RBS 2012 Annual Report Download - page 177

Download and view the complete annual report

Please find page 177 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

175

Key points continued

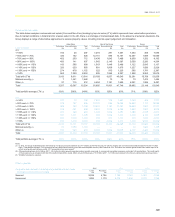

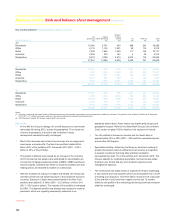

x In 2012 renegotiations were more prevalent in the Group’s most

significant corporate sectors and in those industries experiencing

difficult markets, notably property and transport as the Group seeks

to support viable customers. The majority of renegotiations granted

to borrowers in the property sector were payment concessions and

loan rescheduling. During 2012 there has been an increase in the

number of renegotiations in the shipping sector as poor economic

conditions persist.

x 84% of ‘completed’ and 93% of ‘in progress’ renegotiated cases

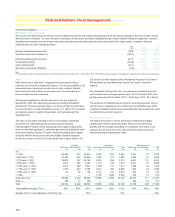

were managed by GRG.

x Provisions for the non-performing loans disclosed above are

individually assessed and renegotiations are taken into account

when determining the level of provision. The provision coverage is

affected by the timing of write-offs and provisions. In some cases

loans are fully or partially written off on the completion of a

renegotiation. Non-performing renegotiated loans also include loans

against which no provision is held and where these cases are large

they can have a significant impact on the provision coverage within

a specific sector.

Provisioning for wholesale renegotiated customers

Wholesale renegotiations are predominantly individually assessed and

are not therefore segregated into a separate risk pool.

Provisions for renegotiated wholesale loans are assessed in accordance

with the Group’s normal provisioning policies (refer to Impairment loss

provision methodology on page 179). For the non-performing population,

provisions on exposures greater than £1 million are individually assessed

by GRG. The provision required is calculated based on the difference

between the debt outstanding and the present value of the estimated

future cash flows. Exposures smaller than £1 million are deemed not to

be individually significant and are assessed collectively by the originating

division. Within the performing book, latent loss provisions are held for

those losses that are incurred, but not yet identified.

Any one of the above types of renegotiation may result in the value of the

outstanding debt exceeding the present value of the estimated future

cash flows from the renegotiated loan resulting in the recognition of an

impairment loss. Renegotiations that include forgiveness of all or part of

the outstanding debt account for the majority of such cases.

The customer’s financial position, anticipated prospects and the likely

effect of the renegotiation, including any concessions granted, are

considered in order to establish whether an impairment provision is

required.

In the case of non-performing loans that are renegotiated, the loan

impairment provision assessment almost invariably takes place prior to

the renegotiation. The quantum of the loan impairment provision may

change once the terms of the renegotiation are known, resulting in an

additional provision charge or a release of the provision in the period the

renegotiation takes place.

The transfer of renegotiated wholesale loans from impaired to performing

status follows assessment by relationship managers in GRG. When no

further losses are anticipated and the customer is expected to meet the

loan’s revised terms, any provision is written off and the balance of the

loan returned to performing status.

Performing loans that are renegotiated will be included in the calculation

of the latent loss provisions. To the extent that the renegotiation event

has affected the customer’s estimated probably of default or loss given

default, this will be reflected in the underlying calculation.

Recoveries and active insolvency management

The ultimate outcome of a renegotiation strategy is unknown at the time

of execution. It is highly dependent on the cooperation of the borrower

and the continued existence of a viable business. The following are

generally considered to be options of last resort:

x Enforcement of security or otherwise taking control of assets -

Where the Group holds collateral or other security interest and is

entitled to enforce its rights, it may take ownership or control of the

assets. The Group’s preferred strategy is to consider other possible

options prior to exercising these rights.

x Insolvency - Where there is no suitable renegotiation option or the

business is no longer regarded as sustainable, insolvency will be

considered. Insolvency may be the only option that ensures that the

assets of the business are properly and efficiently distributed to

relevant creditors.