RBS 2012 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

122

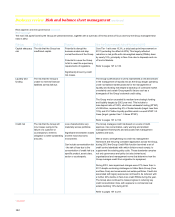

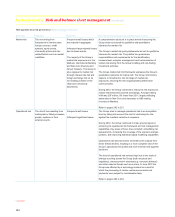

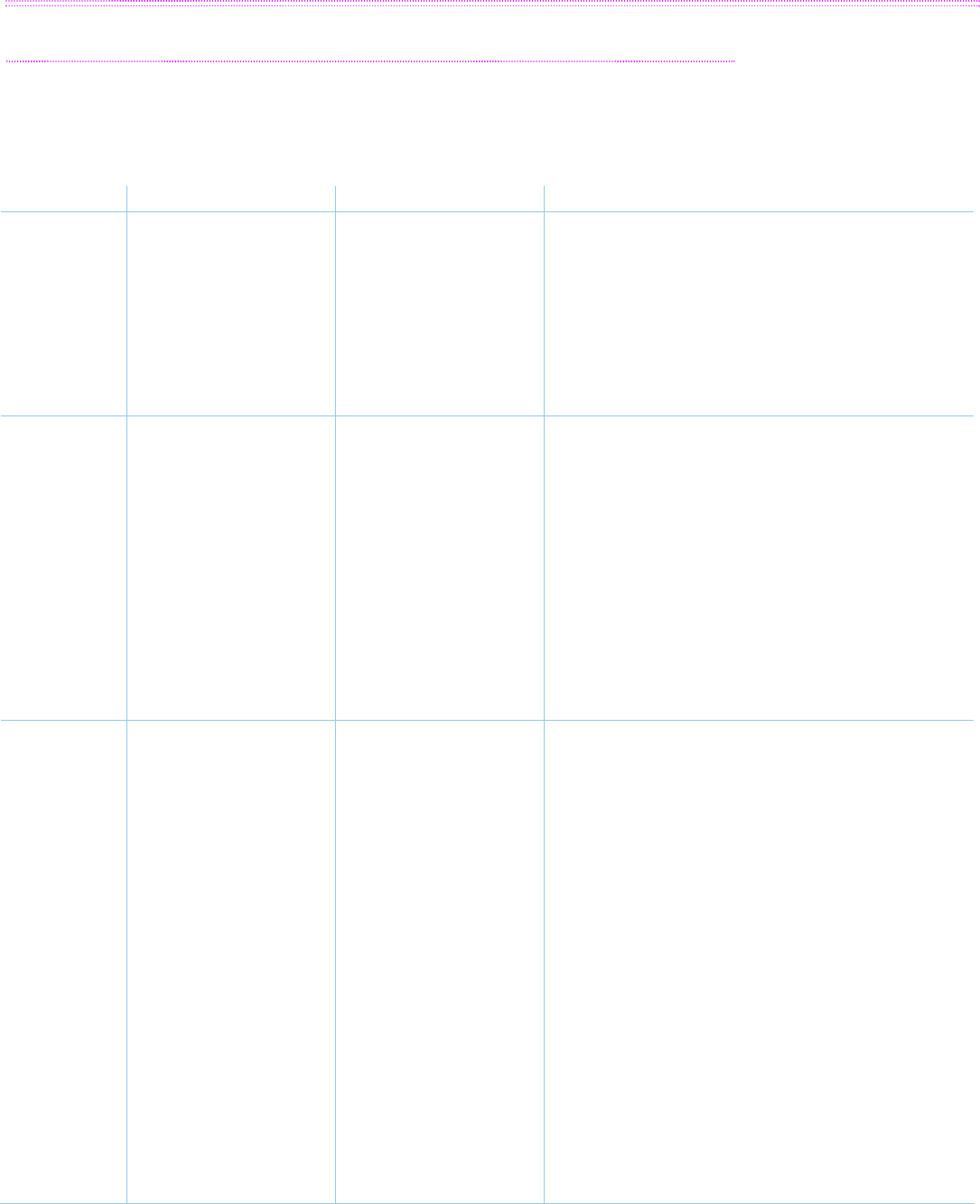

Business review Risk and balance sheet management continued

Risk appetite and risk governance continued

Risk coverage*

The main risk types faced by the Group are presented below, together with a summary of the key areas of focus and how the Group managed these

risks in 2012.

Risk type Definition Features How the Group managed risk and the focus in 2012

Capital adequacy

risk

The risk that the Group has

insufficient capital.

Potential to disrupt the

business model and stop

normal functions of the Group.

Potential to cause the Group

to fail to meet the supervisory

requirements of regulators.

Significantly driven by credit

risk losses.

Core Tier 1 ratio was 10.3%, a sixty basis point improvement on

2011 (excluding the effect of APS). This largely reflected

reduction in risk profile with risk-weighted assets (RWAs) down

by nearly 10%, principally in Non-Core due to disposals and run-

off and in Markets.

Refer to pages 127 to 136.

Liquidity and

funding

The risk that the Group is

unable to meet its financial

liabilities as they fall due.

The Group’s performance in 2012 represented a new benchmark

in the management of liquidity risk as the Group began operating

under normalised market practices for the management of

liquidity and funding risk despite a backdrop of continued market

uncertainty and certain Group-specific factors such as a

downgrade of the Group’s external credit rating.

The Group met or exceeded its medium term strategic funding

and liquidity targets by 2012 year end. This included a

loan:deposit ratio of 100%, short-term wholesale funding (STWF)

of £42 billion, representing 5% of funded assets (target: less than

10%) and £147 billion liquidity portfolio which covered STWF 3.5

times (target: greater than 1.5 times STWF).

Refer to pages 137 to 156.

Credit risk The risk that the Group will

incur losses owing to the

failure of a customer or

counterparty to meet its

obligation to settle outstanding

amounts.

Loss characteristics vary

materially across portfolios.

Significant link between losses

and the macroeconomic

environment.

Can include concentration risk

- the risk of loss due to the

concentration of credit risk to a

specific product, asset class,

sector or counterparty.

The Group manages credit risk based on a suite of credit

approval, risk concentration, early warning and problem

management frameworks and associated risk management

systems and tools.

With a view to strengthening its credit risk management

framework and ensuring consistent application across the Group,

during 2012 the Group Credit Risk function launched a set of

credit control standards with which divisions must comply, to

supplement the existing policy suite. These standards comprise

not only governance and policy but also behavioural,

organisational and management norms that determine how the

Group manages credit from origination to repayment.

During 2012, loan impairment charges were 27% lower than in

2011 despite continuing challenges in Ulster Bank Group (Core

and Non-Core) and commercial real estate portfolios. Credit risk

associated with legacy exposures continued to be reduced, with

a further 34% decline in Non-Core credit RWAs during the year.

The Group also continued to make progress in reducing key

credit concentration risks, with exposure to commercial real

estate declining 16% during 2012.

Refer to pages 157 to 241.

*unaudited