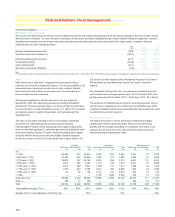

Retail customers

Collections and recoveries

There are collections functions in each of the retail businesses. Their role

is to provide support and assistance to customers who are experiencing

difficulties in meeting their financial obligations to the Group. Evidence of

such difficulties includes, for example, a missed payment on their loan, or

a balance that is in excess of the agreed credit limit. Additionally, in UK

Retail and Ulster Bank, a dedicated support team aims to identify and

help customers who may be facing financial difficulty but who are current

with their payments.

Within collections, a range of tools is deployed to initiate contact with the

customer, establish the cause of their financial difficulty and, aim to

support them where possible including the use of a range of forbearance

options. If these strategies are unsuccessful, the customer is transferred

to the recoveries team.

The goal of the recoveries function is to collect the total amount

outstanding and reduce the loss to the Group by maximising the level of

cash recovery while treating customers fairly. A range of treatment

options are available within recoveries, including litigation. In UK Retail

and Ulster Bank, no repossession procedures are initiated until at least

six months following the emergence of arrears. In Ulster Bank, new

regulations further prohibit taking legal action for an extended period.

Additionally, certain forbearance options are made available to customers

within recoveries.

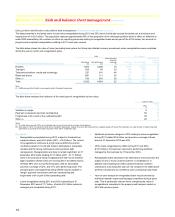

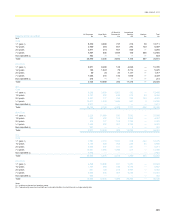

Retail forbearance

Within the Group’s retail businesses, forbearance generally occurs when

the business, for reasons relating to the actual or potential financial stress

of a borrower, grants a permanent or temporary concession to that

borrower. Forbearance is granted following an assessment of the

customer’s ability to pay. It is granted principally to customers with

mortgages. Granting of forbearance to unsecured customers is less

extensive.

Identification of forbearance

Customers are identified for forbearance treatment following initial

contact from the customer, in the event of payment arrears or when the

customer is transferred to collections or recoveries.

Types of retail forbearance

A number of forbearance options are utilised by the Group’s retail

businesses. These include, but are not limited to, payment concessions,

capitalisations of arrears over the remaining term of the mortgage,

extension to the mortgage term and temporary conversions to interest

only.

In payment concession arrangements a temporary reduction in, or

elimination of, the periodic (usually monthly) loan repayment is agreed

with the customer. At the end of the concessionary period, forborne

principal and accrued interest outstanding is scheduled for repayment

over an agreed period.

For UK Retail, interest only conversions have not been used as a tool to

support customers in financial stress since 2009. Following a change to

policy in 2012, switching to interest only is no longer permitted for

residential mortgage customers who are up to date on payments. For

Ulster Bank, interest only conversions are only offered to customers in

financial stress on a temporary basis.

As a result of the economic difficulties in the Republic of Ireland market

and responding to regulatory intervention in the Irish mortgage market,

Ulster Bank has developed additional treatment options to support

customers in overcoming financial difficulties, over an extended period of

time.

The principal types of forbearance granted in RBS Citizens’ mortgage

portfolio are the US government mandated HAMP (Home Affordable

Modification Program) and RBS Citizens’ proprietary modification

programme. Both programmes typically feature a combination of term

extensions, capitalisations of arrears, temporary interest rate reductions

and conversions from interest only to amortising. These tend to be

permanent changes to contractual terms. Borrowers seeking a

modification must meet government-specified qualifications for HAMP

and internal qualifications for RBS Citizens’ modification programme.

Both are designed to evidence that the borrower is in financial difficulty as

well as demonstrating willingness to pay.

For forbearance loans that are performing, the aim is to enable the

customer to continue to service the loan. For forbearance loans classified

as non-performing only those for which capitalisation of arrears has been

agreed can qualify for return to the performing book. Transfer of such

loans takes place currently once the customer has met the revised

payment terms for at least six months and is expected to continue to do

so.

The mortgage forbearance population is reviewed regularly to ensure that

customers are meeting the agreed terms of the arrangement. Key metrics

have been developed to record the proportion of customers who fail to

meet the agreed terms over time, as well as the proportion of customers

who return to a performing state with no arrears.

176

Business review Risk and balance sheet management continued