RBS 2012 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

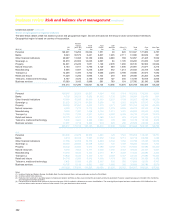

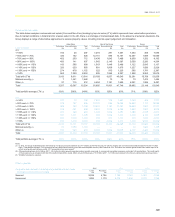

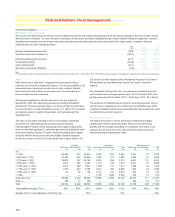

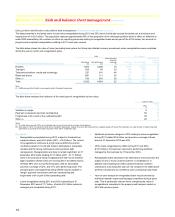

173

Wholesale renegotiations

Loan modifications take place in a variety of circumstances including but

not limited to a customer’s current or potential credit deterioration. Where

the contractual payment terms of a loan have been changed because of

the customer’s financial difficulties, it is classified as ‘renegotiated’ in the

wholesale portfolio.

Loans modified in the normal course of business where there is no

evidence of financial difficulties and any changes to terms and conditions

are within acceptable credit parameters, within credit risk appetite and/or

reflective of improving conditions for the customer in the credit markets,

are not considered to have been renegotiated.

A number of options are available to the Group when a wholesale

customer is facing financial difficulties and corrective action is deemed

necessary. Such actions are tailored to the individual circumstances of

the customer. The aim of such actions is to assist the customer in

restoring its financial health and to minimise risk to the Group. To ensure

that the renegotiations are appropriate for the needs and financial profile

of the customer, the Group requires minimum standards to be applied

when assessing, recording, monitoring and reporting this type of activity.

Wholesale renegotiations involve the following types of concessions:

x Variation in margin - The contractual margin may be amended to

bolster the customer’s day-to-day liquidity, with the aim of helping to

sustain the customer’s business as a going concern. This would

normally be seen as a short-term solution and is typically

accompanied by the Group receiving an exit payment, a payment in

kind or a deferred fee.

x Payment concessions and loan rescheduling - payment concessions

or changes to the contracted amortisation profile including

extensions in contracted maturity may be granted to improve the

customer’s liquidity. Such concessions often depend on the

expectation that the customer’s liquidity will recover when market

conditions improve or will benefit from access to alternative sources

of liquidity, such as an issue of equity capital. These types of

concessions are common in commercial real estate transactions,

particularly where a shortage of market liquidity rules out immediate

refinancing and makes short-term forced collateral sales unattractive.

x Forgiveness of all or part of the outstanding debt - debt may be

forgiven or exchanged for equity in cases where a fundamental shift

in the customer’s business or economic environment means that the

customer is incapable of servicing current debt obligations and other

forms of renegotiations are unlikely to succeed in isolation. Debt

forgiveness is often an element in leveraged finance transactions,

which are typically structured on the basis of projected cash flows

from operational activities, rather than underlying tangible asset

values. Provided that the underlying business model and strategy

are considered viable, maintaining the business as a going concern

with a sustainable level of debt is the preferred option, rather than

realising the value of the underlying assets.

In addition, the Group may offer a temporary covenant waiver, a

recalibration of covenants and/or a covenant amendment to cure a

potential or actual covenant breach. Such relief is usually granted in

exchange for fees, increased margin, additional security, or a reduction in

maturity profile of the original loan. These financial covenant concessions

are monitored internally, but are not included in the renegotiated loans

data (when this is the sole concession granted to a customer) as we

believe that such concessions are qualitatively different from other

renegotiations: The loan’s payment terms are unchanged. Covenant

concessions provide an early warning indicator rather than firm evidence

of a significant deterioration in credit quality.

The impact on the credit quality of any change in terms and conditions of

a loan is assessed at the time of granting such changes, and the

appropriateness of the credit metrics reviewed at such time. For

performing counterparties, credit metrics are an integral part of the latent

provision methodology and therefore the impact of covenant concessions

will be reflected in the latent provision. For non-performing

counterparties, covenant concessions will be considered in the overall

provision adequacy for these loans.

Covenant waivers and amendments are predominantly undertaken prior

to transfer to GRG. The vast majority of the other types of renegotiations

undertaken by the Group take place within GRG. Forgiveness of debt and

exchange for equity is only available to customers in GRG.

Loans may be renegotiated more than once, generally where a temporary

concession has been granted and circumstances warrant another

temporary or permanent revision of the loan’s terms. Where renegotiation

is no longer viable, the Group will consider other options such as the

enforcement of security and or insolvency proceedings.