RBS 2012 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

140

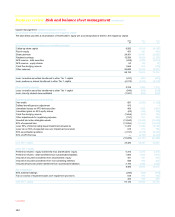

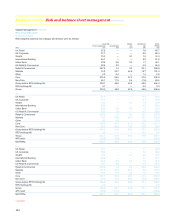

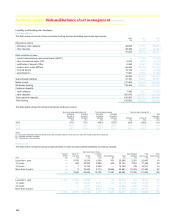

Business review Risk and balance sheet management continued

Liquidity risk: Policy, framework and governance continued

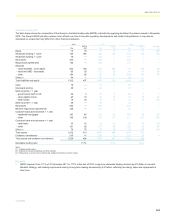

The ILAA is the cornerstone of the Group’s assessment process and

informs the Group Board and the FSA of the assessment and

quantification of the Group’s liquidity risks and their mitigation and how

much current and future liquidity is required to manage those risks.

The Group has identified ten specific liquidity risk factors which range

from the risk associated with both behavioural and contractual customer

deposit outflows, through to firm-specific reputational factors that could

impact the Group’s liquidity position from time to time.

In addition, the Group follows the broader market developments in

respect of the ongoing evolution of industry and regulatory liquidity risk

policies that are currently being debated at an international level and

adjusts its policies and processes where appropriate.

Finally, external stakeholders such as market counterparties, debt and

equity investors and credit rating agencies actively review and challenge

the Group’s approach, their views being reflected through their ongoing

support of the Group.

The Group actively monitors ongoing regulatory developments in the

international arena. Whilst most individual country regulators have

implemented or refined specific country liquidity regulations, much work

continues at an international level to agree common standards.

The majority of this work is conducted under the auspices of the Basel

Committee on Bank Supervision and includes discussion on important

measures such as the liquidity coverage ratio (LCR) and the net stable

funding ratio (NSFR). The Group will always look to proactively adopt

such measures into its reporting capabilities provided that there is an

alignment and agreement between domestic and international regulators

on these issues and specific country regulatory rules are updated to

reflect these agreements.

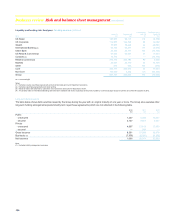

In January 2013, the Basel Committee on Banking Supervision issued its

revised draft guidance for calculating the LCR, which is currently

expected to come into force from 1 January 2015 on a phased basis.

Pending the finalisation of the definitions, the Group monitors the LCR

and the NSFR in its internal reporting framework based on its

interpretation and expectation of the final rules. On this basis, as of 31

December 2012, the Groups LCR was over 100% and the NSFR 117%.

At present there is a broad range of interpretations on how to calculate

the NSFR and, especially, the LCR due to the lack of a commonly agreed

market standard. There are also inconsistencies between the current

regulatory approach of the FSA and that being proposed in the LCR with

respect to the treatment of unencumbered assets that could be pledged

to central banks via a discount window facility. This makes meaningful

comparisons of the LCR between institutions difficult. The Group will

continue to work with regulators and industry groups to measure and

report the impact of the rules as they are finalised. Assumptions will be

refined as regulatory interpretations evolve.

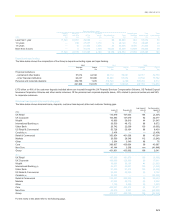

Liquidity measurement and monitoring

Liquidity risk is measured and assessed on a daily basis at Group level.

The Group uses a set of internal and regulatory metrics and analysis to

assess liquidity risk.

The Group uses limits to manage and control the overall extent of liquidity

risk within the balance sheet. Limits focus on the aggregate risk, the

amount and composition of particular sources of liabilities, asset liability

mismatches and third party counterparty concentrations. Reported

balance sheet metrics such as loan:deposit ratio targets or the

percentage of short-term wholesale funding are examples of these limits.

The Group also uses appropriate transfer pricing of liquidity costs to

foster appropriate pricing behaviour and decision making. The Group’s

internal transfer pricing policy helps to manage the balance sheet mix

and composition of contingent and actual liabilities and to ensure that

liquidity risk is reflected in product pricing and divisional business

performance measurement. This also ensures that divisions are being

correctly incentivised to source the most appropriate mix of funding.

Stress and scenario testing is used to help inform a broader

understanding of liquidity risk as well as to model specific liquidity risks

events, for example the secession of a country from the euro.

The Group actively monitors a range of market and firm-specific early

warning indicators of emerging liquidity stresses. Some of these

indicators will be actual performance of the business against pre-agreed

limits, for example customer deposit outflows. Others will be based

around general or specific market movements such as movements in the

Group’s credit default swap spreads.

Liquidity risks are reviewed at legal entity daily, and performance

reported to Divisional and Group Asset and Liability Committees. Any

breach or material deterioration of these metrics will set in motion a

series of actions and escalations that could lead to activation of the

contingency funding plan. Any breach of these metrics that subsequently

means that the Group can no longer comply with its ILG will necessitate

notification to the FSA and the eventual submission of a liquidity

remediation plan.

The Group’s liquidity risk framework is subject to internal oversight,

challenge and governance both at Board level and via internal control

functions such as Internal Audit. The Group is also subject to regulatory

review and challenge from the FSA through its supervisory programme.