RBS 2012 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

141

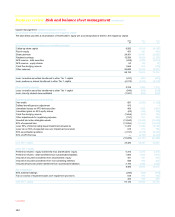

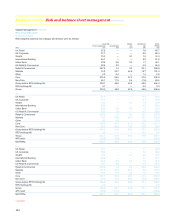

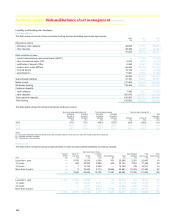

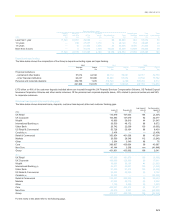

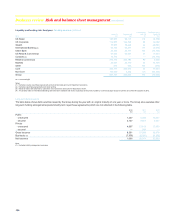

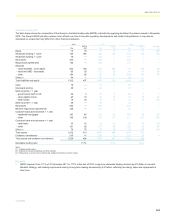

Stress testing*

The strength of any bank’s liquidity risk management can only be

evaluated on the Group’s ability to survive under stress.

Simulated liquidity stress testing is regularly performed for each business

as well as the major operating subsidiaries. Stress tests are designed to

look at the impact of a variety of firm-specific and market-related

scenarios on the future adequacy of the Group’s liquidity resources.

Stress tests can be run at any time in response to the emergence of one

of these risks.

Scenarios include assumptions about significant changes in key funding

sources, external credit ratings, contingent uses of funding, and political

and economic conditions or events in particular countries. For example,

during 2012 the Group undertook a specific series of stress tests to

assess the likely worst case impact associated with a one notch

downgrade to the Group’s credit rating by Moody’s. Stress scenarios are

applied to both on-balance sheet instruments and off-balance sheet

activities, to provide a comprehensive view of potential cash flows.

In determining the adequacy of the Group’s liquidity resources the Group

focuses on the stressed outflows it could be anticipated to experience as

a result of any stress scenario occurring. These outflows are measured

as occurring over certain time periods which extend from any given day

out to two weeks, to as long as three months. The Group is expected to

be able to withstand these stressed outflows through its own resources

(principally the use of the liquidity buffer) over these time horizons without

having to revert to extraordinary central bank or governmental

assistance.

The Group’s actual experiences from the 2008 and 2009 period have

factored heavily into the liquidity analysis in the past, although more

recent market conditions and events provide more up-to-date data for

scenario modelling. Stress tests are augmented from time to time to

reflect firm-specific or emerging market risks that could have a material

impact on the Group’s liquidity position.

The Group’s liquidity risk appetite is measured by reference to the

liquidity buffer as a percentage of stressed contractual and behavioural

outflows under the worst of three severe stress scenarios as envisaged

under the FSA regime. Liquidity risk is expressed as a surplus of liquid

assets over three months’ stressed outflows under the worst of a market-

wide stress, an idiosyncratic stress and a combination of both. At 31

December 2012, the Group’s holding of liquid assets was 128% of the

worst case stress requirements.

The results of stress testing are an active part of management and

strategy in balance sheet management and inform allocation, target and

limit discussions. In short, limits in the business-as-usual environment are

bounded by capacity to satisfy the Group’s liquidity needs in the stress

environments.

Key liquidity risk stress testing assumptions

x Net wholesale funding - Outflows at contractual maturity of

wholesale funding and conduit commercial paper, with no

rollover/new issuance. Prime Brokerage, 100% loss of excess client

derivative margin and 100% loss of excess client cash.

x Secured financing and increased haircuts - Loss of secured funding

capacity at contractual maturity date and incremental haircut

widening, depending upon collateral type.

x Retail and commercial bank deposits - Substantial outflows as the

Group could be seen as a greater credit risk than competitors.

x Intra-day cashflows - Liquid collateral held against intra-day

requirement at clearing and payment systems is regarded as

encumbered with no liquidity value assumed. Liquid collateral is held

against withdrawal of unsecured intra-day lines provided by third

parties.

x Intra-group commitments and support - Risk of cash within

subsidiaries becoming unavailable to the wider Group and

contingent calls for funding on Group Treasury from subsidiaries and

affiliates.

x Funding concentrations - Additional outflows recognised against

concentration of providers of wholesale secured financing.

x Off-balance sheet activities - Collateral outflows due to market

movements, and all collateral owed by the Group to counterparties

but not yet called; anticipated increase in firm’s derivative initial

margin requirement in stress scenarios; collateral outflows

contingent upon a multi-notch credit rating downgrade of Group

firms; drawdown on committed facilities provided to corporates,

based on counterparty type, creditworthiness and facility type; and

drawdown on retail commitments.

x Franchise viability - Group liquidity stress testing includes additional

liquidity in order to meet outflows that are non-contractual in nature,

but are necessary in order to support valuable franchise businesses.

x Management action - Unencumbered marketable assets that are

held outside of the Core liquidity buffer and are of verifiable liquidity

value to the firm, are assumed to be monetised (subject to

haircut/valuation adjustment).

*unaudited