RBS 2012 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

142

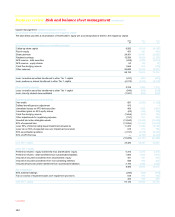

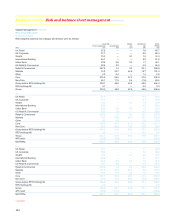

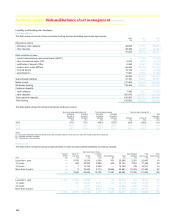

Business review Risk and balance sheet management continued

Liquidity risk continued

Contingency planning

The Group has a Contingency Funding Plan (CFP), which is updated as

the balance sheet evolves and forms the basis of analysis and actions to

remediate adverse circumstances as and if they arise. The CFP is linked

to stress test results and forms the foundation for liquidity risk limits. The

CFP provides a detailed description of the availability, size and timing of

all sources of contingent liquidity available to the Group in a stress event.

These are ranked in order of economic impact and effectiveness to meet

the anticipated stress requirement. The CFP includes documented

processes for actions that may be required to meet the outflows. Roles

and responsibilities for the effective implementation of the CFP are also

documented.

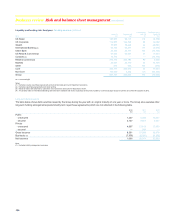

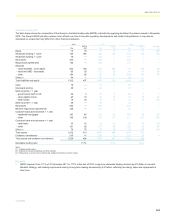

Liquidity reserves

Liquidity risks are mitigated by the Group’s centrally managed liquidity

buffer. The size of the reserve is an output from internal modelling and

the FSA’s ILG. The majority of the portfolio is held in the FSA regulated

UK Defined Liquidity Group (UK DLG) comprising the Group’s five UK

banks: The Royal Bank of Scotland plc, National Westminster Bank Plc,

Ulster Bank Limited, Coutts & Co and Adam & Company.

Certain of the Group's significant operating subsidiaries - RBS N.V., RBS

Citizens Financial Group Inc. (CFG) and Ulster Bank Ireland Limited -

hold locally managed portfolios of liquid assets that comply with local

regulations but may differ with FSA rules. These portfolios are the

responsibility of the local Treasurer who reports to the Group Treasurer.

The Group‘s liquidity buffer is managed by Group Treasury and is the

responsibility of the Group Treasurer. The liquidity buffer is ring-fenced

from the trading book within the Markets division. The liquidity buffer is

actively managed so as to balance its liquidity value relative to the margin

impact of maintaining a large and high quality investment portfolio. This is

in line with internal liquidity risk policy and appetite and regulatory

guidance. The portfolio is accounted for on an available-for-sale basis.

The value of the portfolio can move up and down based on a variety of

market movements. Gains can and will be taken through sales of

portfolios. Such sales and gains are part of normal portfolio management

and these gains can be used to offset costs in other parts of the Group.

The Group analyses its liquidity buffer including its locally managed

liquidity pools into primary and secondary liquidity groups.

The primary liquidity group generally reflects eligible liquid assets, such

as cash and balances at central banks, treasury bills and other high

quality government and agency bonds, and other local primary qualifying

liquid assets for each of the significant operating subsidiaries that

maintain a local liquidity pool.

Secondary liquidity assets represent other qualifying liquid assets that are

eligible for local central bank liquidity facilities but do not meet the core

local regulatory definition. For example, secondary liquid assets include

self-issued securitisations or covered bonds that are retained on balance

sheet and pre-positioned with a central bank so that they can be

converted into additional sources of liquidity at very short notice.

The Group in consultation with the FSA and subject to the requirements

of the FSA’s ILG can change the composition of its liquidity buffer. The

change in composition may relate to market specific factors, changes in

internal liquidity risk mix or regulatory guidance. This occurred in 2012

when the FSA agreed to recognise an increase in the amount of

secondary liquidity assets and a reduction in primary assets. Such a

change was made possible in conjunction with the introduction of the

Funding for Lending Scheme. The reduction in the balance of primary

assets was also beneficial to the Group’s margin.

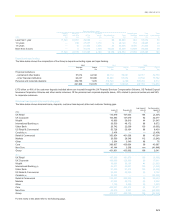

Regulatory oversight

The Group operates in multiple jurisdictions and is subject to a number of

regulatory regimes.

The Group’s lead regulator is the UK Financial Services Authority (FSA).

The FSA implemented a new liquidity regime as documented in PS

09/16, on 1 June 2010. The new rules provide a standardised approach

applied to all UK banks and all building societies as well as branches and

subsidiaries of foreign financial firms. The rules focus on the UK DLG and

cover adequacy of liquidity resources, controls, stress testing and the

Individual Liquidity Adequacy Assessment.

In addition, in the US, the Group’s operations must meet liquidity

requirements set out by the US Federal Reserve Bank, the Office of the

Comptroller of the Currency, the Federal Deposit Insurance Corporation

and the Financial Industry Regulatory Authority. In the Netherlands, RBS

N.V. is subject to the De Nederlandsche Bank liquidity oversight regime.